Written by: Natalia Espinosa Tokuhama, under the supervision of Kim Wilson

Table of Contents

On a Wednesday afternoon near the Parque El Arbolito at the entrance to the center of Quito, we met Nia. She was the owner of a convenience store-internet café. Pasted to the cash register was a large “Banesco” logo. We had noted that many “tienditas” — corner stores — also displayed Banesco signage, usually in their windows, and further inquiries led us to understand that these stores were operating semi-underground money transfer businesses. When we asked about how the remittance services worked, shopkeepers were reluctant to respond. After many refusals to be interviewed, we, at last, met Nia. She agreed to explain the entire process to us if we would wait a few hours. We agreed and later returned to her store to engage in a long chat. Sitting in plastic chairs, we huddled in the section of the cafe where clients could buy and eat sandwiches for just a dollar. Her two employees manned the internet café stations and the register, listening in and occasionally chiming into the conversation.

Nia’s Journey to Quito

Nia moved to Ecuador from Venezuela in 2017 and worked for a year in Ibarra, Imbabura, in the north of Ecuador before making her way to Quito. She had studied “Comercio Exterior y Aduanas” (International Trade and Customs), a degree common in Latin America in which students navigate various customs requirements between large trading blocks, as well as learn about taxation policies, international shipping requirements, and logistics. In Imbabura, Nia worked as an international insurance broker for a shipping fleet but was paid only $200 a month, well below minimum wage (now $400/month). She then moved to Quito to do the same work with her cousin, which included commission fees as part of her employment package. Nearly a year ago, she and her cousin opened a second location — the internet café we were now seated in.

Nia Teaches us How Underground Remittance Systems Work

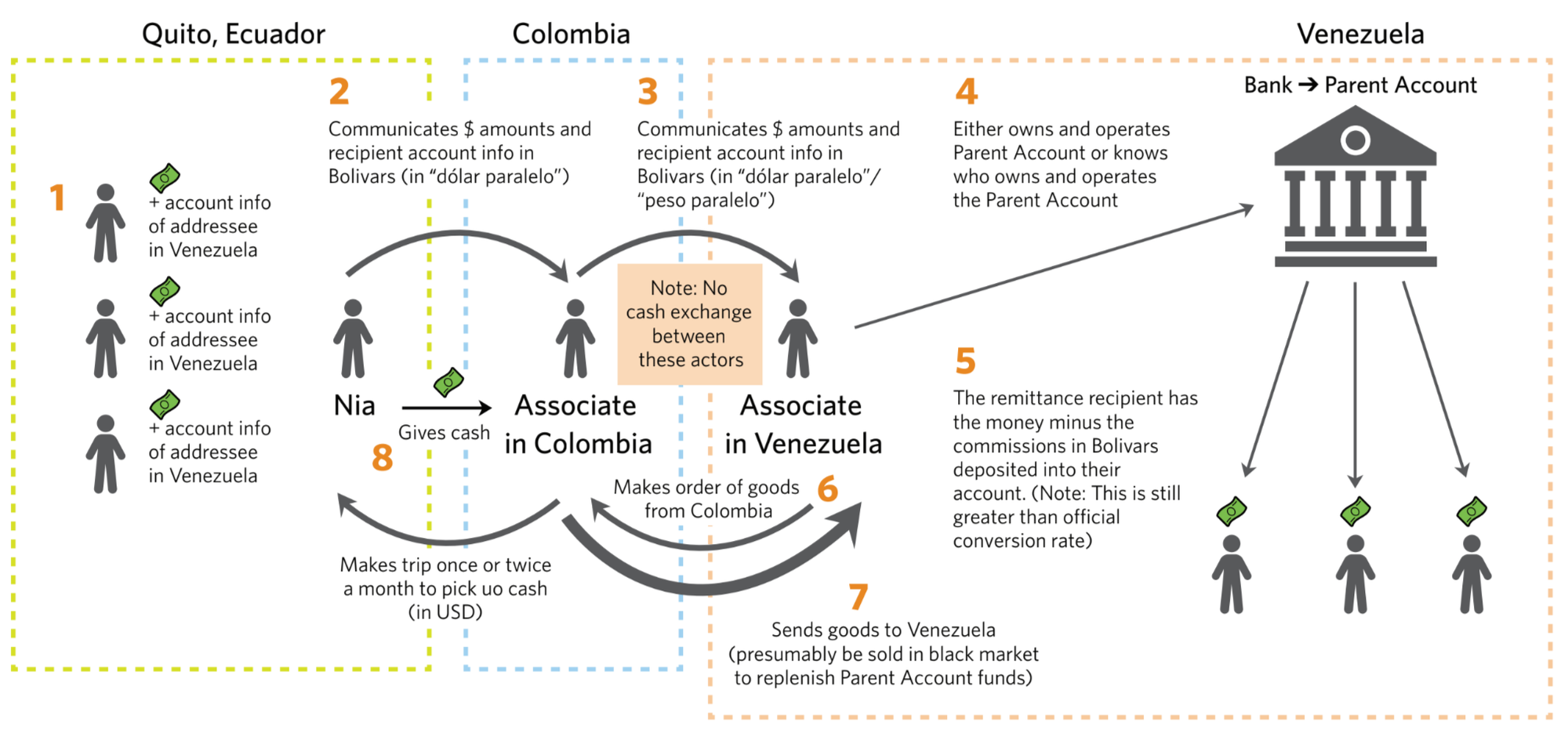

When we asked Nia to explain how the Banesco transfers worked, she pulled out a pen and began doodling arrows. The sketch, at first, was inscrutable. Nia, a bubbly young woman, used the lines she drew on the paper as an extension of her hand gestures. I began to take my own notes, asking her to slow down so that eventually my own diagrams began to match her words. Nia gently corrected me as we went along.

The process begins in Quito, where foreign workers want to send remittances back home. For example, Raul, a Venezuelan living in Quito, wants to send money to relatives back in Venezuela. He could send the remittance through an authorized transfer agency (e.g., Western Union), but he would need to use the official exchange rate, wildly inflated due to the Venezuelan government’s currency controls. Or, Raul could opt for Nia’s service, which offers a more favorable exchange rate based on the ‘dolar paralelo’ – the black-market exchange rate.¹ Although Nia takes a percentage of the transfer as her fee, her service is cheaper than sending money using the official exchange rate. When Raul chooses Nia’s service, he sends her U.S. dollars,² as well as information for the Venezuelan bank account where the money should be deposited.³ Although the remittance amount is generally small ($5, $10, or $20), exchanging it to Bolivars at the black-market rate greatly increases the purchasing power for those in Venezuela.⁴

Step two is when Nia informs Carlos, her cousin, business partner, and the Colombian-based ringmaster of the operation, of the amount that should be deposited into the Venezuelan bank accounts. The value of the deposits equals the dollars collected in step one, converted into Bolivars at the black-market rate, minus Nia’s fees. Often, Nia bundles the funds of multiple clients, given the small size of the average remittance per client. No cash is transferred at this stage.

Next, Carlos informs his contact in Venezuela, Victor, of the sum (in Bolivars) that should be deposited into the Venezuelan accounts, along with the corresponding bank account information.

In step three, Victor, using the information provided by Carlos in step two, makes the deposits from his own bank account using his existing funds (i.e., he has not yet received any cash transfer from Carlos or Nia). Once the deposits have been made, Victor shows Carlos the deposit receipts. Victor, in turn, confirms the transactions with Nia, who then sends along confirmations to her clients in Ecuador. In exchange for the deposits, Victor has a credit with Carlos. Still, no cash has been exchanged.

In step four, Victor uses the credit from step three to order goods from Carlos. For example, if Victor made payments totaling $300 USD in step three, he would order $300 USD worth of Colombian goods (minus Carlos’ small fee) from Carlos. Victor typically orders goods that are scarce in Venezuela. Carlos buys these items in Colombia and then crosses into Venezuela to deliver them to Victor.⁵ Victor takes possession of the goods and is able to resell them in Venezuela at an inflated price. Effectively, this markup yields Victor his profits. Victor also benefits from having buying power in a foreign currency and a partner, Carlos, who is willing to transport and, in some cases, smuggle goods into Venezuela.

In the final step, Carlos visits Quito to collect the U.S. dollars that Nia had collected in Step 1. Nia was vague about what happened next with the cash, but our guess is that Carlos either uses the dollars for transactions in Colombia or Venezuela or simply saves it. People in Venezuela, but also to a less drastic degree in Colombia, prefer to save “under the mattress” or transact in dollars because the currency is far more likely to retain its value than the Bolivar or Peso.⁶ This has led many merchants to accept dollars in daily transactions, often resulting in significant savings for the buyer. Imagine you want to buy a burlap sack of oranges in Colombia. The bag is being sold for 4,000.00 pesos, which in December 2020 is roughly equivalent to $1.15 USD. However, if you pay the vendor in dollars, he could agree to charge you just $1 USD.

Thanks to this informal remittance scheme, Carlos is able to generate quite a bit of cash—and then reap the benefits that come with it. So, although the system poses a risk to him, they are outweighed by the value of the greenbacks.

Running the Remittance Business and Goals

Since Nia had a good location for her shop, she made good money. But the monthly operating costs of rent ($290), electricity ($20), internet ($20), and salaries ($300 per employee) were adding up. She says she can save about $200 a month from her $500-$700 salary (varies depending on her commission). She pays a lot in rent because she likes living in “la Zona”, an area around Mariscal Foch Plaza known for its party scene. She enjoys the environment and the fact that she can walk to work without having to worry about buses. Despite Nia’s target of $200 a month in savings, she says she often falls short. She tries to send her mother and grandmother $70 a month, but confesses that this is hard to do. She can easily spend over $100 a month on evenings out or $120 a month meeting her “sanitary and beauty” needs. (After further probing, we learned that she used “sanitary and beauty” to encapsulate shopping for cosmetics, visiting nail and hair care salons, but also includes buying everyday items such as shampoo or soap.)

Nia claimed that her intention was never to stay permanently in Ecuador. As with many of our refugee respondents, she seemed to have put down substantial roots in Ecuador but has always seen her stay in the country as a prolonged visit. Toward the end of the interview, Nia disclosed that if she were to meet her savings goals this year, she could proceed to her final destination: Europe. “Maybe I’ll be in Spain by the end of the year, that is the plan,” she told us, “I’m going to make that my New Year’s resolution.”

Though Nia’s shop was managed much like any other that brandished the Banesco sign, hers was the one we came to understand in granular detail. Nia’s candid explanation showed us just how powerful innovation can be in the face of constraints imposed by the state. We are grateful for her candor, her patience, and her cheery countenance.

📝 This article was originally published as a report by the Henry J. Leir Institute at The Fletcher School of Law & Diplomacy and Tufts University.

Download the original report below ⬇️