Written by: Kim Wilson and Roxanne Krystalli

Table of Contents

Project Overview, Research Questions, and Methods

The Financial Journeys of Refugees investigates what money and financial transactions can reveal about the journeys and experiences of forced migration. We examine money as a key node of the displacement experience: fueling transactions among formal and informal actors along the way; determining livelihood options; shaping or restructuring kinship networks; and coloring risks, vulnerabilities, or protective forces available to refugees. Our inquiry highlights these transactions and the power dynamics that unfold among refugees as well as between refugees and formal or informal authorities.

Four specific areas of inquiry emerged during this study:

- How do refugees gather, move, store, spend, and make money along the journey of their displacement? How do their strategies lead to enhanced risk and/or self-protection along the way?

- How do financial transactions structure relationships among refugees, as well as between refugees and formal or informal authorities, such as smugglers, informal money transfer agents, and formal banking systems?

- How does the humanitarian system—and, in particular, cash assistance to refugees—shape the aforementioned financial transactions and relationships?

- What are the roles of refugee identity—in terms of gender, ethnicity, religion, and family status—and the documentation of that identity in shaping financial transactions, relationships, vulnerability, and coping strategies?

We pursued these questions in a qualitative study that unfolded between July 2016 and April 2017 at multiple sites in Greece, Jordan, and Turkey. We interviewed 120 refugees and 33 key informants and conducted observations at refugee camps and shelters, informal refugee settlements, money transfer offices, and other locations. This executive summary—and the full report it accompanies—are one of many outputs associated with this research project, all of which are available at the Henry J. Leir Institute for Human Security website.

The significance of the above questions is threefold. First, inquiries about money on the move provide an entry point to exploring the risks refugees face, their coping strategies, and their relationships with formal and informal authorities. In this case, money—and the ways in which refugees amass, move, and spend it—is a window into understanding structures of power, access, protection, and vulnerability.

Second, to the extent that financial inclusion literature and practice engage with refugees, they do so “in terms of integrating customers into an existing digital or formal financial structure,” without focusing on the financial tasks that refugees must perform in order to survive. This study sheds light on the diversity of these experiences and the needs to which they give rise along the way.

Third, while refugee integration into economies and markets is slowly receiving attention as refugees arrive at points of resettlement or their aspirational destinations, to date, little attention has been paid to financial portfolios, transactions, and relationships along the way. Being “in motion”—as opposed to displaced and stationary—is a part of the humanitarian process that needs to be understood more fully.

Summary of Findings: Financial Portfolios of Refugees

Even the most sudden displacement requires financial and logistical preparation—and when that is not possible, refugees face intermittent journeys, with long pauses between stints of movement and possibly higher risks along the way. Preparations include selling land, livestock, and other assets; borrowing money from within kinship networks; making arrangements with smugglers and money transfer agents; and liquidating assets, where possible.

Costs of transit varied greatly among refugees, depending on the route, the timing, and political developments that affected the accessibility of certain routes, family configuration, and other factors.

Paying for smugglers remained the largest, most significant cost of transit. Refugees who participated in the research framed smugglers not necessarily as criminal actors but as essential to their transit and paying them as a livelihood choice they made to facilitate their passage.

Rarely did the funds refugees gathered in advance of their displacement suffice for financing the entire journey. Refugees thus resorted to a combination of formal and informal labor along the way, as well as to borrowing money, where possible. The lack of sufficient funds to pay for the next leg of a journey was most frequently cited as the reason some refugees were “stuck” in the country in which our research team met them.

Summary of Findings: Financial Relationships on the Move

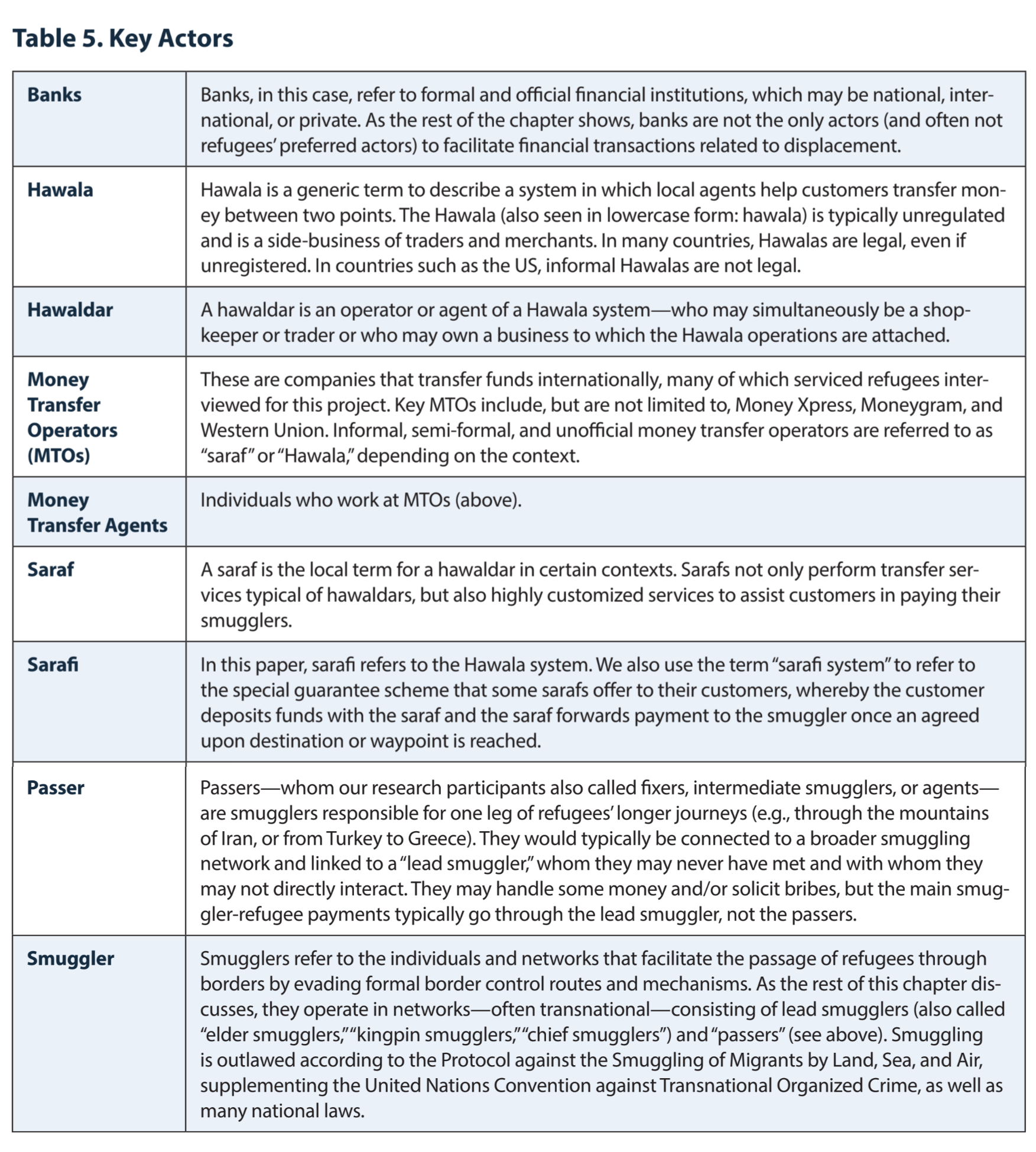

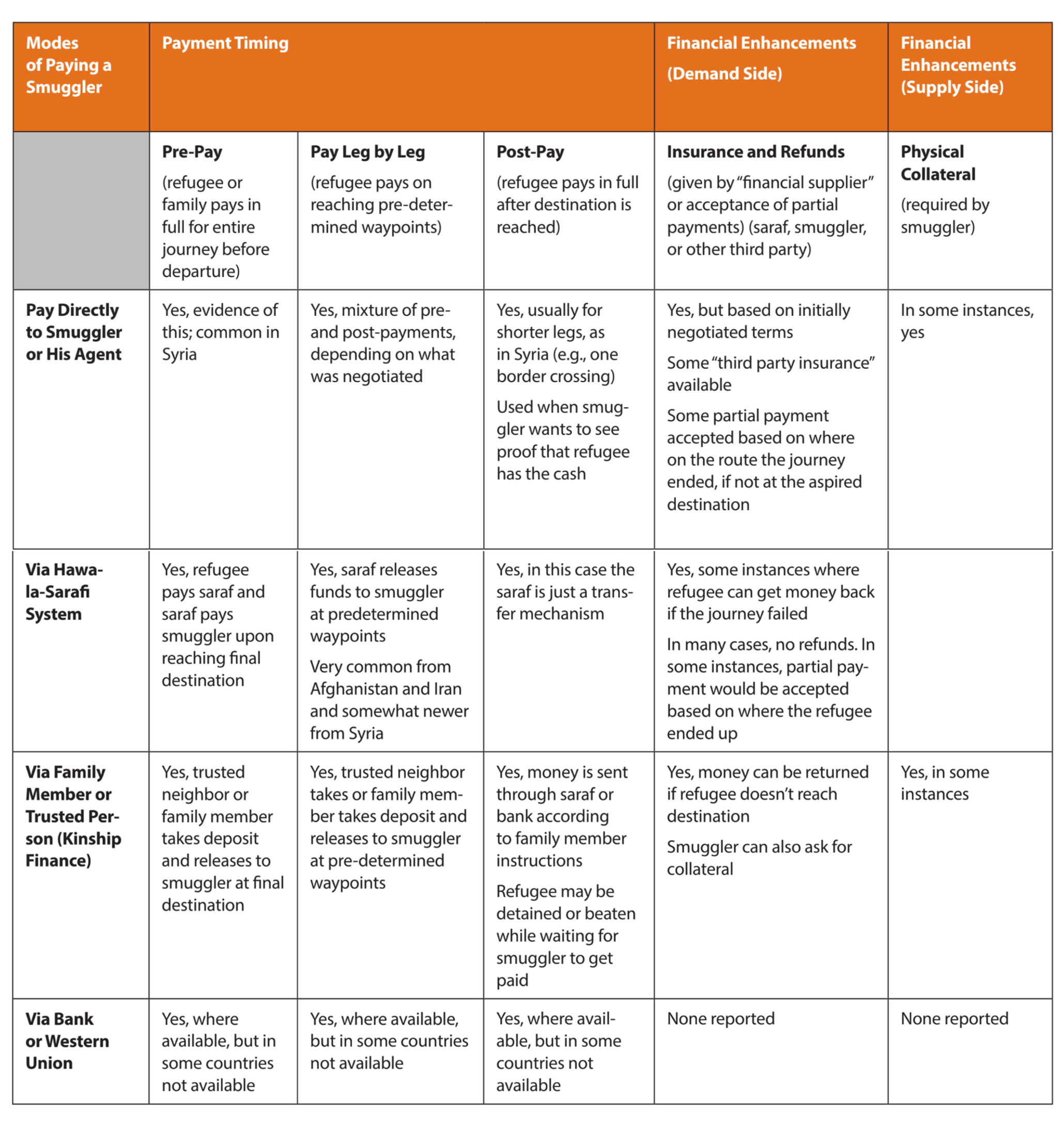

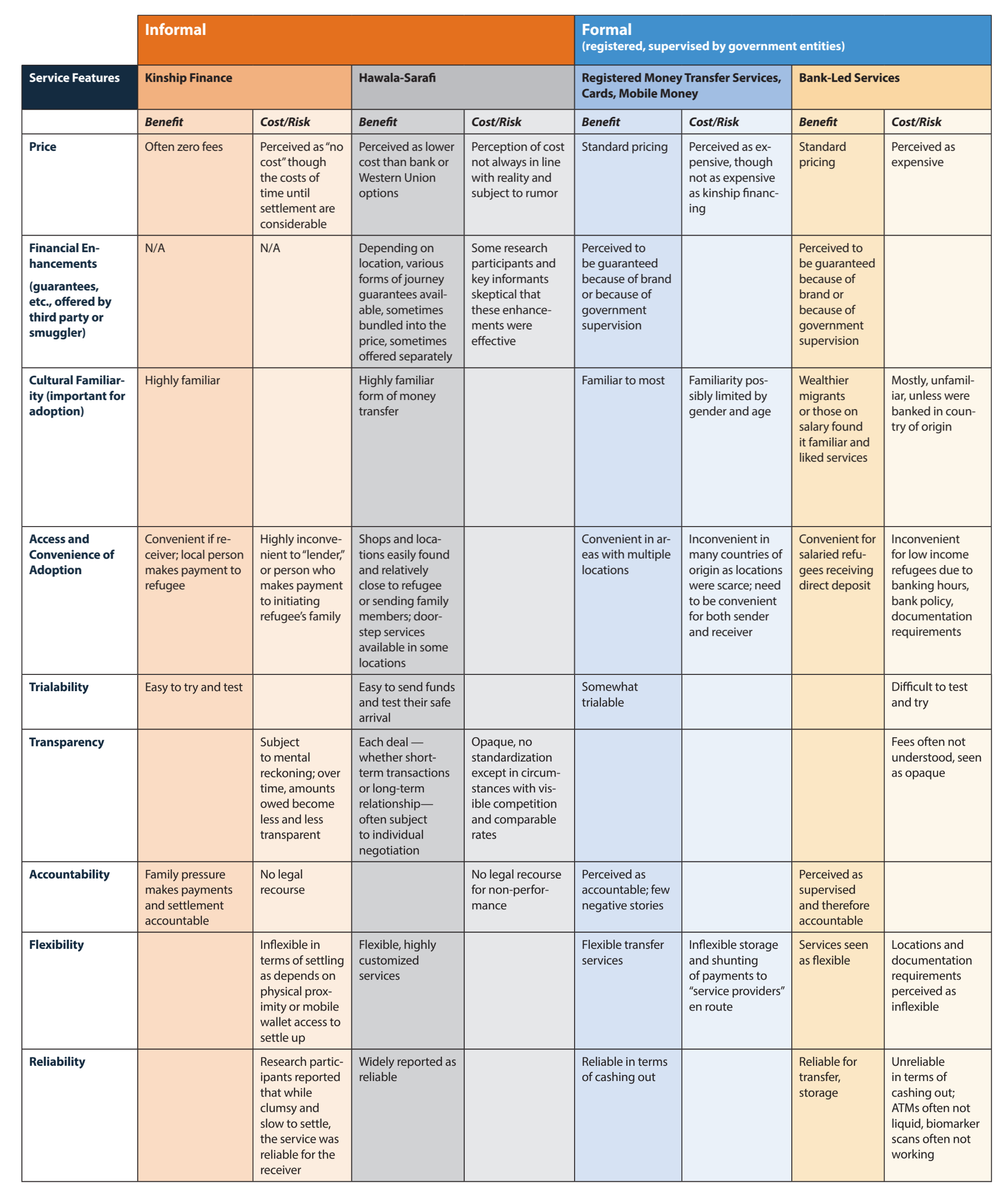

A number of intermediaries are essential for completing the financial transactions that underpin displacement. These include smugglers, money transfer agents such as Western Union, Hawalas and Hawaldars, and sarafs.

A key component of refugees’ financial relationships with smugglers involved the terms of payment and, particularly, the timing. Refugees who employed a pre-pay system risked losing money when the smuggler failed or refused to transport them to the destination to which they had originally agreed.

Few refugees were able to negotiate a “post-pay” system, whereby the smuggler was paid only after successful transit. More common was the “pay-as-you-go” system, whereby refugees’ family members in the country of origin would release a payment to a member of the smuggling network as soon as the refugee successfully completed each leg of the journey.

The financial transactions involved in smuggling suggest a network of formal and informal, licit and illicit systems. An example of the convergence of the systems is some refugees’ purchase of insurance or use of “guarantee schemes” to ensure that the smuggler provided the services agreed.

Social networks and kinship finance are essential for financing refugees’ transactions and shaping relationships. Some refugees even benefitted from “pay it forward” schemes, whereby those who financed the refugee’s journey did not expect to be repaid, knowing that social norms would ensure that the refugee would assist someone else in the future.

Though some refugees attempted to use banks and/or formal money transfer operators such as MoneyGram or Western Union, many shared their perceptions that those systems were less accessible to them than more informal arrangements were. This was at times due to insufficient documentation to satisfy identity requirements, fear of discrimination or harassment, or lack of interaction with the formal financial sector prior to displacement.

Summary of Findings: Humanitarian Assistance as Part of Refugees’ Financial Portfolios

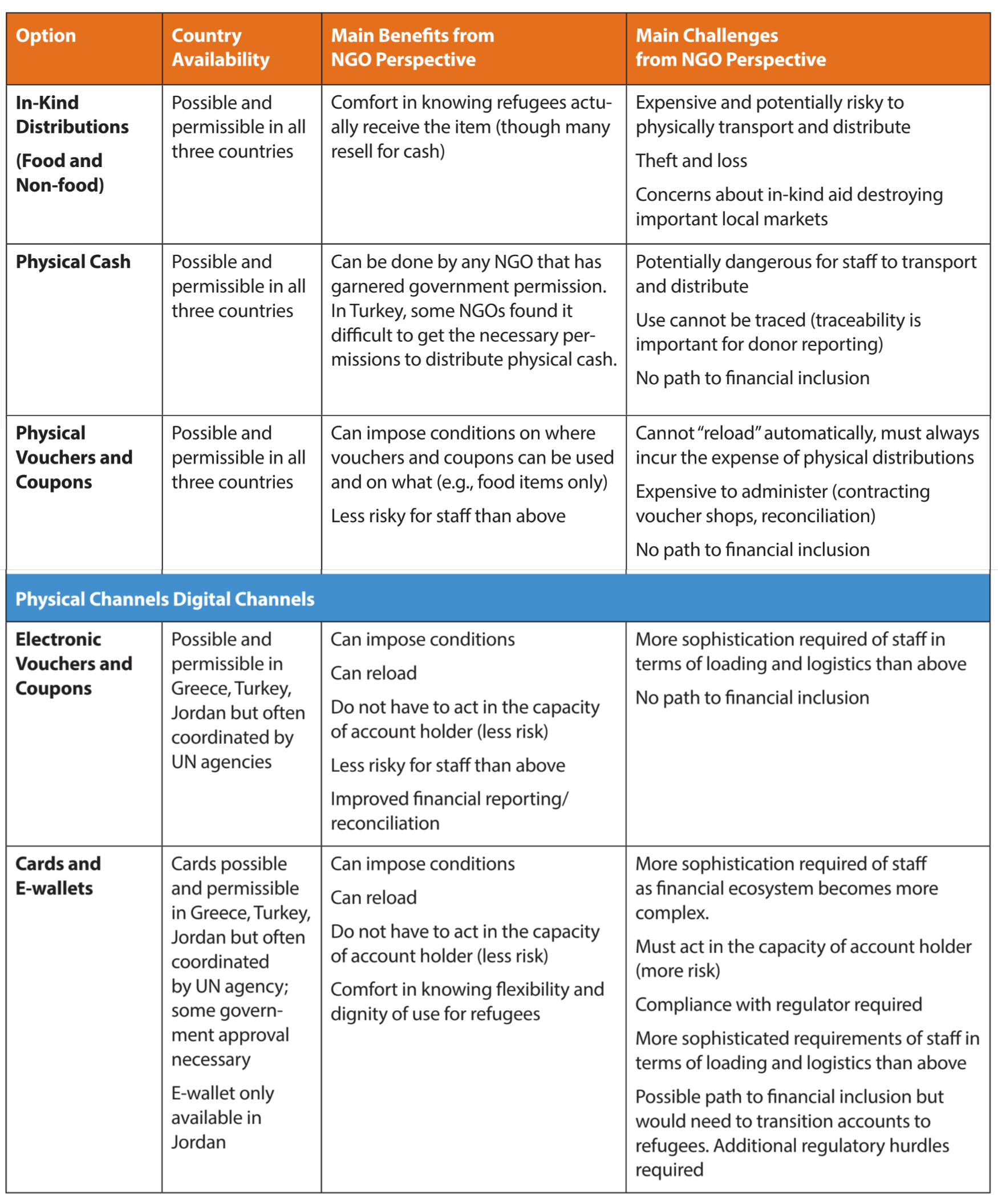

Modes of distribution of humanitarian assistance varied among agencies, including in-kind aid, physical cash, physical vouchers and coupons, electronic vouchers and coupons, and cards and e-wallets.

From the perspective of the NGOs we interviewed, key factors for consideration in terms of the mode of assistance included ease and safety of distributing assistance; traceability of refugees’ spending as a way to comply with donor requirements; ease of reloading or redistributing assistance; ease of imposing conditions on how the assistance could be used; and the existence of a path to refugee financial inclusion.

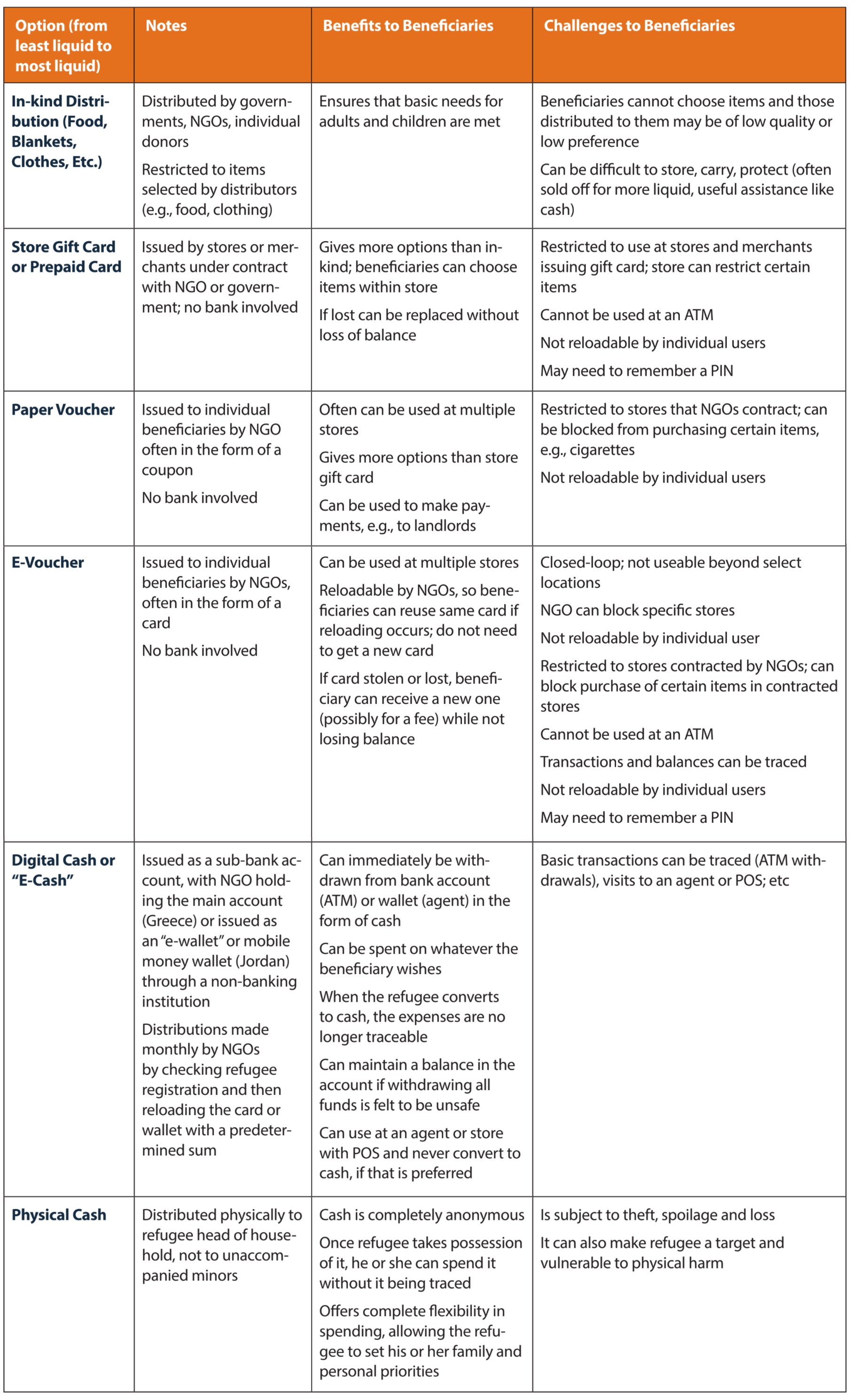

Key factors affecting NGOs’ perspectives on cash assistance included efficiency and scale; familiarity and comfort levels; considerations of financial inclusion; dignity of and flexibility for end users; and traceability and conditionality of funds.

Key factors affecting refugees’ perspectives on cash assistance included flexibility, familiarity, ease of use by different family members based on gender and age, and the dignity the form of assistance may have made possible, particularly when compared to other forms of assistance.

Refugees cited fears of losing eligibility for humanitarian assistance as a reason to avoid using licensed financial institutions for money transfers between themselves and family members or smugglers. Though the alleged linkages between money transfer agents and humanitarian organizations were unconfirmed, refugees nonetheless believed that NGOs could trace their transactions through money transfer agents.

Rumors of such linkages drove refugees towards more informal money transfer arrangements. They believed that less formal institutions were less likely to report their transactions, including deposits from casual labor or remittances from relatives.

Summary of Findings: Identity on the Move

Who one is and the ability one has to prove it turns out to be two of the thorniest problems for a refugee¹. Identity is linked to who can gain permission to work or travel or access systems of protection and assistance. It determines which experiences different systems prioritize over others and how refugees interface with bureaucracies of care.

Identity refers both to one’s own self-identification and its political connotations, as well as to its documentation.

Refugees remarked on their national origin, religion, gender, age, and family status as having been both sources of vulnerability and potential assets during transit. Refugees recurrently noted their perception that humanitarian agencies, legal systems, state security forces, or other actors affecting the refugee experience privileged certain identities over others.

Some refugees were able to highlight certain aspects of their identity—or, indeed, to transform into more favorable subjects—that were perceived to be favorable to the system. For those who could not, identity became a way in which numerous systems created and enforced hierarchical regimes, which they were powerless to change except through deception.

In terms of the documentation of identity, refugees remarked that, at times, not having documented identity allowed them more flexibility in navigating the complex systems of assistance, protection, and care. At the same time, lack of documented identity precluded some refugees from accessing services, particularly in the formal financial system.

Various actors—from money transfer agents to interpreters—assisted refugees in informally navigating identity requirements in order to access the services they needed.

Opportunities for Further Research

- The role of social networks in shaping the refugee experience. Subsequent studies can shed light on how refugees forge and maintain social networks—often cross-border and cross-nationality—while in transit.

- The financial journeys of refugees traveling alone. Much of this research focused on refugees fleeing alongside families or neighbors. Refugees traveling alone appeared to differ significantly from those traveling in groups in ways that merit further research.

- The evolving role of formal financial institutions. As protracted displacement and refugee transit continue, it will become increasingly important to trace whether and how refugees’ interactions with formal financial institutions change over time.

- Host community perspectives. Host community perspectives would complement this analysis, particularly considering the challenging financial journeys many residents of host communities faced in the countries of study.

- The social networks of smuggling. Smuggling is a key node through which to understand refugees’ financial journeys and overall experiences. Further research could examine the social networks of smugglers, including the role of gender and ethnicity in shaping smuggler-refugee interactions.

- Discrimination and harassment of refugees. This study has shown how both the fear of and the reality of discrimination and harassment shaped refugees’ behavior in their financial journeys.

- Longitudinal research on the experiences of refugees over time. Tracing these experiences over a longer time can reveal insights on the evolution of financial journeys, particularly in situations of protracted transit or uncertain resettlement.

Introduction: Research Questions and Overview of Study

The church bells near Piraeus Port in Greece ring every hour to the tune of Manos Hatzidakis’ song “The Children of Piraeus.” Made iconic through Melina Merkouri’s performance of it in the movie Never on Sunday, the song extolls the magic of the port and of the children “who will grow up to be brave for Piraeus’ sake.” At the crescendo, Merkouri sings: “As much as I search, I cannot find a port… like Piraeus.”

For the refugees who sought shelter at the port in 2016, Piraeus was a more reluctant temporary home than the song would suggest. One port worker who gave our research team directions said the refugees were located at hangar 13 and under a bridge, “across the ships to Crete.” On the walk to hangar 13, we pass a sinking vessel named Panagia tis Patmou (The Virgin Mary of Patmos), the protector of ships.

The contrasts in the imagery we encountered appropriately represent the tensions at the heart of this research. On one side, we observed tourists, in white linen and straw hats or denim shorts and backpacks, rolling bags off the cruise ships to Crete. Across the way, a wooden rocking horse toy and two pairs of children’s shoes sit at the edge of an informal tent settlement for refugees, underneath graffiti that reads “No Borders.”

This research project investigates what money and financial transactions can reveal about the journeys and experiences of forced migration. The overwhelming refrain in response to our questions about what refugees brought with them on their journeys was “just the clothes on my back.” It would be a misreading of this project to assume that any discussion of money or assets among refugees negates the vulnerabilities and risks they face along their journeys or disputes their needs for humanitarian and legal assistance or protection. Rather, we examine money as a key node of the displacement experience, fueling transactions among formal and informal actors along the way; determining livelihood options; shaping or restructuring kinship networks; and coloring risks, vulnerabilities, or protective forces available to refugees. Our inquiry highlights these transactions and the power dynamics that unfold among refugees as well as between refugees and formal or informal authorities.

Four specific areas of inquiry emerged during this study:

- How do refugees gather, move, store, spend, and make money along the journey of their displacement? How do their strategies lead to enhanced risk and/or self-protection along the way?

- How do financial transactions structure relationships among refugees, as well as between refugees and formal or informal authorities, such as smugglers,² informal money transfer agents, and formal banking systems?

- How does the humanitarian system—and, in particular, cash assistance to refugees—shape the aforementioned financial transactions and relationships?

- What are the roles of refugee identity—in terms of gender, ethnicity, religion, and family status—and the documentation of that identity in shaping financial transactions, relationships, vulnerability, and coping strategies?

We pursued these questions in a pilot qualitative study that unfolded between July 2016 and April 2017 at multiple sites in Greece, Jordan, and Turkey. Exploratory research in Denmark informed the project, but has not been included in the write-up of our findings at this stage. The significance of these questions is three-fold: First, inquiries about money on the move provide an entry point to exploring the risks refugees face, their coping strategies, and their relationships with formal and informal authorities (Jacobsen 2005, Collins et al. 2009). In this case, money—and the ways in which refugees amass, move, and spend it—is a window into understanding structures of power, access, protection, and vulnerability.

Second, to the extent that financial inclusion literature and practice engage with refugees (El Zoghbi et al. 2017, Hansen 2016), they do so “in terms of integrating customers into an existing digital or formal financial structure,” without focusing on the financial tasks that refugees must perform in order to survive (Wilson and Krystalli 2017, p. 2). As we have written elsewhere, “refugees are not a homogenous block of consumer interests—a market—but a diverse group of people living in urban neighborhoods and formal or informal camp settings. They have far-ranging experiences with cash management, digital technology, and banking, and varied consumer interests” (Wilson and Krystalli 2017, p. 4). This study sheds light on the diversity of these experiences and the needs to which they give rise along the way.

Third, while refugee integration into economies and markets is slowly receiving attention once refugees have arrived at a point of resettlement or aspirational destination (Bevelander and Pendakur 2014, Bakker et al. 2016), to date, little attention has been paid to financial portfolios, transactions, and relationships along the way. Being “in motion”—as opposed to displaced and stationary—is a part of the humanitarian process that needs to be understood more fully. We explore movement not merely as a process of getting from point A to point B, but as a way of life for months or years. It becomes a way of being, and shapes economies (formal and informal) and relationships that surround them.³ By shedding light on those experiences, we examine the implications for humanitarian actors, financial regulators, and other agencies that engage with refugees during their transit.

The rest of the analysis proceeds as follows: Chapter 1 discusses the research methods, including our use of terminology and considerations related to research safety and ethics. The four subsequent chapters correspond to research questions. Chapter 2, which corresponds to the question on how refugees gather, move, store, spend, and make money along the way, provides an in-depth look into the financial portfolios of refugees. Chapter 3, which corresponds to the research question on how financial transactions shape relationships with formal and informal actors along the way, examines the modes through which refugees pay smugglers; the financial intermediaries along the way; and the role of kinship-based, informal, semi-formal, and formal financial systems.

Chapter 4 examines the role of humanitarian cash assistance in refugees’ financial portfolios. Chapter 5, which corresponds to the overarching research question on identity and its documentation, sheds light on how refugees navigate who they are, who they are perceived to be, and who they can prove they are in their constant attempt to access systems of protection and assistance. In Chapter 6, we outline questions for further research.

In addition to this paper, we are releasing a number of outputs related to this research project. These include, among others, (1) a compendium of fieldnotes, aimed at both serving as a teaching tool and providing a less-edited, less-fragmented account of refugee narratives; (2) topic-specific briefing papers, including a discussion of the implications of this research for policy and practice; (3) brief online videos summarizing study findings; (4) an opinion essay on inancial inclusion for refugees; and (5) blogs summarizing findings for different audiences.

📝 This article was originally published as a report by the Henry J. Leir Institute at The Fletcher School of Law & Diplomacy and Tufts University.

Download the original report below ⬇️

Financial Journeys of Refugees: Evidence from Greece, Jordan, Turkey.pdf

Chapter 1. Research Methods, Dilemmas, and Ethics

Knowledge is socially made, and the power dynamics of research shape both the refugee experience and its narration through refugees’ own stories and our retelling of them.⁴ In this chapter, we discuss the terminology we use, our methodological principles and practices, the timing and profiles of our research sites and participants, and some of the ethical dilemmas that underpinned this research.

1.1 Terminology

A tension in this research project reflects the politics of naming and recognition that we are investigating: What do we call our research participants? Labels in the literature have included “refugees,” “migrants,” “immigrants,” “displaced people”—each carrying different meanings and symbolic power (KhosraviNik 2010). We have chosen the term “refugee” because that is the word our research participants overwhelmingly used to describe themselves—as well as the term by which humanitarian actors referred to them. In this context, “refugee” does not necessarily refer to someone who has the formal, legal recognition of this status.

The politics of labeling also complicate the framing of the spatiality of the refugee crisis. Labels have included “the Mediterranean refugee crisis,” “the European refugee crisis,” or “the Syrian refugee crisis” (Linden-Retek 2016). We are conscious that this is not a single crisis that unfolds in a discrete, bounded geographic region. For this reason, we focus our analysis on the specific sites of research, where possible, rather than constructing an imagined, cohesive space of a singular crisis.

1.2 Methodological Principles and Practices

Our methodology reflects key tenets of feminist research (Wibben 2016, Lykes and Coquillon 2007) and interpretivist social science. As articulated by Lisa Wedeen (2013), these include a

- commitment to understanding how knowledge is situated and entangled in power relationships;

- curiosity about how categories are socially manufactured, not existing “always already,” waiting to be discovered;

- ejection of strictly individualist assumptions in favor of a recognition of more complex social relationships and modes of agency; and

- close examination of language, symbolic systems, and meaning-making. To apply these commitments, we relied on the Lean Research approach for conducting research in vulnerable settings (Armstrong et al. 2015).

The Lean Research Framework articulates principles and practices for conducting rigorous, respectful, relevant, and right-sized research in vulnerable settings.

Throughout our analysis, we acknowledge that refugees do not merely exist; they also have to do refugee-ness. Like all narratives—and especially narratives of injury and vulnerability (Brown 1993; Jones 2009), stories of displacement invite and require performance (Wedeen in Schatz 2009; Jones 2009). Performativity here refers to the iterable practices (Derrida 1998) that “constitute individuals as particular kinds of social beings or subjects” (Wedeen 2013, p. 88). Both in this methodology section and throughout the report, we note the ways in which these performances shift across contexts and audiences (Scheper-Hughes and Bourgois 2004).

1.3 Overview of Research Participants

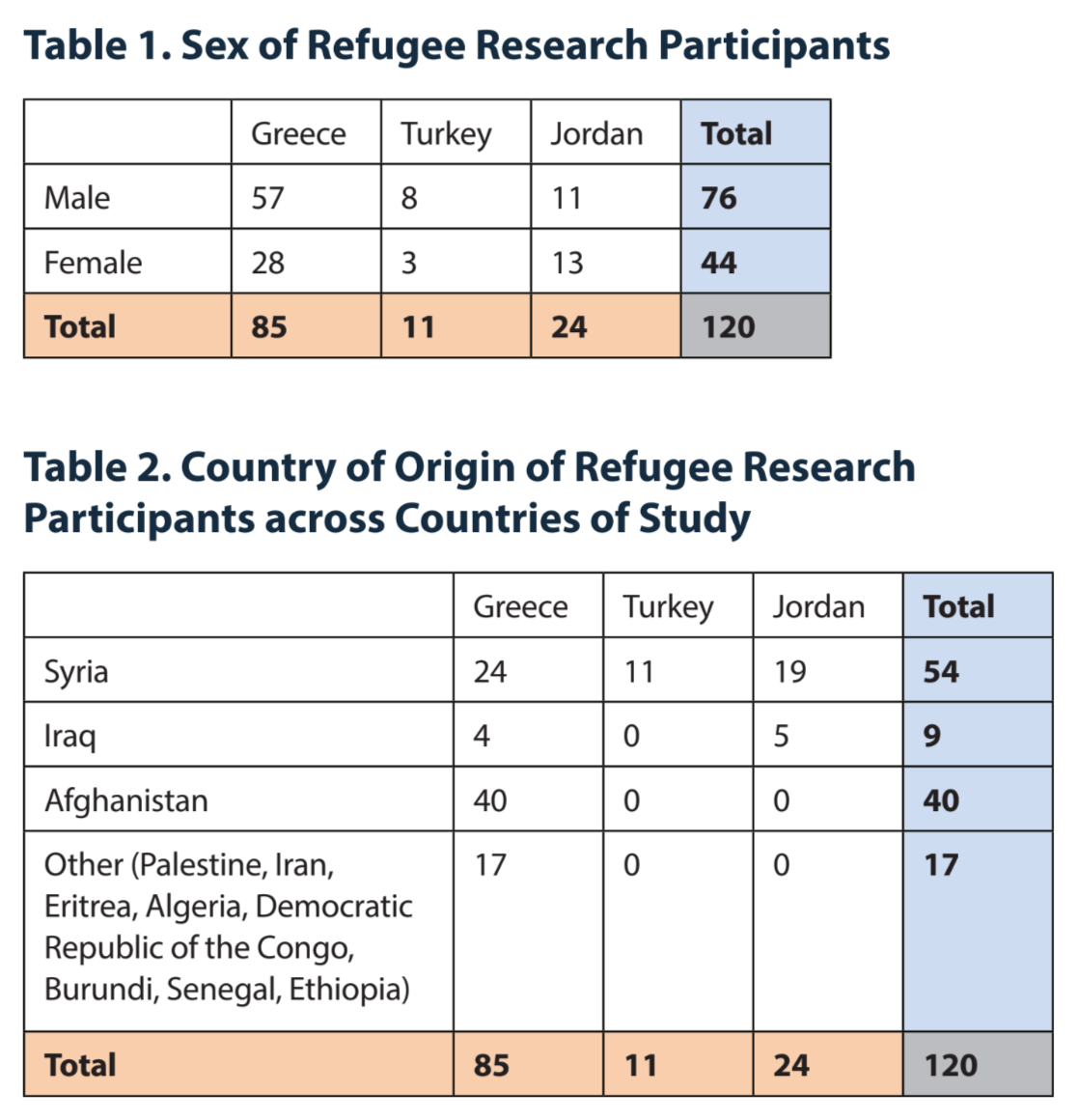

The breakdown of refugee research participants by sex and ethnicity across our three country sites can be seen in Tables 1 and 2. Consistent with our approved research protocol, we did not interview children, defined in our countries of study as individuals under the age of 18. As the tables indicate, we deliberately did not limit our refugee participants to certain points of origin or ethnicities (e.g., Syrian refugees) and, instead, engaged with a diverse group of participants who mirrored the languages spoken by our interpreters and research team (see below). This engagement highlighted important themes regarding perceived hierarchies within and among refugees, discussed in Chapter 5 of this report. In addition to the refugee research participants, we engaged with 25 key informants, described in the next sub-section.

1.4 Overview of Research Locations

Collectively, refugees viewed our three countries of study differently, seeing some primarily as countries of transit (Greece) and others as temporary destinations that sometimes evolved into more permanent places of settlement (Jordan, Turkey, and—to an extent—Greece).

In all three countries, members of the research team interacted with refugees in a variety of settings, including refugee camps (e.g., Elliniko camp in Greece) and informal refugee settlements (e.g., under the bridge in Piraeus Port in Greece). Members of the research team also engaged with refugees who had dispersed within urban or semi-urban areas without being part of a formal or informal refugee settlement (e.g., certain refugees in Sanliurfa, Turkey; Amman, Jordan; and Athens, Greece).

The numbers of research participants across our sites were uneven, reflecting the availability of funding, research team members, interpreters, and time. Acknowledging the value of refugee testimonies even at sites at which we were able to collect few narratives, we have opted to include all three country cases and highlight gaps and areas for further research, where relevant. Each refugee testimony is cited in connection to the country in which the interview took place. Elements of refugees’ experiences varied depending on their location and the juncture in their journey, and we note any variations in the analysis.

1.5 Research Timing, Analysis, and Subsequent Fieldwork

The timing of interviews affected the narratives we were able to access. The first cycle of fieldwork took place in July and August 2016. By July 2016, many of the formal border crossings to Central and Western Europe had closed or passage through them had slowed considerably. This meant that many of the people we interviewed who had previously considered themselves to be in transit were now fairly immobilized in the country in which we encountered them (Digidiki and Bhabha 2017, Brooks 2016). As one key informant said in Greece in July 2016, “There is no money here. Most people don’t have the hope they can leave Greece at this point. If you have money, you are already gone.” A different key informant in Greece in July 2016 echoed, “Accurately speaking, nobody is in transit [in Greece] anymore. The formal border is closed. Some—few, not many— have accepted that this may become their country. Most people still want to leave and think they will leave.”

A preliminary analysis workshop by the research team in September 2016 identified areas for further inquiry. We pursued some of these during subsequent fieldwork in Jordan and Greece between December 2016 and April 2017.

1.6 Engagement with Research Participants

The primary modes of engagement with research participants included interviews with key informants and refugees and observation at the above sites. Key informants consisted of personnel interacting with refugees in numerous professional capacities. These included the delivery of humanitarian assistance, facilitation of money transfers, provision of legal services and counseling for asylum, and offering of other programming to support refugee integration into communities. Certain key informants had also supported state agencies in verifying refugee registration information, and thus shed light on the eligibility requirements for receipt of certain types of assistance. The engagement with key informants reflected a feminist commitment to “studying up” (Nader 1972) and exploring the narratives of those with power to shape refugees’ experience, instead of placing narrative expectations squarely on refugees who experienced various forms of vulnerability throughout their journeys (Theidon 2012).

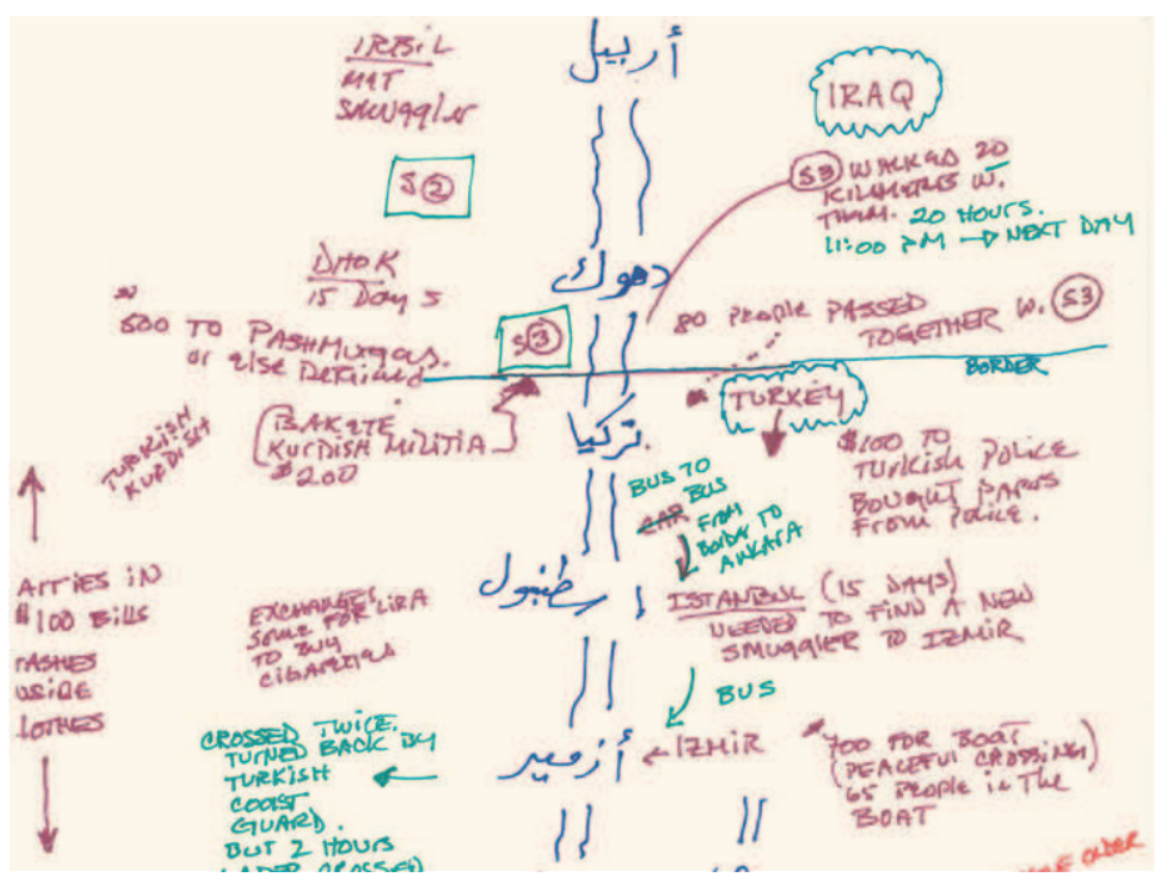

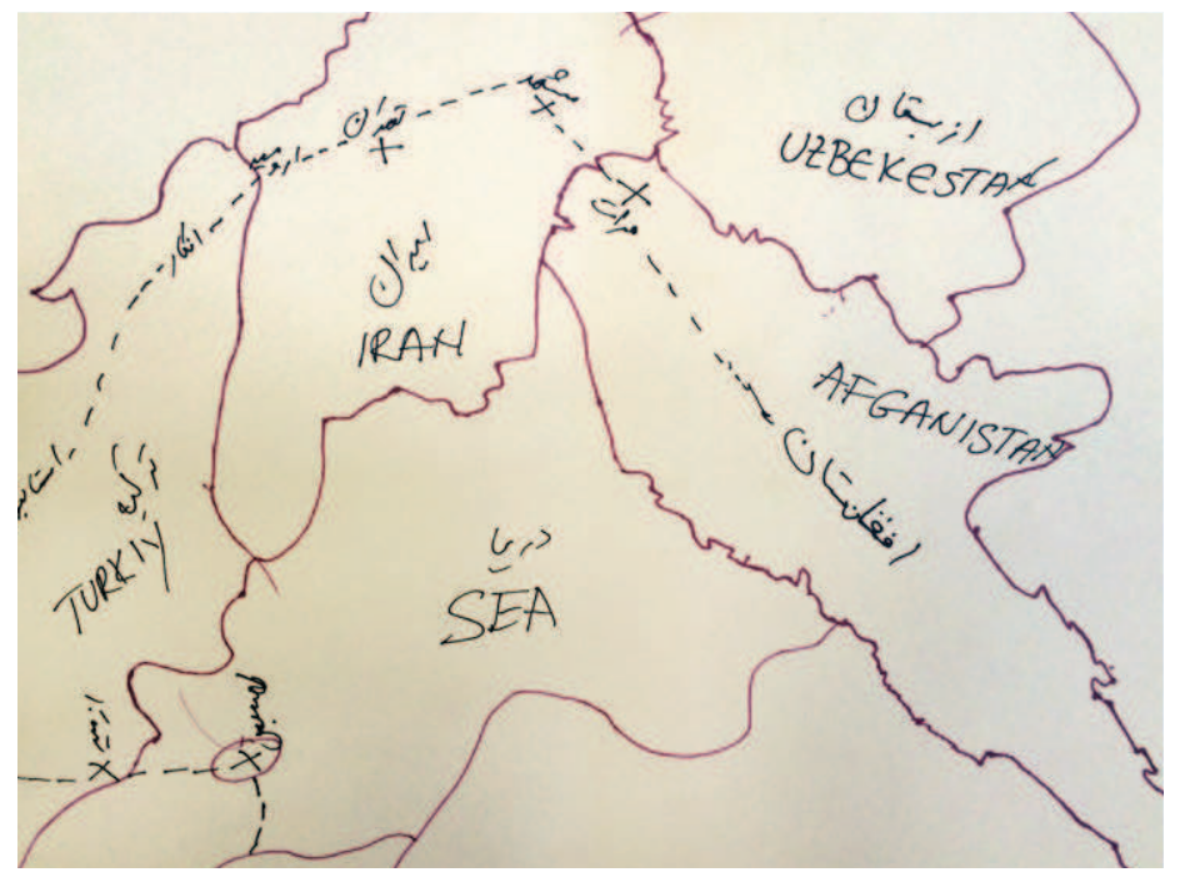

Engagement with refugees primarily consisted of semi-structured interviews as well as observation of settlement sites. Certain refugees also participated in mapping their journeys, drawing on participatory cartography methodologies from Robert Chambers (2006) and Elisabeth Wood (2003). The maps provided entry points for conversation on points of risk, vulnerability, and protection in refugees’ journeys, as well as their interactions with authorities. As maps are useful not only as entry points of conversation but also as analytical tools, some are displayed as illustrations throughout this report.

During observation, we noted, among other factors, the physical setup of the site, the available facilities, the presence of humanitarian actors or other professionals and their interactions with refugees, the ease of movement between the settlement and other areas in which refugees spend time, and the ways in which refugees organize their daily lives during displacement. Members of the research team also had the opportunity to observe selected non-governmental organization (NGO) focus groups and meetings with refugees at field sites. Reflections from those events, particularly with regard to hierarchies of humanitarianism, are included throughout the analysis.

1.7 Effects of Gender, Ethnicity, and Language on the Research Process

Our research methods affected the narratives to which we had access. For example, it was often difficult to talk to women alone, without the presence and/or permission of male family members or other men in the women’s network (such as neighbors). Many of the stories of women were often mediated through the presence of men, who at times dominated the conversation or answered on women’s behalf.⁵ As we remarked in our earlier discussion of luid performances of refugee-ness across contexts, the narratives that refugees feel comfortable producing for researchers may differ from those they feel compelled to perform in front of other refugees (even when—or especially when— those are their family members, neighbors, or acquaintances). We sought to address these issues by engaging with female research participants in women-only spaces, or in gender-segregated community groups, as well as by talking to women who were traveling alone or in groups of other women and by noticing the shifting dynamics and narratives. The languages our research team members and interpreters spoke—Arabic, English, Farsi/Dari, Greek, Turkish—affected the narratives to which we had access.

1.8 Editing and Analysis

As Helen Bassini writes, “The qualitative feminist research journey is messy, non-linear, and inductive” (Bassini in Wibben 2016, p. 181). We used an inductive approach to code data both at our formal analysis workshop with our full research team and during subsequent opportunities among the co-authors of this paper. Where possible, we have opted to quote extensively from the stories of refugees themselves. Consistent with our approved research protocol, we have chosen to abstract or omit entirely certain identifying details pertaining to people’s identities or to places. We have also chosen to quote from the field notes of our research team in situations where quoting a refugee directly is not possible or where the researchers’ observations provide additional context.

Throughout the write-up process, we paid close attention to narratives themselves as a financial resource and a form of financial performance.⁶ Chapter 5 explores how refugees felt compelled to produce shifting performances of need or vulnerability depending on what the particular system (whether kinship finance, humanitarian protection, or other) expected of them. In examining these narratives and performances, we explore not only the stories refugees produce, but also the systemic pressures, expectations, and inequalities with which they are engaging.

The process of editing and analysis has prompted us to reflect on the politics of knowledge production. Echoing Malkki (1995, p. 56),

The problem of representation is, at this point, tied to that of representativeness. For ethnographic generalizations are inevitably supported with citations of particular events and utterances. But which particularity is to be privileged? Which specific statement will be quoted? Does one always omit “freak utterances,” comments that were heard only once, in favor of recurring statements?

We wrestled with Malkki’s questions and acknowledged editing as its own form of instrumental fragmentation—indeed, of violence—to the narratives of refugees. While we acknowledge the necessity of putting narratives in conversation with each other and of making selective choices about how to pair refugees’ voices with our own analysis of them, we have also sought to preserve the integrity of refugees’ stories as holistic narratives in themselves. To that end, complementing the release of this paper, we will be launching a series of lightly edited ieldnotes. These consist of refugee narratives edited for security (i.e., removing identifying information) and told in the voices of the refugees who shared their stories with us.

Finally, throughout the write-up, we note tensions between what emerged as common stories versus exceptional narratives. As we discuss in greater depth in Chapter 5, we build on research by Didier Fassin and Mariella Pandoli (2010), Miriam Ticktin (2011), and others to illustrate how the humanitarian system operates under a logic of exception and “how compassion acts as a form of policing, choosing a few exceptional individuals and excluding the rest” (Ticktin 2011, p. 127). This system of exception shapes the narratives that refugees share with researchers, humanitarian agencies, legal groups, and other key actors in the migration crisis. The political economy of trauma (James 2004) rewards certain scripts of exceptional hardship over other, more common narratives. In the context of our research, this tension took many forms: When discussing their strategies for liquidating assets into cash prior to their journeys, the most common narrative among refugees involved the sale of livestock, homes, and household appliances, as we discuss in Chapter 2. In the case of one research participant, however, it involved the sale of a child; in the case of another, it involved encouraging a daughter to marry earlier to both make the household smaller (thus reducing its financial needs) and to use bridewealth as an asset that could finance migration. Illustrating the range of refugee journeys, while being mindful of the reinforcement of particular narratives at the expense of the marginalization of others, has remained a challenge throughout the research and analysis process.

1.9 The Ethical Dilemmas of Refugee Research

Throughout this chapter, we have discussed some of the ethical dilemmas we have faced and some of our strategies for engaging with them. Though a fuller discussion of the ethical dilemmas this study has raised is the topic of a separate publication, and this theme has already received extensive attention in the literature (Jacobsen and Landau 2003, Mackenzie et al. 2007), three additional dilemmas are worth briefly highlighting here.

First, we navigated concerns around access and “research fatigue” (Pascucci 2017) due to an oversaturation of researchers, journalists, and humanitarian practitioners, all asking questions to the same groups of refugees. This was coupled with perceptions among refugees that participating (or refusing to engage in) a study may affect their access to humanitarian assistance, protection, or other benefits. These dynamics were further exacerbated when refugees were asked to repeatedly narrate experiences of physical violence they or their loved ones suffered in their home countries or along the journey of migration (Theidon 2012). As Elissa Helms writes in her exploration of the obligations that we impose on victims of violence to narrate the harms they suffered, “Sometimes allowing victims to remain silent and anonymous is a way to allow them to reclaim dignity and a sense of self” (Helms 2013, p. 240).

We attempted to engage these concerns in a number of ways. These included:

- opting not to conduct research in areas in which large research studies were underway (such as Zaatari refugee camp in Jordan);

- receiving feedback on the relevance and respectfulness of our initial study approach from humanitarian practitioners, researchers, and interpreters who worked in our geographic and thematic research areas;

- iteratively revisiting our semi-structured qualitative interview protocol at the end of each day to incorporate refugees’ and interpreters' feedback on our approach;

- accessing all sites independently of the practitioner organizations that supported the research, knowing that being seen in any affiliation with them might affect refugees’ willingness to participate in the study; and

- opting not to ask direct questions about the violence that may have motivated refugees’ light from their point of origin, or that they encountered along the way, and clarifying this to all potential research participants. Where stories of violence—physical, structural, and systemic—emerged in the research process, we documented them accordingly herein.

Second, we remain aware of how the process of research and documentation may undermine coping strategies that are essential to refugees’ survival. Here, too, we follow Malkki (1995, p. 51) and Feldman (1991, p. 12):

I would emphasize that in all of this, the success of the fieldwork hinged not so much on a determination to ferret out “the facts” as on a willingness to leave some stones unturned, to listen to what my informants deemed important, and to demonstrate my trustworthiness by not prying where I was not wanted. The difficult and politically charged nature of the fieldwork setting made such attempts at delicacy a simple necessity; like Feldman, I found that “in order to know, I had to become expert in demonstrating that there were things, places, and people I did not want to know.”

Finally, the political economy of suffering⁷ that governs storytelling in vulnerable settings (Fassin and Rechtman 2009) affected both refugees’ willingness to participate in our study and the narratives we accessed during our engagement. We acknowledge that power imbues research relationships—in this case, visibly unequal power. In the end, we were—and remain—part of the hierarchies that elevate certain narratives while marginalizing others. Rather than denying this subjectivity and power, we have attempted to explicitly convey it through our writing.

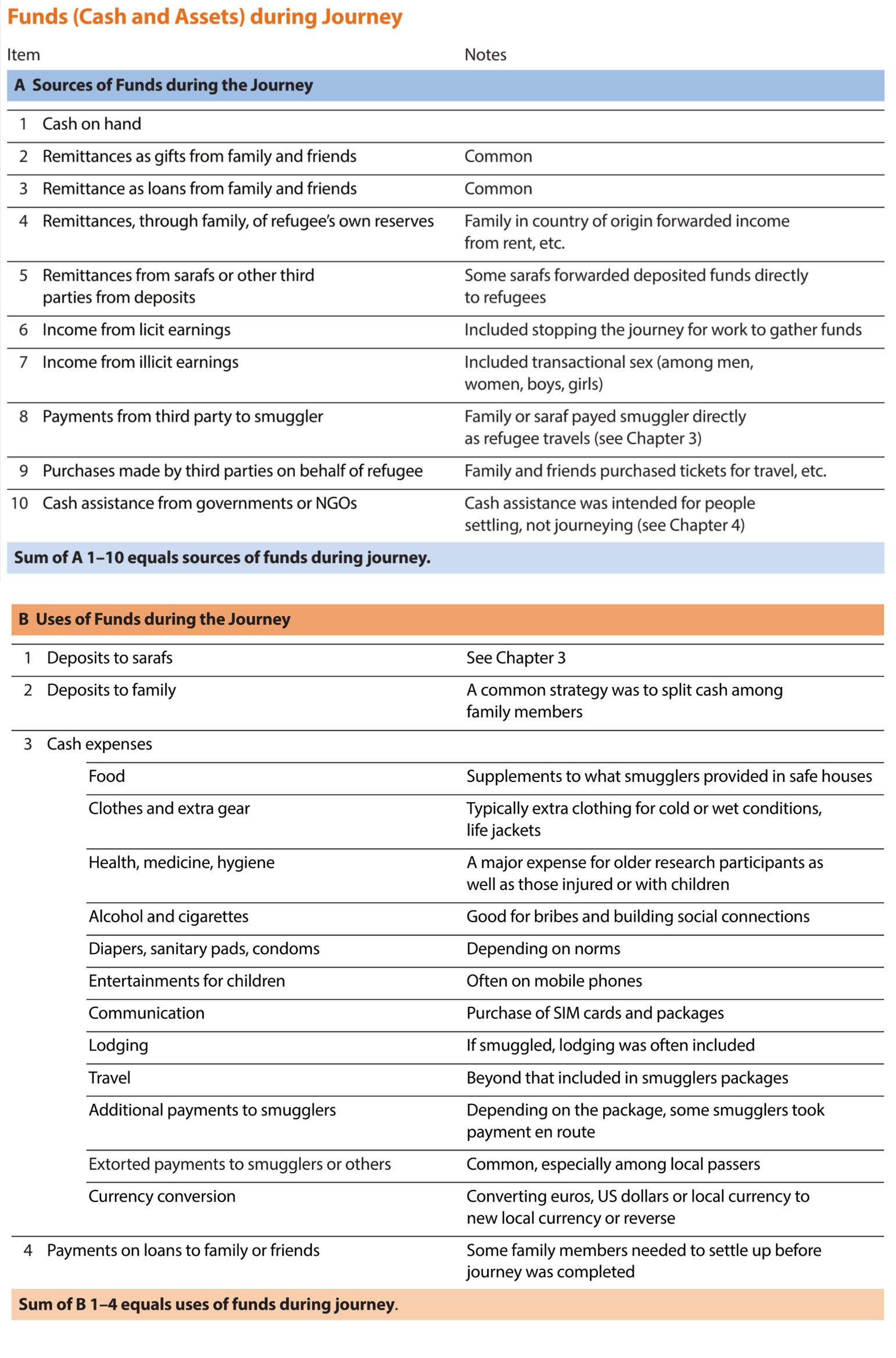

Chapter 2. The Financial Portfolios of Refugees: Amassing, Carrying, and Spending Money on the Move

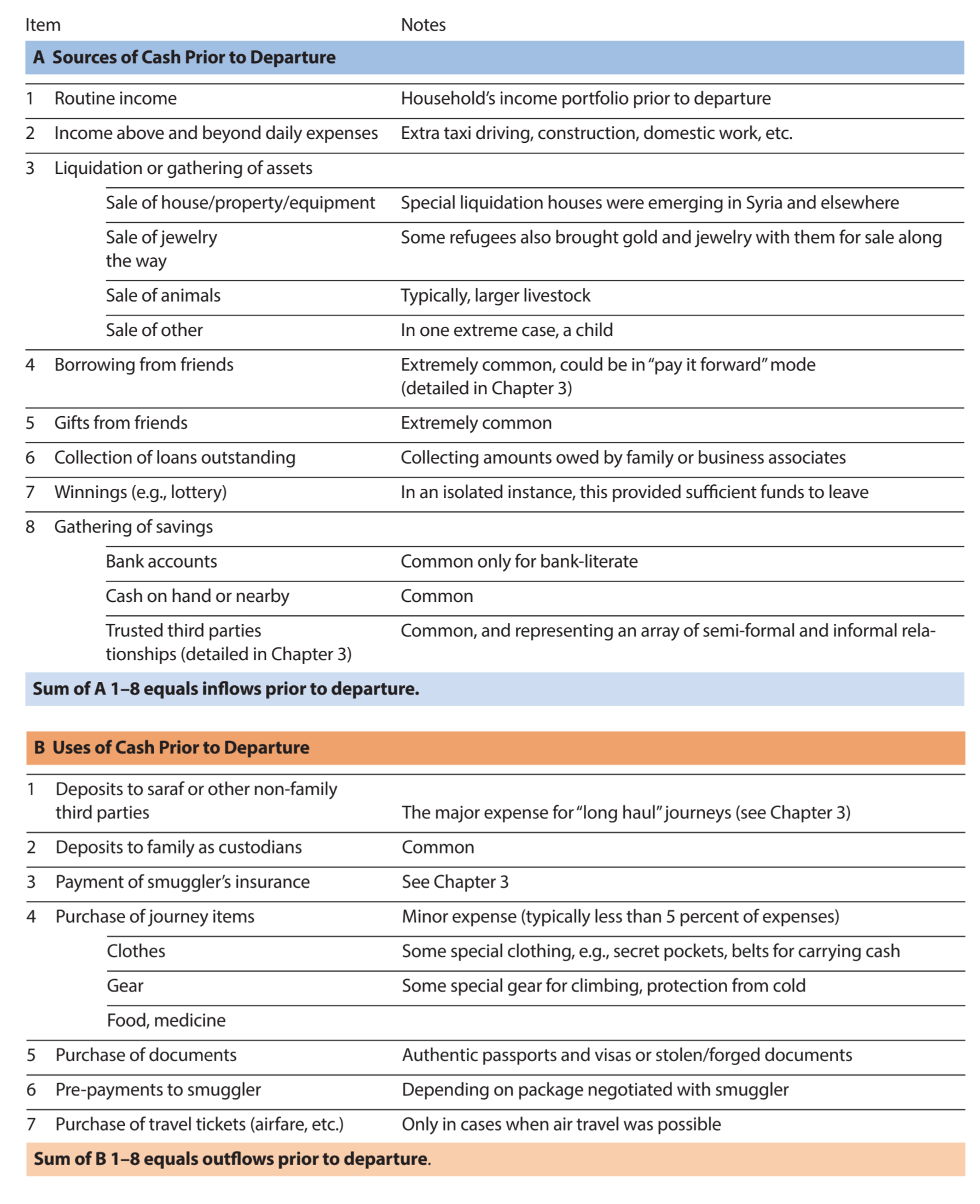

Money is an essential component of refugees’ journeys, not only for financing daily expenses (such as food, shelter, diapers, etc.), but also for facilitating relationships with key actors along the way, as we examine in depth in Chapter 3. In this chapter, we begin by exploring the main sources of funds that refugees use to finance their journeys. A key finding is that even the most sudden displacement requires financial and logistical preparation—and when that is not possible, refugees face intermittent journeys, with long pauses between stints of movement and possibly higher risks along the way. Preparations include selling assets, withdrawing any available cash from accounts, borrowing money from kinship networks, and setting up financial mechanisms to access funds along the way. After discussing these preparations, we take a look at the costs of these journeys, acknowledging that costs varied widely over time and from refugee to refugee. Finally, we examine refugees’ strategies for gathering money during their transit, such as borrowing (profiled in depth in Chapter 3) and working along the way.

2.1 Prior to the Move: Financial Preparation for Departure

Though the exact moment at which a person embarks on the migration route is usually triggered by a defining, often sudden, event, these journeys require financial and logistical preparation. The majority of research participants articulated having considered leaving their point of origin before the incident that led to their eventual departure.

These preparations consisted of:

- liquidating assets to secure cash to carry during the journey;

- depositing cash with kinship networks to transfer to refugees during transit;

- soliciting or borrowing cash from kinship networks to finance transit, where possible;

- collecting outstanding debts; and

- identifying smugglers and money transfer agents, where needed, and negotiating terms and insurance policies.

In liquidating assets to secure cash, research participants narrated selling land, homes, or livestock, when possible:

We all sold things, whatever we could… We just wanted money immediately to pay to leave.

—Syrian woman in Greece

We sold everything: refrigerators, washing machine, everything. Sold the house, closed the bank account. Liquidated. Anything to get here.

—Iranian woman in Greece

It was a black day when I had to sell my wife’s gold.

—Iraqi man in Jordan

When preparations for departure where protracted, as was the case with some research participants fleeing Afghanistan or certain African countries, they may have lasted years:

In Nigeria, you cannot sell your family’s land because it belongs only to the family. If you sell it to someone else, both will have problems—it’s the bad eye of the ancestors. So, there is a dawlet system that allows us to lend land in exchange for money. People can borrow your land if they give you money, but they cannot build a house on it; they can only bring in their animals, harvest crops. My brother lent the land to a cousin for two years, and he used that money to go.

—Nigerian woman in Greece

By contrast, when preparations had to be brief due to imminent departure, as was the case with some research participants fleeing Syria, sales took place over a matter of days and often resulted in substantial losses over what peacetime sales could have been:

I sold my house for €5,000, but I believe before the war it would have been worth €50,000. I sold my motorbike for €1,000 and borrowed €4,000 from my brother.

—Syrian man in Greece

For those who were not able to prepare extensively and had to leave suddenly, financial readiness depended on the possibility of borrowing money from family members and friend networks (either at the country of origin or after arrival in other countries). Sometimes, this involved even borrowing money from strangers:

We were running when we left, and we did not have a chance to bring anything. We just took our ID cards and passports. Our livestock, possessions, everything we left behind was lost. We left with only our clothes. At the airport, good people offered us money for tickets.

We went to people that we know to get help, saying that we wanted to come to Jordan. Those people bought tickets for us. We did not know anyone in Jordan. We came and immediately applied to UNHCR. We asked Iraqis that we know what to do.

—Iraqi man in Jordan

The journeys of refugees who had less time to prepare financially (or who had fewer assets to liquidate) were often more staggered and characterized by long pauses along the way to find work and secure a temporary livelihood to finance the next leg of the journey. As one key informant said about refugees who were stuck in Greece without being able to move forward in July 2016, “Refugees who are still in Greece haven’t found a smuggler or don’t have money to pay him. In that case, you look for agricultural work. It’s not like Turkey, where it’s relatively easy to find labor for refugees. Because of the financial crisis, both the laws and the jobs are harder here.” Refugees themselves reported having to pause their onward journeys towards Europe to amass more cash to finance them. An excerpt from a researcher’s fieldnotes regarding a conversation with an Afghan man in Greece elaborates:

His family sold a house to pay for the trip. He brought 500 dollars with him for water and food along the way. “That was not enough. I had to work. There was no work in Iran for people like me. Too dangerous. ” He stopped in Turkey for 8 months, where he worked construction.

—Researcher’s fieldnotes from a conversation with an Afghan man in Greece

If one were to analyze a refugee’s cash flow from an accountant’s point of view, our field notes in aggregate could be represented in the form of a “statement of sources and uses of cash.” Table 3 below summarizes the funds gathered prior to departure, as well as their uses. Subtracting item B from A would indicate the funds available for the journey itself.

2.2 Costs of Transit

How much money does a refugee need while on the move? In over 100 conversations with refugees, we found no cost structures identical. Instead, the cost of moving from a refugee’s country of origin to Europe fluctuated, as did the costs of moving through countries of transit, some of which became countries of endured settlement or “reluctant destination” over the course of our study. Key informants affiliated with the Balkan Center for Migration and Humanitarian Activities, which tracked monthly costs of border crossings, confirmed this fluctuation in prices. Even over the time of our research (July 2016-April 2017), prices varied by thousands of Euros from month to month. Factors that affected the price luctuation included (1) family status, including how many children were part of the group; (2) territories people had to pass through and who controlled them; (3) mode of travel, such as the combination of taxis, trucks, planes, or feet needed to cross borders; (4) documents refugees needed smugglers to procure or replace for them; (5) political developments that facilitated or foreclosed certain routes of passage. As one key informant said in Greece,

When we say the borders are closed, we mean the formal border. As soon as the formal border [from Greece to elsewhere in the Balkans] closed, the smugglers were in great business. Golden jobs! The prices vary, and they fluctuate depending on these events. To give you an example, this week it seems to cost 1,800 euros to get from Greece to Austria. But this depends on who has to mediate, who is helping along the way, whether you’re taking trucks or taxis or walking, whom you have to bribe. There is all-inclusive smuggling, and smuggling à la carte, and everything in between. Problem is, you don’t know what you’re getting.

—Key informant in Greece

We deliberately did not initiate direct conversations with refugees about the amount of money they carried with them or their costs during transit. However, as refugees began to volunteer this information themselves during our conversations about preparing to flee, we discovered that discussing money on the move was a less contentious topic than we had anticipated. Many refugees—particularly men, as we discuss in Chapter 5—were happy to shed light on the transactions underpinning their experiences of forced displacement. Some had kept detailed records; others recalled from memory. This information is significant because the amounts of money refugees were required to spend during their transit corresponded to financial preparations they had to make prior to departure, kinship networks they leveraged before and during their transit, and risks they faced along the way. Below, we preview some indicative costs for various routes.

From Afghanistan to Turkey or Greece and Beyond.

For those who had to endure the hardships of travel largely characterized by trucks and buses, a trip from Afghanistan to Greece could cost $7,000. If Turkey (rather than points in Europe) were the destination, the cost could lower to $2,000 per person or less. A refugee from Afghanistan describes such a journey to Greece:

My children are seven years old, five years old, and three years old—all boys. The whole trip from Afghanistan to Greece lasted two and a half months. One of the most frightening legs of the journey was crossing from Iran to Turkey, across the Zagros mountains. It was 15 hours by foot. A loose boulder fell on my husband, crushing his foot. Some young Afghan men, traveling alone, helped him by spraying some “soccer spray, ” getting him up and helping him limp through the climb.

Often, along the journey, people would ask us for things. Give us your phone. Give us your money. We had no idea who these people were or if we should pay attention to them, and frequently we did give them money just to get rid of them. The problem was not our smuggler; it was everyone else. We were constant targets.

We had only one main smuggler, elder smuggler, from Kabul to Van, but were passed along by 25 different local smugglers all across Iran. We made no payments to these smugglers—only to the elder, and only then when we reached Van. It cost €2,000 to travel from Afghanistan to Turkey (Van).

—Afghan woman in Greece

Refugees’ ability to negotiate prices was also critical in determining costs. In areas in which smugglers were ubiquitous and prices more transparent—for example, in Nim - rooz Province in Afghanistan, border crossings between Syria and Turkey, or ports in eastern Turkey—refugees could choose a smuggler based on price. However, in areas in which smugglers were fewer or not as identifiable, a good price depended on an individual’s ability to negotiate. As one Afghan key informant noted, individual negotiating skills were key to getting a good deal: Jor amad was key, meaning the way in which parties come to terms with one another. Each arrangement appeared bespoke, even when travelers had time to shop for the best deal. Pricing was somewhat consistent in places where there existed an informal “office of transactions,” a physical place where a refugee may visit and obtain prices. Research participants reported such places in Athens, the Turkish western seaboard, and parts of Syria. Pricing was also more consistent when competition was apparent.

The following are three legs of a journey and costs of each.

From Afghanistan to Greece, typical costs for traveling via truck, buses, cars and boats in winter of 2016 ran something like this: $1,500 from Afghanistan to Pakistan; $1,000 from Pakistan to Iran (just crossing border); $3,500 from Iran to Istanbul; $1,350 from Istanbul to Athens (via bus, boat, and ferry), for a total cost of $7,350. Smugglers provided food, safe houses, and transportation.

—Afghan man in Greece

Smuggling represented the single largest cost of the refugee journey, and fees included travel, shelter, food, documentation, and bribes. Though smuggling itself is discussed in greater detail in Chapter 3, a researcher’s fieldnotes from a conversation with an Afghan man describe how he allocated costs between travel-related expenses and cash-on-hand:

It costs 10,000 Afghan dollars (equivalent of about $200) to get to the border of Iran per person. He said this is a less formal part of the journey—in his group, only 4 of 17 made it across the border without getting sent back. On the border between Afghanistan and Iran, he said “smugglers line up like a taxi stand—you just get off the bus and choose one. ”… He said he had no passport because it would have been too expensive to get a real passport. He reports that it cost about 500–500–600 to get across the border into Iran, plus he carried another $200 of pocket money. He stayed in Iran for only about 10 days, then crossed to Turkey for about $1,500, which was the price of being smuggled at the time. He stayed in Turkey for a few months, working in construction, but he didn’t get paid properly. He was never able to save money, only to live day by day. His original plan was to save enough money in Turkey to pay for a smuggler into Greece by himself. Because he was not able to save enough, he called his family, and they pooled more money together and called the same smuggler that had gotten him into Iran, and they paid him $1,600 to get him from Turkey to Greece. He brought about $300 with him to Greece.

—Researcher’s fieldnotes from conversation with Afghan male, Greece

The ratio in this story, of roughly 15 percent cash for day-to-day costs versus smuggling costs of 85 percent, held true for most interviews, even though the total costs changed markedly based on the distance traveled, the duration of the journey, and mode of travel.

Families could find better prices, but their hardships would multiply. An excerpt from a researcher’s fieldnotes describes part of a family’s particularly punishing journey. It cost $3,500 per person in hard cash, but cost considerably more in adversity.

From Kabul, they traveled for 24 hours by bus, passing through Kandahar. They were afraid, having heard that Daesh stops buses along the way looking for Shias passing through. They spent two nights in a border town, and then made the journey across the border into Pakistan. This journey took them 28 hours, sometimes by car and other times by foot. There were about eight families traveling together, along with 13–14 single men. In Pakistan, they were sometimes followed by the police, but once they reached the smugglers’ safe houses, the police no longer bothered them. The safe houses in Pakistan belonged to families who had some connection to the smugglers. They had no food that first night and just enough cash to buy some bottles of water and some cookies that they gave to the younger travelers. The smugglers had advised them not to carry cash, because of thieves, and they were not allowed to leave the safe house to access their money through a saraf [money middleman— see Chapter 3].

After spending the night, they departed at 8 AM to make the journey into Iran. This involved a 13-hour trip, once again traveling by car and foot, mostly through desert. They traveled at high speeds in the back of large, open-top vehicles—every inch was packed, and the vehicle carried 70–80 people. The young men sat around the perimeter of the vehicle, holding onto dear life at dangerous speeds, and the women and children sat towards the middle, holding onto their young children. The men sitting at the perimeter sometimes fall out of the vehicle and are left behind in the desert.

From Syria to Greece and Beyond.

Though a shorter journey end to end, departing Syria for Greece could also be expensive—up to $2,500 per person in the spring and early summer of 2016—with the major expense entailing movement across variously controlled territories within Syria itself. The few who were able to drive to the border to Turkey at Idlib reduced their costs to being smuggled across a single border.

A typical trip from Damascus to Greece in the spring of 2016 could range from $1,000–$3,000, depending on how many internal borders were crossed in Syria. Each major segment was cut into smaller segments based on which areas were controlled by Syrian forces and pro-government militias, by Daesh, or by opposition forces, foreign and domestic.

Routes through Africa.

For routes through Africa, costs again varied, with country of origin and route dictating aspects of costs but not accounting for all variations in pricing. An Ethiopian described his multi-legged, broken journey to Turkey:

I went to the bank, took all of my money out, and asked my sister to keep it. I had money from my job— about 300,000 birr [$12,000] in my bank account. I wanted to go to Sudan. I called my friend who lives in Germany, and he gave me the phone number of a smuggler. I met the real smuggler after two weeks. We discussed the travel—I told him: “I have money and everything. Whenever I can leave, I’m ready. ” The smuggler said okay. He asked for $1,200. To go to Sudan only, to which I said, “Okay, anywhere but Ethiopia. ”

Someone working for the smuggler drove us to the border with Sudan. The driver told us to get off, and he left us in a small house there. He told us to wait for a Sudanese man. When the Sudanese smuggler came, we crossed the border at night with him by foot. We walked for four or five hours. Then we took a car to Khartoum. The driver doesn’t leave us for a second. The Sudanese smuggler called the Ethiopian smuggler when we arrived. Then the Sudanese smuggler gave me a phone to call my sister so she would pay him. I think she met one of them in person, but I’m not sure who or how she paid.

In Khartoum, I had to stay in the smuggler’s house for ten days without going out. I heard an Ethiopian had been deported from Sudan to Ethiopia. I tried to collect information, and when I realized it was too dangerous to stay there, I told the smuggler I wanted to leave. I said I wanted to travel to another country, farther away. I wanted to go to Turkey and stay there. The Sudanese smuggler put me in contact with a Turkish smuggler. I didn’t speak with the Turkish smuggler, just with the Sudanese. He asked for $2,000. I stayed in the same house for four more days. And then the smuggler gave me a fake passport with a visa to Turkey.

—Ethiopian man in Greece

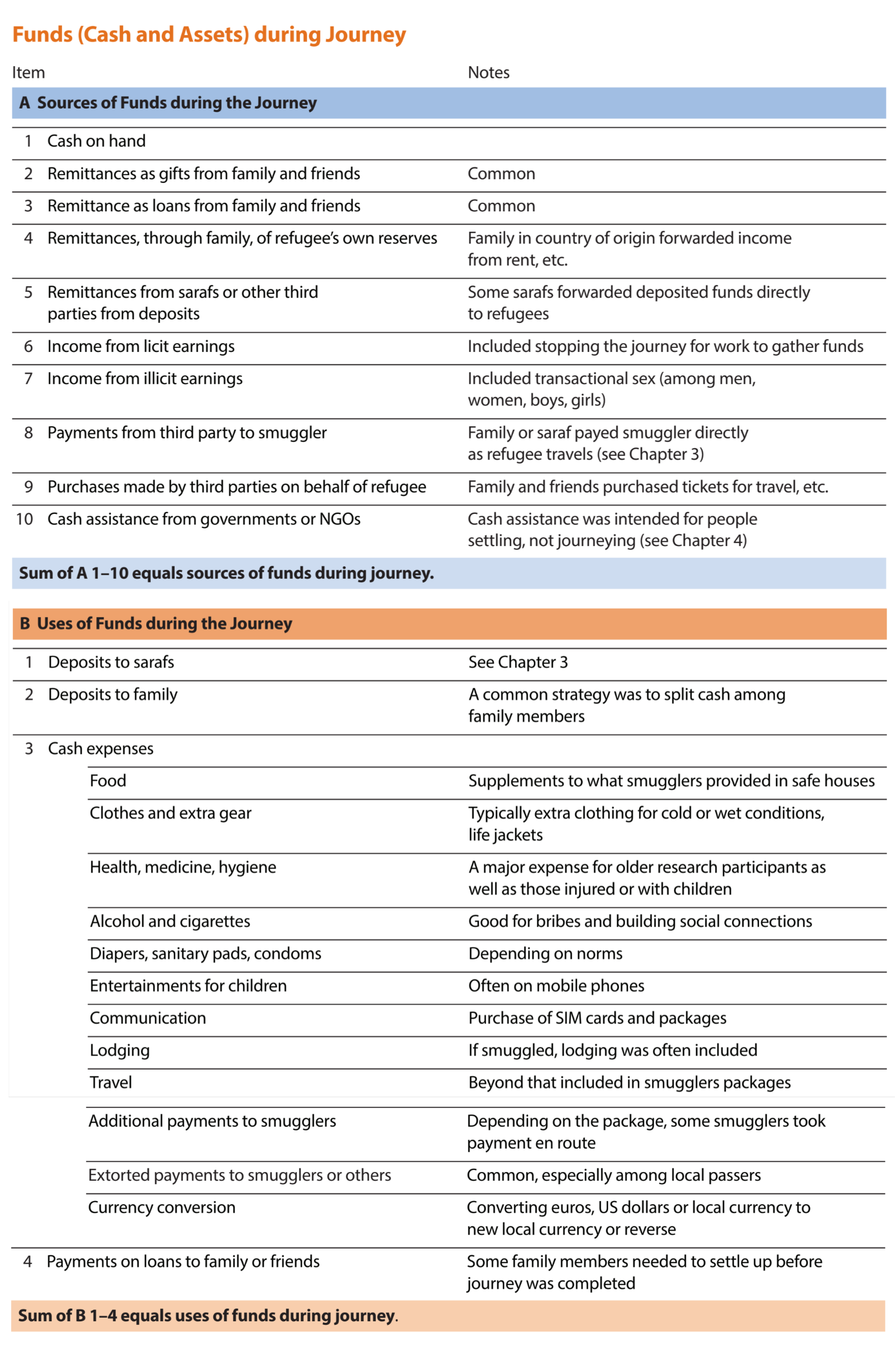

2.3 Beyond Smuggling: Other Uses of Funds on the Move

Having reviewed the ways in which the price of smuggling is a key cost of the financial journeys of refugees, we now turn to the rest of their expenses. A summary is provided in Table 4. Costs varied, depending on the individual experiences of refugees, as well as their family status. For example, refugees fleeing with young children reported spending money on diapers and baby food, as well as medical care along the way. Similarly, refugees who were injured during transit reported issues both with amassing funds (often because they could not work at the time) and with unforeseen expenses.

We note some interesting silences regarding spending and costs along transit routes. Specifically, in none of our conversations with refugees did spending on their own entertainment come up; insofar as entertainment or leisure was mentioned, it was always with reference to refugees’ children (for whom they occasionally bought new toys or clothes).

Key informants at times expressed skepticism regarding the acceptability of refugees’ use of money towards what these key informants perceived as indulgences. One key informant in Greece expressed dismay at the idea that refugees had used humanitarian cash assistance (discussed in Chapter 4) towards haircuts, and another key informant felt similarly about adult women using cash assistance to buy new clothes. A key informant who had worked with refugees throughout the Balkans echoed dissatisfaction with the idea of refugees buying themselves computers or hairdryers. These dynamics are worth examining for three reasons: First, they suggest a hierarchy of legitimacy in others’ imaginations of refugees’ needs—and that hierarchy may shape the narratives that refugees feel they can produce to describe their own spending habits on the move. Second, key informants’ attitudes regarding refugees’ “allowable expenses” reveal imaginations of dignity, vulnerability, and need and are, thus, instructive for understanding how refugees are expected to perform their plight. Third, as many of these refugees enter phases of protracted displacement and as “transit” becomes an indefinite state or a new norm for some of them, additional attention will need to be paid to their forms of leisure, entertainment, and construction of a life beyond survival.⁸

2.4 The Special Cost of Bribes

Bribes took on a major role in most journey narratives. This is not unique to the context of our study; from urban refugees in Kenya (Pavanello et al. 2010, Campbell 2006) and Mauritania (Lindstrom 2003) to journeys of Central American migration (Brigden 2016, Galemba 2017), people on the move frame bribes as a livelihood strategy or a strategy for facilitating passage and ensuring self-protection.

Among those reported to have solicited or accepted bribes from refugees are police, border guards, smugglers, and camp residents. Depending on the risk the refugee faced and the relative power of the briber, the cost of bribing varied. A Congolese woman reported having paid a $2,000 bribe twice, once to get released from prison and once when police searched her suitcase at an overland border crossing in East Africa.

After the investigation in September, the police saw I was innocent and re - leased me. When I got out, I told myself, “I can’t work here anymore. There are no other jobs. I have to leave. ” My lawyer too said I should leave, turn the page. I sold my house with the help of my lawyer for cash. It was a beautiful home. I put the money in my luggage. In Goma, I stayed in a hotel for two weeks. I knew no one there so I wasn’t hiding. I was going out to shop. After ten days my lawyer called me: “The bank is still after you. They’re saying the money you have is not the house’s money and that you didn’t sell the house. It’s the bank’s money, ” they say. “You have to leave. ” I bought a bus ticket to go to the border. I had my luggage with the cash inside with me. At the border, they checked us, and they saw I had all that cash. I had to justify why I had so much money. I said it was my money, that I sold my house, but they didn’t believe me. They arrested me and put me in jail for four days. I called my lawyer and they released me, but I had to give them $2,000.

—Congolese woman in Greece

Though this is a unique case, the necessity of bribing to secure passage, release oneself from prison, procure documents, or ensure relative safety recurred throughout the refugee narratives we encountered. As an Eritrean woman shared in Greece, “I had to pay $5,000 to go from Asmara to Khartoum. It is so dangerous to leave Eritrea that it is very expensive to corrupt the guards.” Bribes to reduce jail time when police caught refugees trying to find smugglers to lee were common, especially in Turkey:

You see the same people in jail again and again—we are all making the same journey. If you bribe the police, maybe they won’t throw you in jail, or they will let you out of jail faster. And sometimes, nothing happens. The police catch you trying to leave, but nothing bad happens.

—Afghan man in Greece, narrating his experience in Turkey

Some bribes were part of an intricate system that involved police and were bundled into the price of the journey. A refugee described his experience in Turkey:

In Istanbul we started looking for sea smugglers. Every smuggler was giving us diferent prices. I started having expertise in this. Even in the streets, some people approached us “selling paradise [a ticket to Greece] for 500 euros. ” One of our friends in France recommended an Algerian smuggler: The smuggler had “ten years of experience” and put us in contact over the phone. We went to his house. It was big. He has a Turkish residency. He works with the Turkish people, with the police. He said: “Don’t worry the Turks work with me… I make you pay only 500 euros. Don’t tell your friends. ” We got along very well. He got us passports and took care of everything for us. The smuggler told us a policeman would come to us and that we should do whatever he told us to do and not speak to anyone else. The policeman did approach us at a corner—we pretended to know each other—and he asked each of us to follow him one by one to diferent restaurants where he would take money from us—his payment. We had to give him 100 Turkish liras. Once we had all paid him, he said, “If you’re with me, the police won’t speak to you, ” and we followed him to the public bus stop.

—Algerian man in Greece

None interviewed seemed surprised about the requirement to pay bribes for various services. Many spoke of needing to “hasten the process” or “find a way.” Some planned well in advance for the eventuality of paying a bribe. A researcher’s fieldnotes reveal how a research participant in Jordan prepared in Syria for the eventuality of bribes along the way:

The family lew into Amman then traveled to Irbid by bus. All they had with them were their documents, some clothes, and a special drink from Syria (didn’t specify) that she [the refugee] would use to “bribe” guards at various points.

—Researcher’s fieldnotes from conversation with Syrian woman in Jordan

Finally, bribes were not absent from camp settings—even among refugees themselves. A key informant in Greece relayed that in one camp, after an NGO digitally loaded up cash assistance onto refugee-held debit cards each month, certain camp residents would tax each aid recipient the sum of €10, or about 10 percent of their aid, in exchange for “protection.” These camp residents would be refugees themselves with no formal power, but with perceived informal authority among other refugees, particularly in terms of guaranteeing security. Gretchen Peters (2009, p. 132) describes a similar scheme in Afghanistan, wherein “shopkeepers, like farmers, could expect to hand over about 10% of their monthly take, either in the form of cash or commodities.”

2.5 Making Money on the Move

Until this point, we have reviewed how refugees prepared financially for their journeys, and took stock of their sources and common uses of funds. We now turn to refugees’ strategies for making money while on the move. Most of our research participants were not able to finance their journeys exclusively through the assets they gathered prior to departure. Instead, they had to piece together a financial strategy while on the move, which combined laboring, borrowing, and attempting to safeguard cash from being lost or stolen and/or stretching their cash assets to last as long as possible. The strategies we encountered included

- scrambling (scrambling for cash from relatives in the form of loans or gifts),

- swapping (switching out one asset for another while on the move or in preparation, such as selling gold for cash).

- squirreling (storing or hiding money from others, such as by sewing it into clothes).

- stretching (making what little money they had last till the next grant, or transfer), and

- shunting (directing payments via third parties to smugglers).

In this section, we focus on scrambling and swapping. Other sections of this report detail squirreling, stretching, and shunting.

A. Harvesting Income from Immoveable Assets

Some research participants had relatives in their country of origin who forwarded the income earned from immovable assets at home. One such research participant reported,

We sold one house for about $100,000 to get money for our journey. We did not have to borrow; the second house is being rented for $300 a month.

—Afghan man in Greece

Certain research participants from Syria, in particular, reported that relatives at home were forwarding money from jointly held businesses still functioning in their hometowns or from liquidating property and equipment. What was not clear from our interviews was how long assets back in a refugee’s country of origin could continue generating income. Conflict and the threat of destruction or seizure, as well as continued liquidation, would surely deplete assets; this area requires further research over time. Notably, this strategy of harvesting income from immoveable assets was only available to refugees of particular social classes who had access to those assets in the first place, which does not accurately reflect the experiences and backgrounds of many of the refugees we met transiting our countries of study.

B. Selling Assets: Swapping an Asset for Cash

Many of our research participants traveled with assets to be sold along the way. The asset most cited for stowage and sale was gold:

They brought gold and money with them when they crossed the border. His family traveled irst to Beirut by car. His father drove with them to help see them through the checkpoints on the way. They passed 7-–8 checkpoints in which soldiers were heavily armed, not like the quick security checks that they had known in the past. They spent four hours driving. At the airport, they said goodbye to his father. His father gave him cash and gold to carry.

—Researcher’s fieldnotes from a conversation with a Syrian man in Jordan

Research participants discussed the sale of the gold they carried:

In Homs, she and her family stayed in a hotel for the night (with more than “one million other people” in the same room). There were no blankets, so she covered her children with her coat. They stayed in Homs for one week, and she sold her gold for cash there. Her husband’s annual bonus had paid for the first bus ride, and now they were low on funds. They attempted to travel to Jordan again, this time a different route. They went back to Damascus, then from there to Zabadani and then to Lebanon. With the gold she sold, they paid for a car for the family to Beirut (they slept in the car the first night). From Beirut, they traveled to Tripoli. Their relatives were very poor, and could not house them, so the family stayed overnight in a storeroom.

—Researcher’s fieldnotes from an interview with Syrian woman in Jordan

C. Rotating Savings Clubs

Some Syrian refugees reported a model of informal and rotating savings clubs with family members. In such clubs, each member would deposit an agreed-upon sum over a given cycle. During each week of the cycle, a designated member would receive the entire pot. This would repeat until each member had received the pot. The club allowed members to gather a more useful sum of money to fund a special purchase or to pay larger expenses such as rent.

While this type of system is common outside contexts of armed conflict or forced migration (Ardener 1995), research participants reported that it was challenging to keep these clubs together in times of displacement. Uncertain income streams and frequent movement and relocation of club members made holding the clubs together difficult:

Inside her home, her family participates in their own jama3eh [savings club]. Everyone who can contribute financially puts money in weekly, and it gets paid out to individuals on a rotating basis so they can use the lump sums to pay for personal expenses. She says jama3ehs aren’t super common outside families because there’s always the risk that someone will exit it (move) and no longer contribute/take the money with them before the circle is finished. This insecurity/people always on the move is making most refugees hesitant to use this system.

—Researcher’s fieldnotes from interview with Syrian woman in Jordan

D. Licit Wages and Livelihoods

Research participants often could not travel in a continuous, unbroken journey. Instead, they traveled in fits and starts, their available cash and income opportunities defining stops along the way. Refugees not only had to earn income to pay their living expenses, they had to save up for their onward journeys. Those onward journeys did not come cheaply, but often included the expensive services of smugglers. As a result, refugees took up a range of temporary employment as a strategy for gathering funds. While a detailed exploration of the legality, politics, and practicalities of refugee labor is beyond the scope of this report, we provide a few illustrative examples in this section.

In Iran, they stayed in Shiraz for about seven months to earn money for the next part of their journey—she stitched goods that were sold in the market. Her uncle sold their house in Kunduz, and they waited until he sent the money to them in Iran. Once they earned enough for their next journey, they found a smuggler for $800 per person to cross to Turkey.

—Researcher’s fieldnotes from interview with Afghan woman in Greece

Not all stops were planned and foreseen at the beginning of a journey. Emergencies arose that required refugees to halt their movement and gather more funds. Key informants and refugees cited medical crises as a reason to stop and earn an income. A research participant described her trials getting from Syria to Greece:

We have been in this camp for four months. It took us ive days to get from Deir ez-Zor to Turkey. We had to use a smuggler to get out of Syria because we traveled through areas controlled by Daesh and “the system.” I traveled with my sister, her husband, and her two children, then me and my daughter, and our uncles. There were 10 children in the whole group, and 20 of us altogether. My sister and her husband and children stayed in Turkey because their daughter was sick. I waited for four months there because my daughter was sick too, but decided to keep moving with her after she got better. She is two years old. During the four months, I worked in a factory for a Turkish boss.

—Syrian woman in Greece

E. Illicit Wages and Livelihoods

Women reported that they often did not have the social or cultural permission to work in agriculture, domestic, or construction jobs. Refugees of all genders and ethnicities also reported lacking either the working permits or the skills to obtain regular wages.

Some of the men and women who fell outside the quotas and constraints of the formal workforce often fell through the cracks of assistance systems as well.⁹ They had few alternatives to earn money. Some turned to transactional sex in exchange for cash, which is discussed in greater length in Chapter 5.

F. Blended Income: Formal and Informal

Rarely did research participants who worked only work in the formal sectors. Their opportunities changed as they were able to get work permits, place themselves in a location with good job prospects, or upgrade their skills through training. The following example, told in the participant’s own words, illustrates a remarkable journey from Syria to Turkey via a northern country. We provide his long narrative below (edited for security and brevity), as it illustrates a circuitous journey, the uncertainty and patchiness of his income, and his constant financial shuffle.

I left Syria in late 2012 when my job ended after the start of the uprising. I was arrested twice for participating in the protests. The organization laid some of us off, as my job required me to travel between cities and they could not guarantee our security. I faced trouble at checkpoints, so decided to travel. Turkey wasn’t my destination. I decided to try to go to a northern country. I wanted to go to a university there. I studied the language.

I carried the money on me. I waited for 16 hours in Beirut and didn’t leave the airport because I was worried about my stuff. I flew from Beirut to Istanbul airport, then on to the country. I kept my money on me the whole time.

I brought winter clothes, but didn’t end up needing those because the best way to fight cold is layers. I brought my ID, certificates, passport, military service book. I worked in a bakery when I ran out of money. He paid us daily wages. I got bored, and had to leave the dorm. So I used my remaining money to buy a tent and a hiking backpack.

After a month in the country, they asked me to leave because I was active in a protest movement. They gave me two weeks’ notice to leave the country. I saved up money and bought a ticket to Istanbul.

I was paid cash for day labor and spent that money on a daily basis. I spent as earned to get some food. I had been able to save money working as the bouncer. I saved $500. I used that to buy the ticket to Istanbul, some $180. I met an American there, part of a missionary group. He helped me buy the ticket online using his credit card. I paid him in cash. We are still friends on Facebook. He liked my hiking experience; we were friends. Working on the farms in the towns wasn’t that easy. There were times when I would not find a job for a few weeks. I would use the job to buy bread and mayonnaise. There was one incident when I could not find work for four weeks. I hunted for food with a Swiss army knife.

All my money came and went on the trip. I started the trip broke and earned enough money for each day. I remember when I left Syria, I had $1,800 on me. This was a lot of money for me. It was my savings from the work I was doing. The possibility of losing it was too much. If I’d known how to wire it to a safe account and pick it up there, I would have, but didn’t know how to do that. Even when I was in one place, it was hard for me as a foreigner to open a bank account with a residency permit. By the time I had been there long enough, the money was gone. When I flew to Turkey, the authorities stamped my passport and let me in.

I slept on a bench in front of the Blue Mosque for three weeks, looking for an apartment I could afford. I found a room for 150 Turkish lira per month, with only a mattress and a chair. On the bench, I was completely ignorant. I blocked out the existence of other Syrians. I didn’t want to introduce myself to anyone else because I didn’t trust them. I kept my cash with me on the bench, in my socks.

I enjoyed the apartment with this old guy. He confused English and Russian, combining them to talk to me. I started looking for a job because my $300 was running out. I ate one meal a day; sometimes I forgot because I got used to low food consumption. I started posting on Craigslist to teach Arabic, English, and other languages. I asked if market shops were hiring. I found Craigslist through looking for vacancies on Google. I saw that you could post there that you were looking for a job.

—Syrian man in Greece

G. Mixed and Changing Portfolios

Families had multiple sources of income, and their income portfolios shifted over the trajectory of their periods of transit. The financial shuffle was constant, piecemeal, and ever-changing.

This research participant’s scramble began before he started his journey and continued in Lebanon, Egypt, and Turkey:

My friend had rented an apartment. It was awful, but it was ready. To get there, we—my wife, toddlers, and me—went by car to Lebanon, then lew to Egypt. My cousin bought the tickets online for me. He also sent 500 to me in Egypt through Western Union. My friend in Saudi did the same. My sister gave me cash. Another friend gave me $250 in cash. A friend in a difficult situation offered to give me $200 in cash. His brother carried the money to my brother who gave it to me before I left. We had about $3,000 on us. My wife hid the money in her clothes. I had some daily money in my pocket.

I applied for jobs, didn’t get any, so I used the time to learn the transportation system. A couple of months later, a friend with a company was settled, so we resumed the work that I had been doing in Syria. I started the online job again. Then a professor who’d been my teacher at university offered me an opportunity. Later, my cousin who was also in Egypt told me about a customer support company in Egypt. So I worked for that company, fulltime. I had three jobs. After three months I was so exhausted, I resigned from the technical support job.

—Syrian man in Turkey

Not only did he knit together an income from far-flung sources, he knit together multiple ways of getting paid: