Written by: The Journeys Project

Table of Contents

Executive Summary¹

Managing finances is challenging for most people, but it is truly daunting for

migrants and refugees. They face numerous hurdles that range from obtaining the right documents to securing permission to work—obstacles that limit both their income and their opportunities to make longer-term investments.

Between 2019 and 2021, a research collaborative between Catholic University Eichstaett-Ingolstadt, Tufts University, and the International Rescue Committee conducted research in Jordan, Kenya, Mexico, and Uganda on refugees and migrants, focusing on those who had been in their host countries between three and eight years. We chose this time period to capture their early arrival experiences and longer-term coping and integration strategies. In total, we conducted 428 interviews,² organized field observations, and utilized focus groups in two locations.

The aim of our research was to understand how refugees and migrants financially integrated into their host surroundings and how financial services played a role in that integration. If we were to elevate two key insights that supersede the findings in this summary, they would be:

- Financial services do not lead to fulsome livelihoods or to financial health, but fulsome livelihoods and improved financial health lead to the need for more financial services; and

- We did not observe financial or economic integration in most instances. At best, adaptation occurred as respondents settled into their new surroundings.

Our sample and methods are more fully explained in the Methods and Sample section of the Appendix. But we must point out that there were limitations to the research. The COVID-19 pandemic affected two research sites—Jordan and Kenya—where research was still underway. While all studies borrowed from a Grounded Theory approach, a method that tasks researchers with refraining from testing specific hypotheses in order to see what insights emerge during the course of the research, the Kenya and Jordan studies differed from the Mexico and Uganda studies. In Kenya and Jordan, our teams interviewed the same respondents (minus a few dropouts) three separate times, with each set of interviews picking up on different aspects of life as a refugee. In Mexico and Uganda, respondents were interviewed only once. The different methods and different contexts challenged our ability to draw comparisons. This report is an attempt to draw out similarities where possible and highlight discrepancies when findings diverged.³

Our high-level findings⁴ follow:

Finding 1: For financial inclusion policies to make a positive impact, they must build on host government policies that give refugees rights, opportunities, and provide appropriate documentation. Refugees’ financial success depends on their ability to exercise fundamental economic rights that are often denied to them. Without the ability to move about freely and safely, effectively procure permission to work, or open a small business, financial services (such as credit, savings, and insurance) can do little

to build the financial well-being of refugees.

Finding 2: The need for and the uses of financial services coevolve with progressions in the diversification of refugee livelihoods. The financial services that refugees need upon arrival are designed to help them survive and are distinct from services that help build robust livelihoods later on. Demand for services shifts depending on both the stage of displacement and the opportunities available. If refugees are allowed to participate in

local and regional economies, their livelihoods progress naturally. Only after

they find their bearings and learn new skills do they develop uses for financial services. As a companion finding, elaborated on in Finding 3, we learned that refugees and migrants value mainstream financial services popular with host populations versus those that are designed specifically for them.

Finding 3: Financial service providers (remittance, mobile money, banking, and MFI services) need not create new services for refugees. Instead, they should adapt existing mainstream solutions that are popular with the host population by making necessary adjustments (such as language or documentation needs). Different organizations have been nudging refugees into services, channels, or platforms that are not yet mature or have not yet found solid footing within host populations. For example, services that rely on networks, such as remittances via mobile wallets, may only be in an

experimental stage with a host population, as is the case in Jordan. As such, one cannot expect widespread adoption by refugees. This finding is important for two reasons. First, refugees and migrants do not constitute a market; they are not a homogeneous group defined by similar traits, customs, and preferences. They speak different languages, have different priorities, and engage in different financial practices. Their livelihoods

and financial needs evolve at different paces and in different ways. Because of this population’s diversity, a supplier would need to develop a business case for each market subset, an expensive proposition. Second, refugees and migrants are not a segregated group either in camps or in urban areas. They interact with members of the host population and can observe the financial products their hosts use.

Finding 4: The uncertainty of long-term prospects discourages refugee investment in skills and assets, limits self-reliance, and produces a permanent dependence on charity. Instead, they invest energy in hoping for resettlement, a highly unlikely prospect for most. In two of our research countries, Kenya and Jordan, an overwhelming majority of respondents believed that resettling to a third country was the only way to improve their circumstances. Not being able to obtain a work permit, become a legal resident, legally own business assets, or even buy basic necessities like

a SIM card, deterred investment in new skills, property ownership, or business assets.

In our other two country sites, Uganda and Mexico, where rights were more easily accessed, migrants and refugees could obtain work more steadily and tended to trade up their assets, diversify their income streams, steady their cash flow, grow their social and economic networks, and invest in education for themselves and their children.

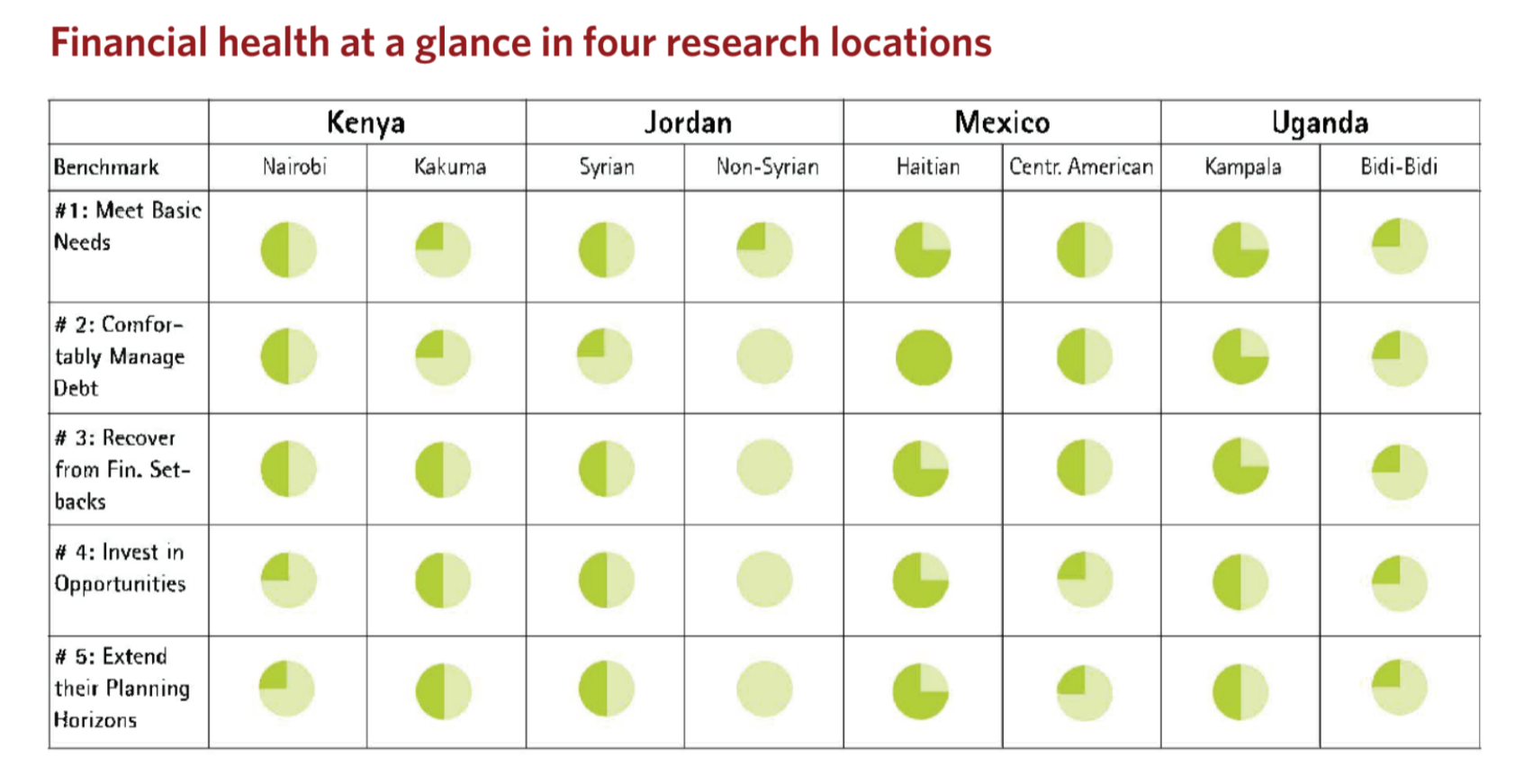

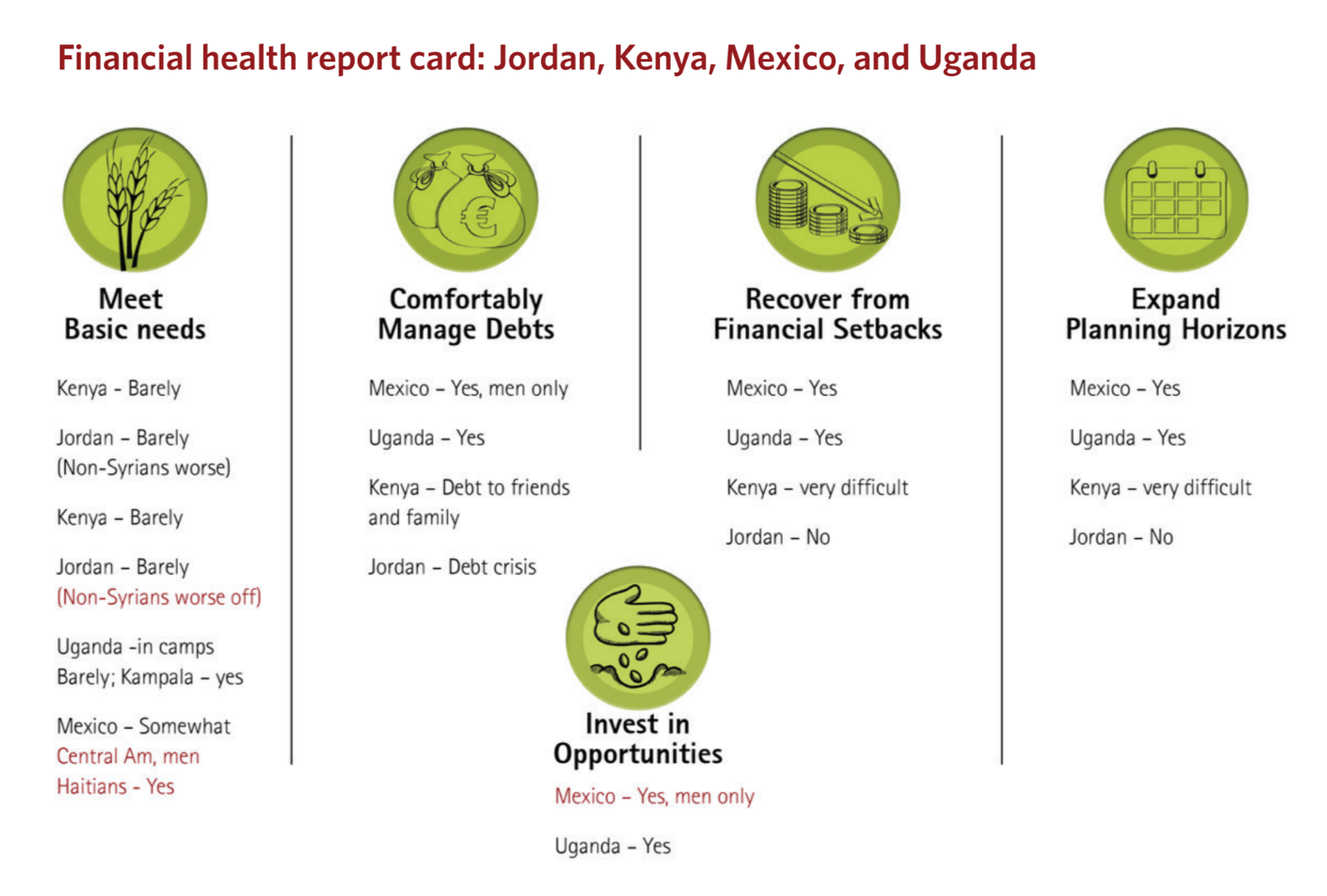

Finding 5: Our “financial health” framework modified for refugees is useful for analyzing the role of financial services in people’s financial health. We found that financial services are only one contributing factor to financial health. Certain financial services can be utterly irrelevant if more important conditions are not in place, such as the ability to obtain identity documents, to work, and to move freely.

Consequently, we adapted the Council for Financial Inclusion’s Financial Health Framework⁵ for use in displacement contexts. In our framework, refugees or migrants are “financially healthy” when they can:

- Meet basic needs. This is achieved when refugees or migrants can access the resources they need, such as food, shelter, clothing, medicine, or other essential products and services. This indicator matters both at the arrival phase and all subsequent phases.

- Comfortably manage debt. Refugees and migrants frequently arrive indebted to smugglers and those who financed their journeys (friends, family, others). Debt can pile up as they begin to settle. Too much debt can render individuals and households vulnerable to ostracization, extortion, and poor mental health.

- Recover from financial setbacks. Loss of a job, a medical emergency, or destruction of an asset (such as a house, a bicycle, or a sewing machine) can produce financial hardship. Being able to borrow from social networks, access humanitarian aid, or dip into savings enables recovery from these unforeseen stumbling blocks.

- Invest in opportunities. Many refugees arrive stripped of their physical assets and cash savings. In the right conditions and with the right mindset, refugees and migrants may find over time that they have the savings they need to invest in education, training, or better housing.

- Ability to expand planning horizons. Over time, new arrivals move from daily hand-to-mouth struggles to a place where they can increase their economic activities. They find themselves able to imagine a financial future beyond the present day.

Policy Recommendations

Three years since the adoption by the international community of the Global Compact on Refugees (GCR)—a multi-sector program of action to support countries hosting large numbers of refugees and build refugee self-reliance and financial inclusion—lack of political will and leadership is limiting progress.⁶

For a vast majority of our respondents, financial health remains elusive. Host and donor governments committed to the GCR, as well as private sector and humanitarian practitioners, should implement the following recommendations to live up to their commitments and enhance refugees’ financial health:

1. Host Governments

- Create a welcoming economy by removing barriers blocking refugees' access to their rights at a foundational level, including eliminating barriers and restrictions to legal work, and limitations on freedom of movement.

- Include refugees in national policies and services, including social protection, education, health, and national financial inclusion policies.

- Increase bureaucratic efficiency and transparency and ease access to refugee documentation and permits required to secure a decent livelihood, without discrimination on the basis of nationality.

- Provide easily accessible and regularly updated information through official channels about immigration procedures and pursuing employment or business activities, finding housing, language classes, and childcare.

- Challenge current norms held by government service providers, employers, and financial service suppliers that stigmatize refugees and block them from using mainstream services.

- Provide a clear path towards long-term solutions to help refugees plan for the future. Examples include pathways to residency, new work opportunities, and skills-building.

2. Host Governments and Financial Regulators

- Ensure refugees from all nationalities can access mainstream financial services, by providing a clear regulatory framework and guidance for financial service providers that permit the use of alternative forms of government-issued refugee identification documents through tiered or simplified Know Your Customer and customer due diligence requirements based on a proportionate risk-based approach that balances proof of identity requirements with risks associated with terrorism and money laundering.

- Ensure access to mobile phones and SIM cards for refugees.

3. Donors and Multilaterals

- Advocate for full economic and financial inclusion of refugees in policy dialogue with host countries.

- UNHCR should reduce uncertainty for refugees by increasing long-term livelihood options while providing clear and regular communication regarding resettlement from the country, as well as regular updates on individual applications, ideally through digital tracking of their application status.

- Increase flexible funding for community-based organizations (CBOs), refugee-led organizations, and religious organizations that often do the heavy lifting when it comes to new arrivals and long-term arrivals unable to survive without charity.

4. Financial Service Providers and Mobile Network Operators

- Authorize the use of alternative forms of government-issued refugee ID documents for accessing services where government policies allow and implement the policy consistently across branches.

- Collaborate with humanitarian partners to make mainstream financialservices relevant to refugees and tailored to the needs of refugee women. This includes translating products and marketing materials to refugee languages.

- Improve customer service, address complaints regarding handling procedures, and quickly redress grievances.

- Provide training to refugees, including women, about available services and how they can access them.

5. Humanitarian Practitioners

- Work with financial service providers to improve access to formal and informal services, including through sharing information and helping refugees negotiate barriers to access and sensitizing banks to particular issues and needs of the refugee population.

- Combine financial services with livelihood support programs, including skills-building, vocational training, and financial literacy, including guidance and information to navigate documentation requirements, cross-cultural exchanges with the host community, and expanding social networks, while addressing specific barriers women face and via support for refugee-led and community-based organizations.

Finally, one overarching recommendation for practitioners, policymakers, financial institutions, and researchers is to adopt the Financial Health Framework to evaluate the impact of financial interventions.

- Evaluate success of new financial services using the adapted Financial Health Framework.

- Research and set benchmarks for the five refugee financial health indicators, to define, for example: what is a desirable lump-sum? Or, what is “comfortably” manageable debt? Specific benchmarks will help practitioners and researchers measure and respond to financial health outcomes in different displacement contexts.

Livelihoods

While the research team focused on the aim of the study—that is, how refugees and migrants integrate financially in their new surroundings—we realized early in the study that our respondents wanted to report first about their livelihoods. We have structured the report to first discuss the ways in which our sample earned an income and then how those earning streams were aided by financial services.

First Jobs

Most jobs held by respondents were found outside of the regulatory structures that characterize formal, salaried employment. Working both legally and illegally, migrants and refugees in all sites were primarily found operating in unregulated settings, far from the protection of job contracts or legal recourse.

There is no clear pattern of how refugees and migrants secure their first jobs. In Kenya, Mexico, and Uganda, refugees’ first jobs were typically menial labor positions given to them by churches, local NGOs, and locally based co-nationals (migrants and refugees hailing from the same countries). Referrals from co-nationals were also crucial in finding work. In all research sites, local residents would also offer low-paying work that ranged from washing clothes and cleaning homes in the city or, in the case of the Bidi Bidi settlement in Uganda, working the land.

First jobs in Kenya were hard to come by and usually included informal labor or home-based businesses, both of which were fragile livelihoods that depended on the mercy of local authorities. In Jordan, many Syrians made their way to Amman via the camps. They had to find a Jordanian sponsor in order to leave the camp, requiring many to frantically search for outside contacts.

Urban Livelihoods

In urban research sites, it was common to see several kinds of incomes in a household, as is common among low-income people in general in these settings. However, even if our respondents had several jobs, most could barely cover their day-to-day expenses or save money. It took several years to get work that matched their skills, even with the support of their networks. While a few found financial success, most struggled to make ends meet, doing their best to avoid exploitative work.

In Kenya, many refugees engaged in high-frequency hawking of prepared foods and trading colorful, printed cloth. Those with an education were sometimes able to procure better-paying jobs, but usually only temporarily and informally, as they were nearly always denied work permits when they applied. Unable to work, many were unable to put their skills to use in building a livelihood. For example, a male refugee had previously served as a medical doctor, but during our interviews, he revealed he was reduced to helping his wife prepare food she would then sell in the street. Others could hide for a while in professional jobs masquerading as Kenyans, but they could not enjoy any form of security. They knew it was a matter of time before they were discovered and forced to quit. Respondents were always on the lookout for local authorities waiting to either fine or shutter them.

In the urban areas of Jordan, most respondents depended on income from informal work, which was paid on a daily or weekly basis and was highly seasonal. They worked in the construction or agricultural sectors or as porters—on and offloading heavy goods in the local markets. Syrians could obtain work permits more easily than Yemenis, Sudanese, Somalis, and Iraqis, who were not allowed to work at all.⁷ Consequently, many non-Syrians worked furtively, assuming low-paying construction jobs or operating businesses from their homes, out of view of the authorities. While home-based businesses were technically legal for Syrians, they were not legal for non-Syrians, and yet were one of the few strategies that non-Syrians could use to survive. To avoid detection, women took up daily-wage work such as cleaning houses or providing beauty services on-demand at clients’ homes.

Our Central American and Haitian respondents in Tijuana engaged in both wage labor and self-employment, providing a range of services from hair braiding to construction work. Wage labor usually included low-skilled formal and informal jobs in factories, construction companies, restaurants and hotels, and domestic work.

Settlement and Camp Livelihoods

In Bidi Bidi, Uganda, a large settlement near the border of South Sudan, respondents could receive a plot of land on which to grow animal fodder and food. They were allowed to run businesses and were encouraged to trade with local Ugandans, but despite these government affordances, businesses in Bidi Bidi were modest. Many refugees brought cattle and other physical assets like sewing machines or brewing equipment from South Sudan, which they sold to raise capital for their businesses or make ends meet. For example, a South Sudanese respondent brought a solar panel with him to Bidi Bidi. He sold the panel and used the funds to purchase inventory for a liquor-brewing business. Most small businesses are related to the needs of other settlement residents, such as clothes-making, liquor-brewing, and firewood provision.

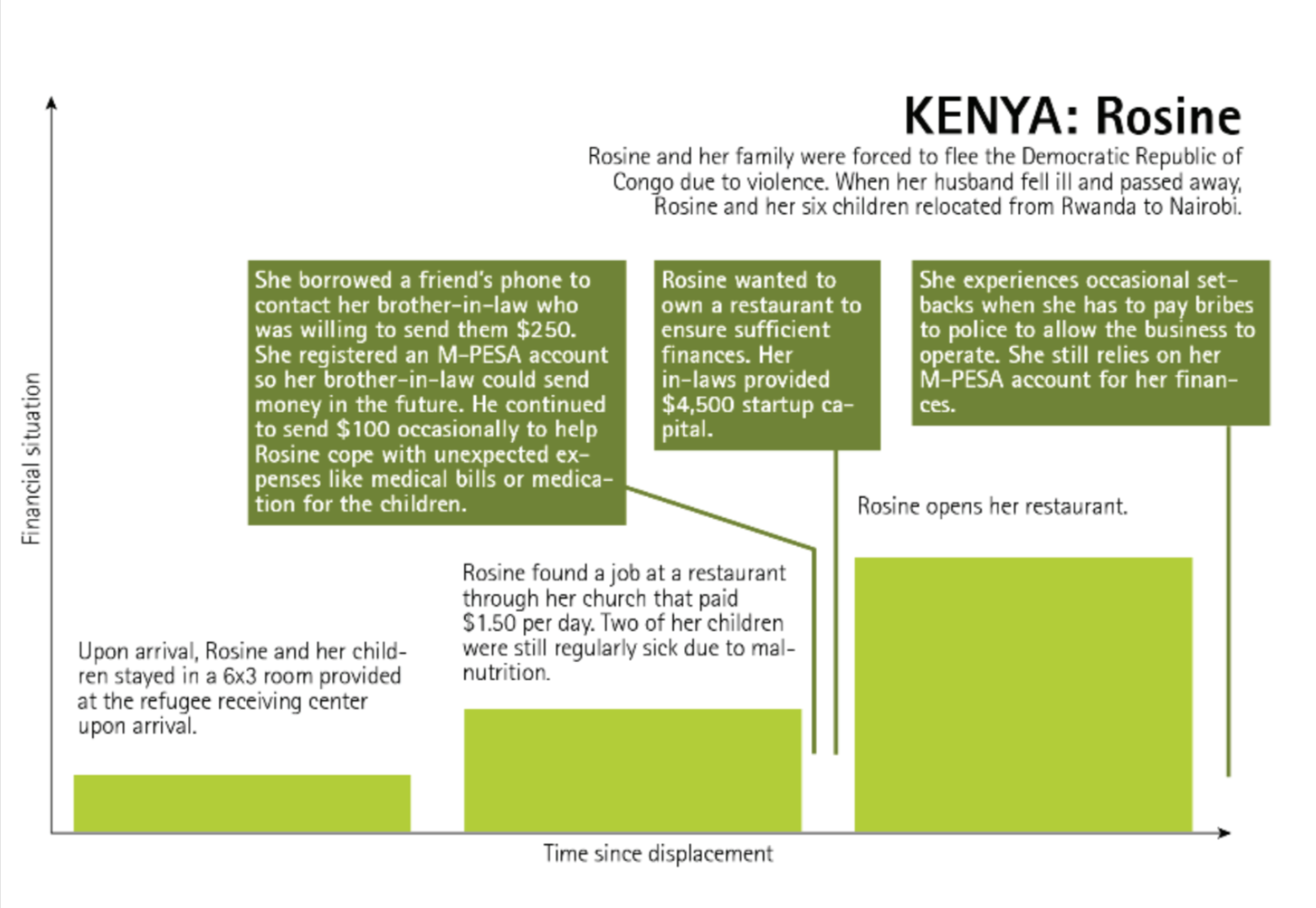

We can see another story of a refugee-owned small business in a refugee camp in Kenya below:

Sally is South Sudanese by nationality, even though she has never left the Kakuma camp. Her parents fled South Sudan for Kenya in 1992. They struggled to earn enough money to send their children to a school just outside the camp borders, where her father felt that the teachers were better trained. Her father had to quit his low-paying job building refugee houses with the National Council of Churches of Kenya (NCCK) to pay for tuition. He started a nyama choma (roasted meat) and changaa (homemade alcohol) business.

It was not the life Sally chose, but she has tried to make the most of it. Her job as a teacher brought in KES 5200 per month (which was about $52, lower than the consumption poverty line in the country), and she usually saved part of that every month in a bank account. She saved until she had enough money to buy some brewing equipment of her own and start a wholesale changaa business. She also rented out her equipment for extra cash.

In total, she made about three to four times as much money from her changaa business as from her teaching job. Her business income was a helpful cushion when she lost her teaching job due to COVID-19 budget cuts. Between her income and remittances from her sister and other extended family members, Sally’s family has achieved a level of comfort and resilience. But they would gladly walk away from all of it if they had a chance to leave the camp for good, a chance to build their lives on more solid, permanent foundations.

Volunteer Work (for Pay)

Humanitarian organizations in Kenya, Jordan, and Uganda hire refugees to assist in their refugee work. The practice makes sense—refugee workers know the plight of their people and speak their language. If they can speak both their native languages and those of their host country (or English), this qualifies them to be eligible for volunteer work. In these situations, NGOs must offer pay below a government threshold. This is ostensibly so they can comply with local laws that bar them from employing refugees without work permits, though in some places, like Kenya, it is also part of a UNHCR cap on affiliates’ wages, justified by wage “harmonization” policies.

In Jordan, respondents worked as volunteers in exchange for a transportation allowance to make home visits to refugees, organize community initiatives, conduct trainings, and provide administrative support. The allowance was modest in Jordan ($210—350 per month), but it provided a dignified and regular income. This kind of work was especially suitable for women and non-Syrian refugees who otherwise had limited opportunities. In the camps in Kenya, these “volunteer” wages typically ranged between $40-60 per month, and were often below the poverty line, raising questions about UNHCR and affiliates’ commitments to the decent work agenda.

Livelihood Progressions and Reversals

Scenario A: Urban Progressions in a Welcoming Economy

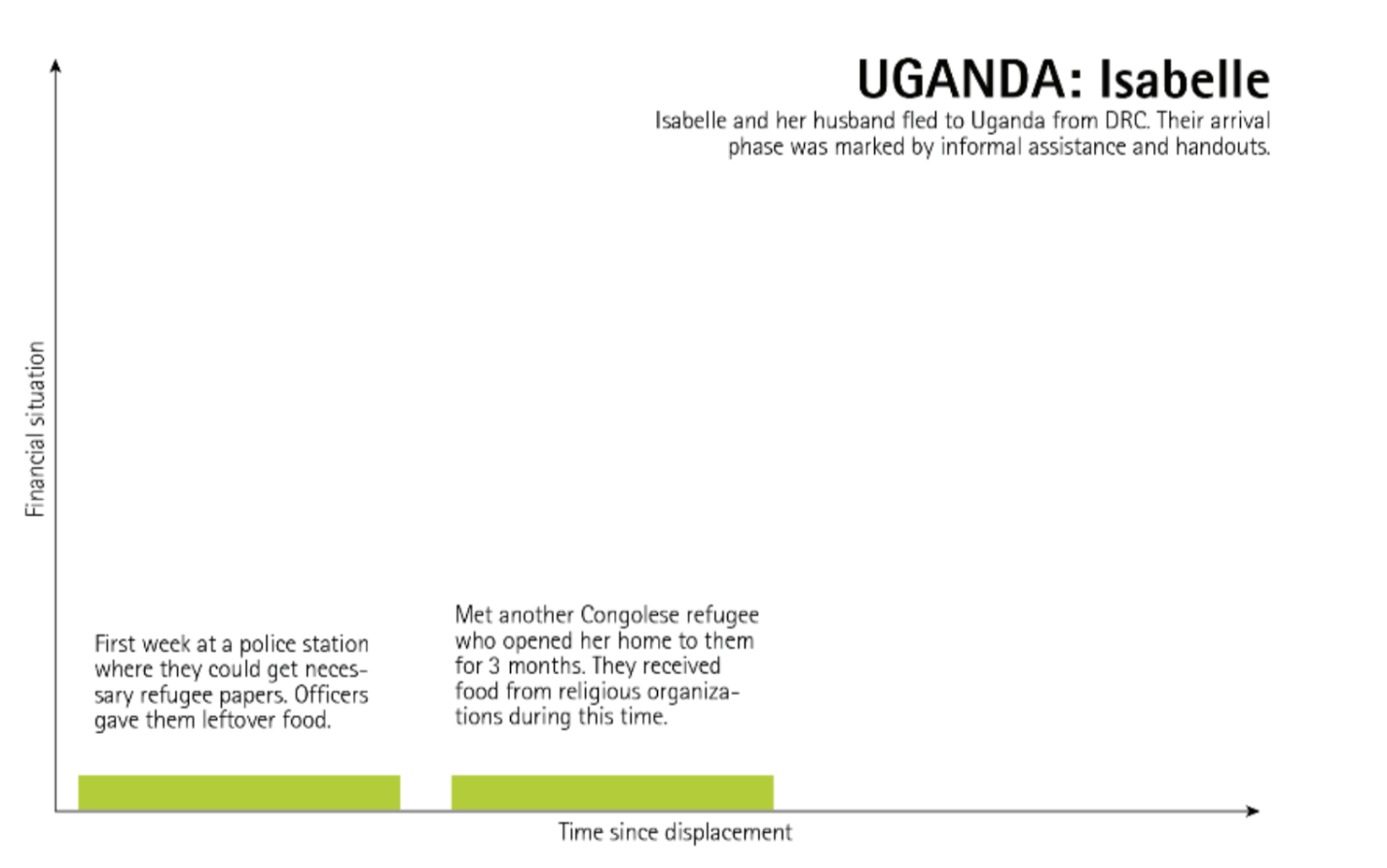

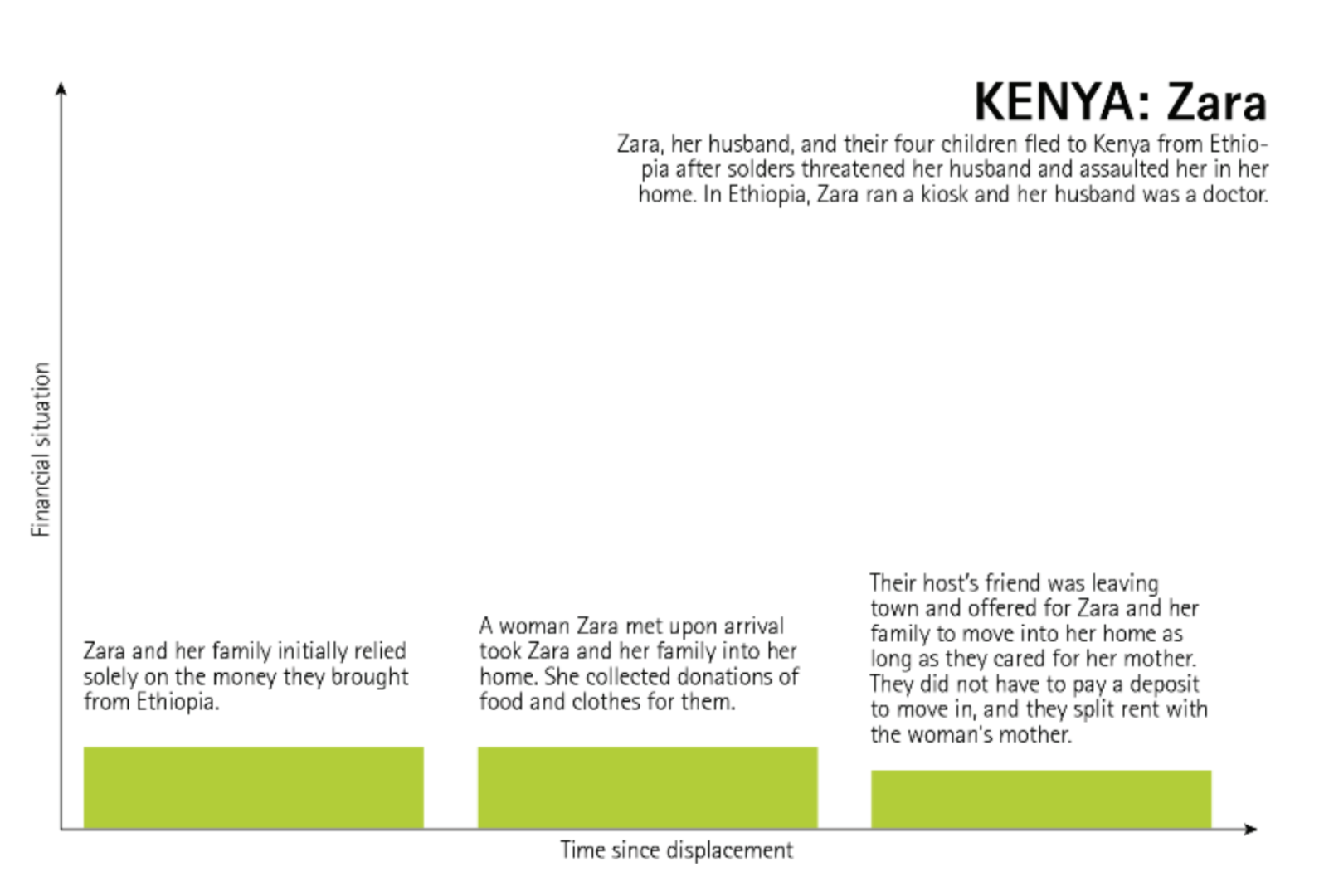

As we interviewed respondents, we saw patterns emerge. In welcoming economies— those with policies that allowed refugees and migrants to obtain documentation, work, and live and move outside of camps—such as Mexico and Uganda (what we call “Scenario A” economies), migrants might arrive penniless. During their first days and weeks after arrival (the “Arrival Phase”), they depended on the kindness of strangers, friends and family, houses of worship, and local charities to survive. Now and then, some might receive remittances from families abroad.

After some time (a few months at most), respondents would find their bearings, locate a place to live, and begin earning an income. These income streams, except for a few exceptions in Mexico, were typically meager. Respondents might wash dishes, clean homes, or sweep the steps of the local church or mosque, all for less than $1 a day.

We termed this phase the “Survivelihood Phase”; they were earning just enough money to survive.

Then, after some months, respondents would begin to progress. If they were bussing tables at a restaurant, they might get promoted to wait staff and earn more. If they were sweeping the floor of a hair salon, they might be asked to braid hair for higher pay. They could open a small business, usually from home or on the street, and again improve their incomes. We termed this phase the “Ratcheting Phase,” where livelihoods would become more robust, both in income and diversity. Many were doing well enough to abandon any thoughts of moving back home or to a third country. Instead, they would stay, get their children an education, and expand their businesses.

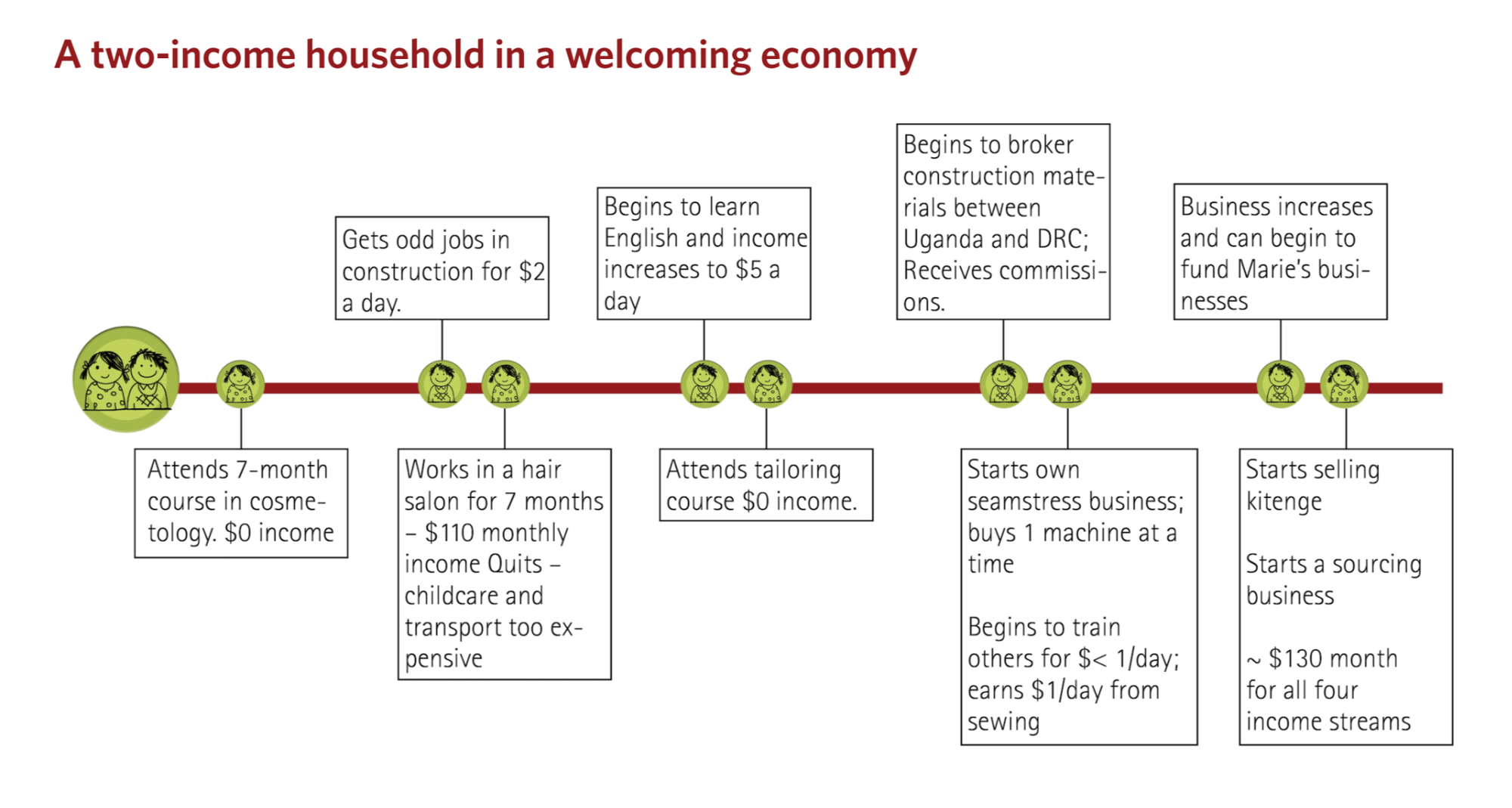

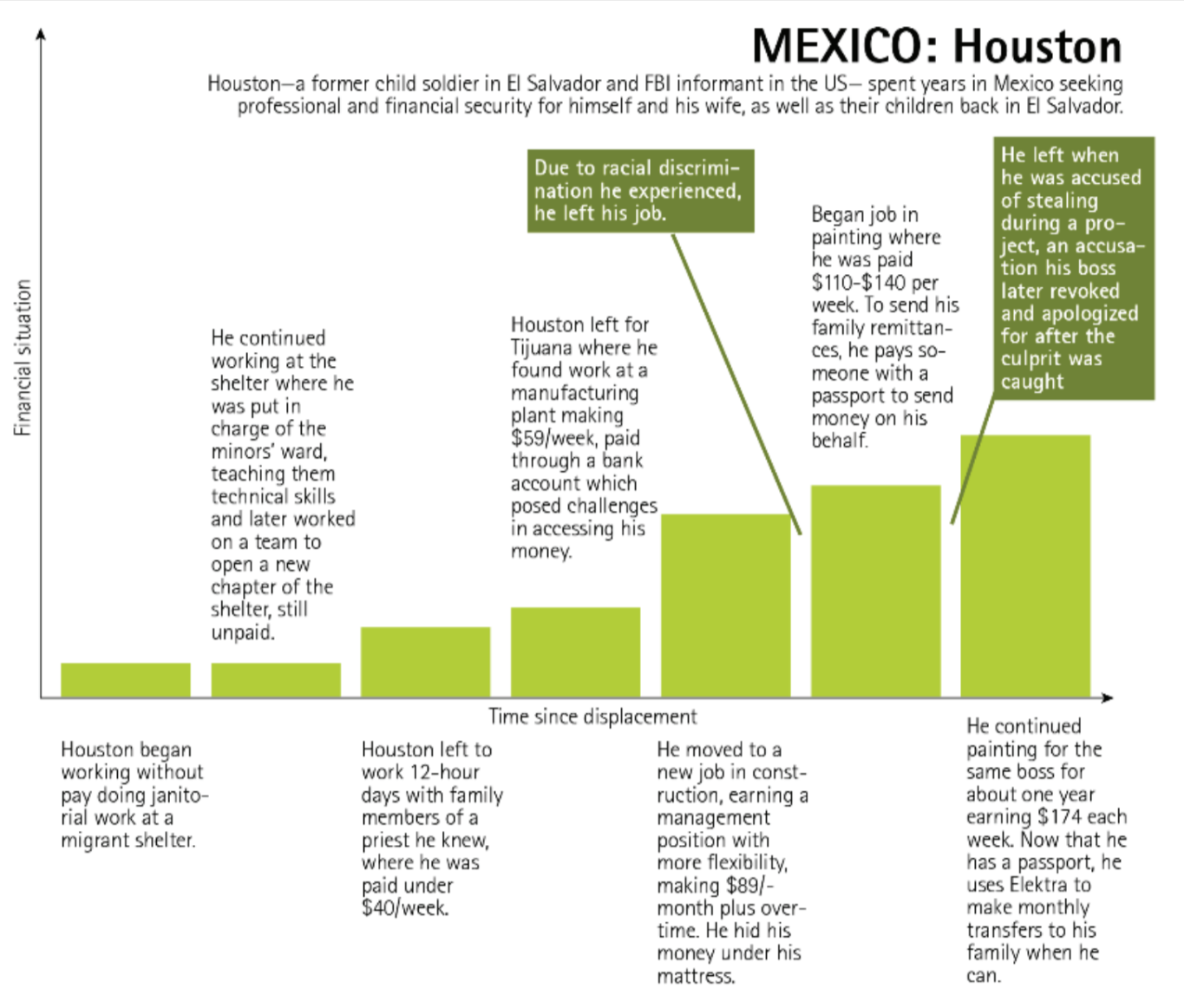

In 2012 Emmanuel and Marie, a Congolese couple, arrived in Kampala with two children, a baby, and zero funds. During their first week in the city, they relied on the Old Kampala Police Station for food. Emmanuel worked low-paid construction jobs at first, earning between $2.70-5.40 a day. He learned English, allowing him to move out of wage labor and into brokering construction materials across the border to the DRC and Rwanda.

Marie took a cosmetology course offered by Jesuit Relief Services. The course lasted seven months, convening daily from 9:30 am – 4 pm. Marie brought her baby to class. After earning a certificate, she “walked from salon to salon” until she found an unpaid internship at Treasure Salon. After three months, the internship turned into a job that paid about $110 per month, covering the cost of childcare (about $16 per month). She stuck with the job for seven months and then quit. Between the expense of childcare and the chemicals she was inhaling daily, she figured that finding new work was a better option. But during her stint at Treasure Salon, Marie was able to put some money aside. She then attended courses at another NGO, Young African Refugees for Integral Development (YARID), to learn to tailor and found a job as a seamstress in a local business. She stayed for three months and then returned to YARID as a trainer. She parlayed that work into starting her own sewing business and now has a shop that offers tailoring services and sells kitenges (colorful fabrics for multiple uses) and children’s clothes. Marie went on to start another business where she shopped online for clients—a concierge service of sorts.

With the income from Marie’s businesses and Emmanuel’s brokerage, the couple could afford to rent their apartment (about $30 per month), Marie’s shop (about $ 40 per month), and pay $35 per term for her eldest child’s tuition, which increased to $55 per term. Her second child would soon enter kindergarten with fees of $35 per term.

We can deduce the reasons Emmanuel and Marie were able to grow their activities. First, Uganda allows refugees to live outside camps, work, and start businesses, but equally important is that their household had two wage earners and two parents to watch over the children. Emmanuel’s ability to learn English was also helpful, as were the classes that Marie attended. The couple could weave together assorted income flows, allocating them between household needs and investments in their various income streams, driving all activities forward. Below, we can see how livelihoods like Emmanuel and Marie’s can develop in welcoming economies:

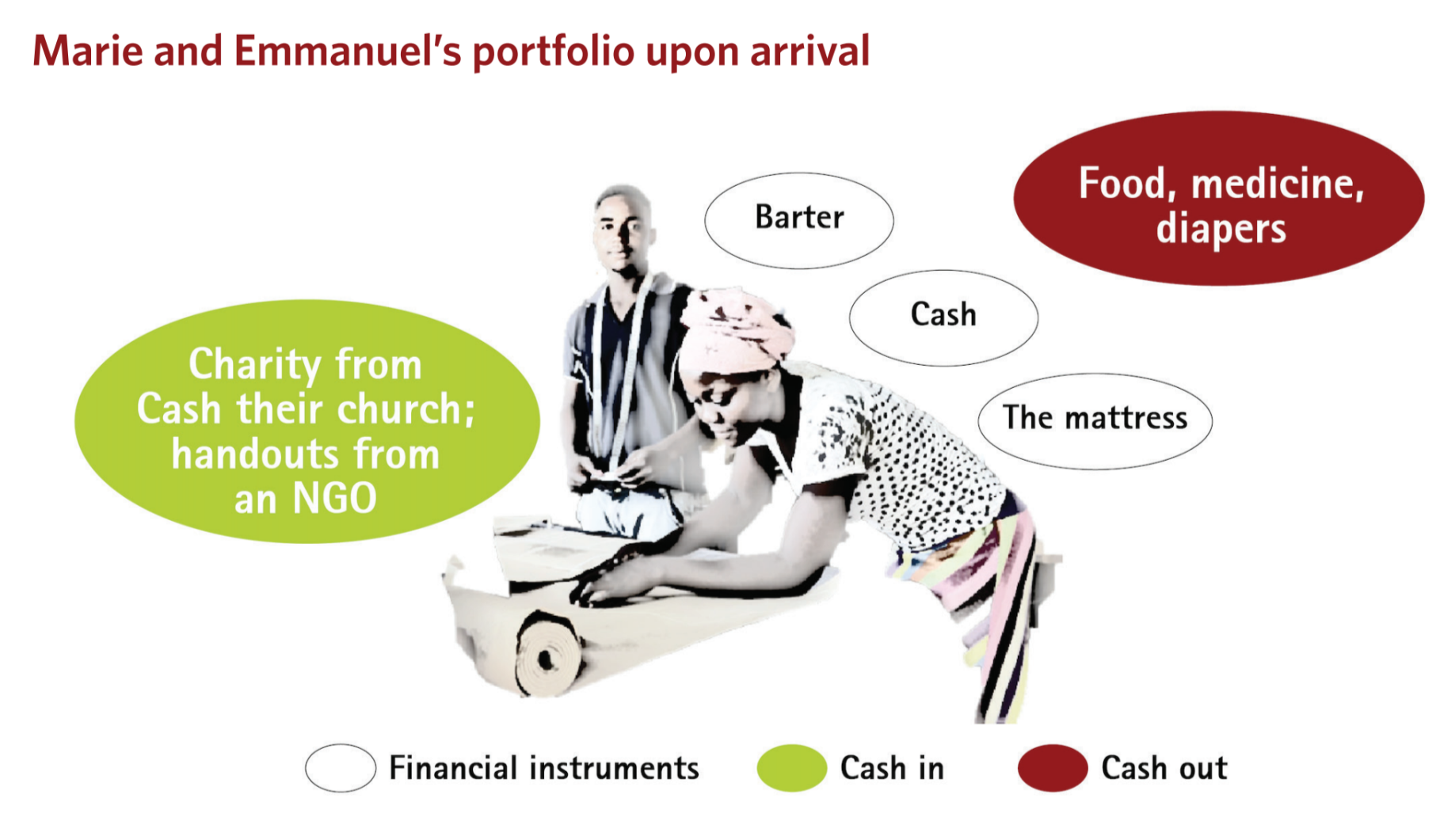

As a couple, they were able to weave together different strands of income to help support each other and grow the earnings of the household.

Initially, their sources of income and their expenses were simple. So too was their use of financial instruments. Their initial income was so meager that they had little use for anything more than the crudest financial services.

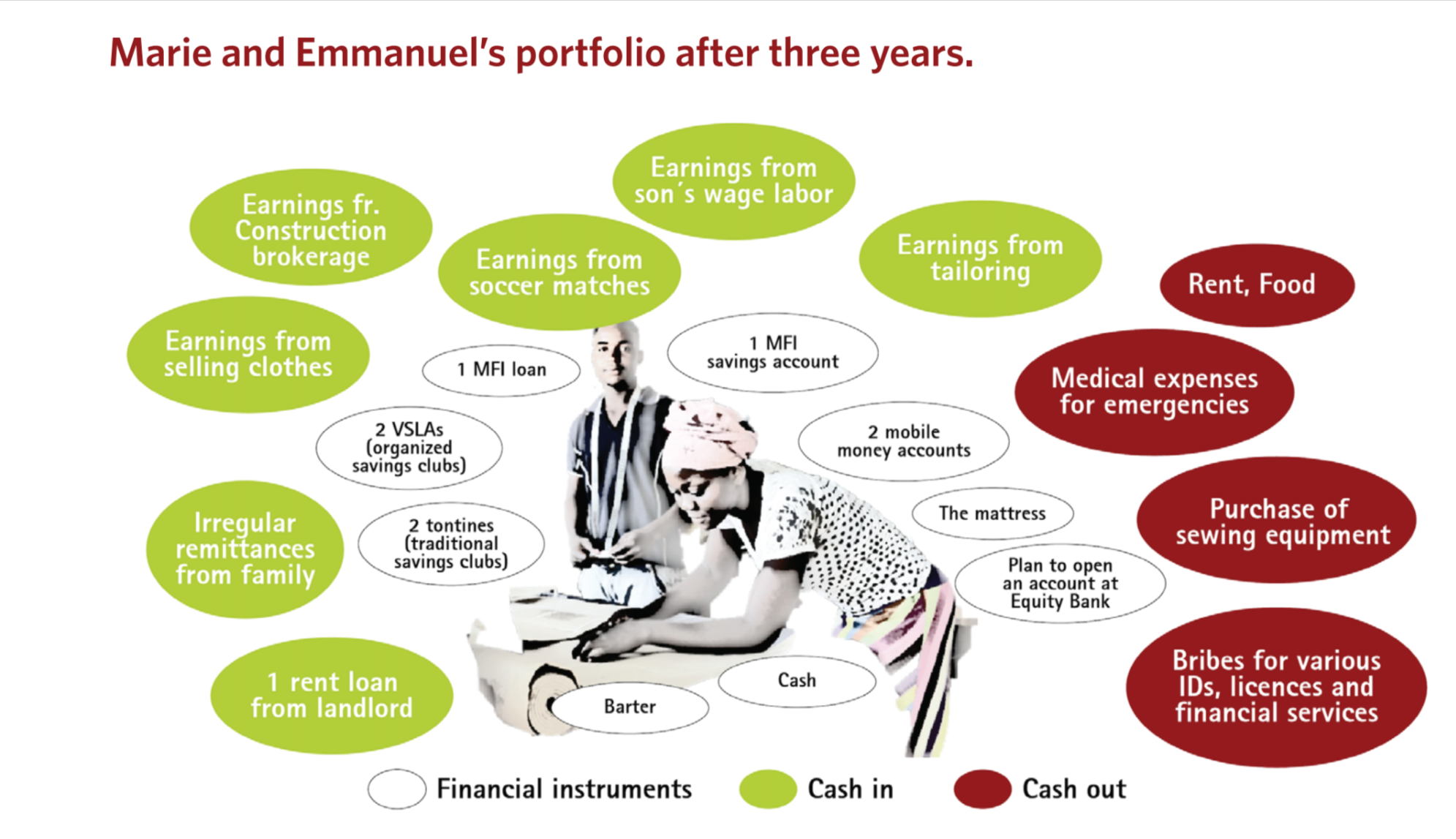

But over time, as they found their financial footing, their sources of income expanded, as did their earnings. Expenses and investments also grow. And to manage more income, they widened their use of financial instruments. Eventually, their portfolio included membership in traditional and NGO-formed savings clubs (tontines and village savings and loan clubs, as well as microfinance savings loan accounts. And they looked forward to opening an account with Equity Bank.

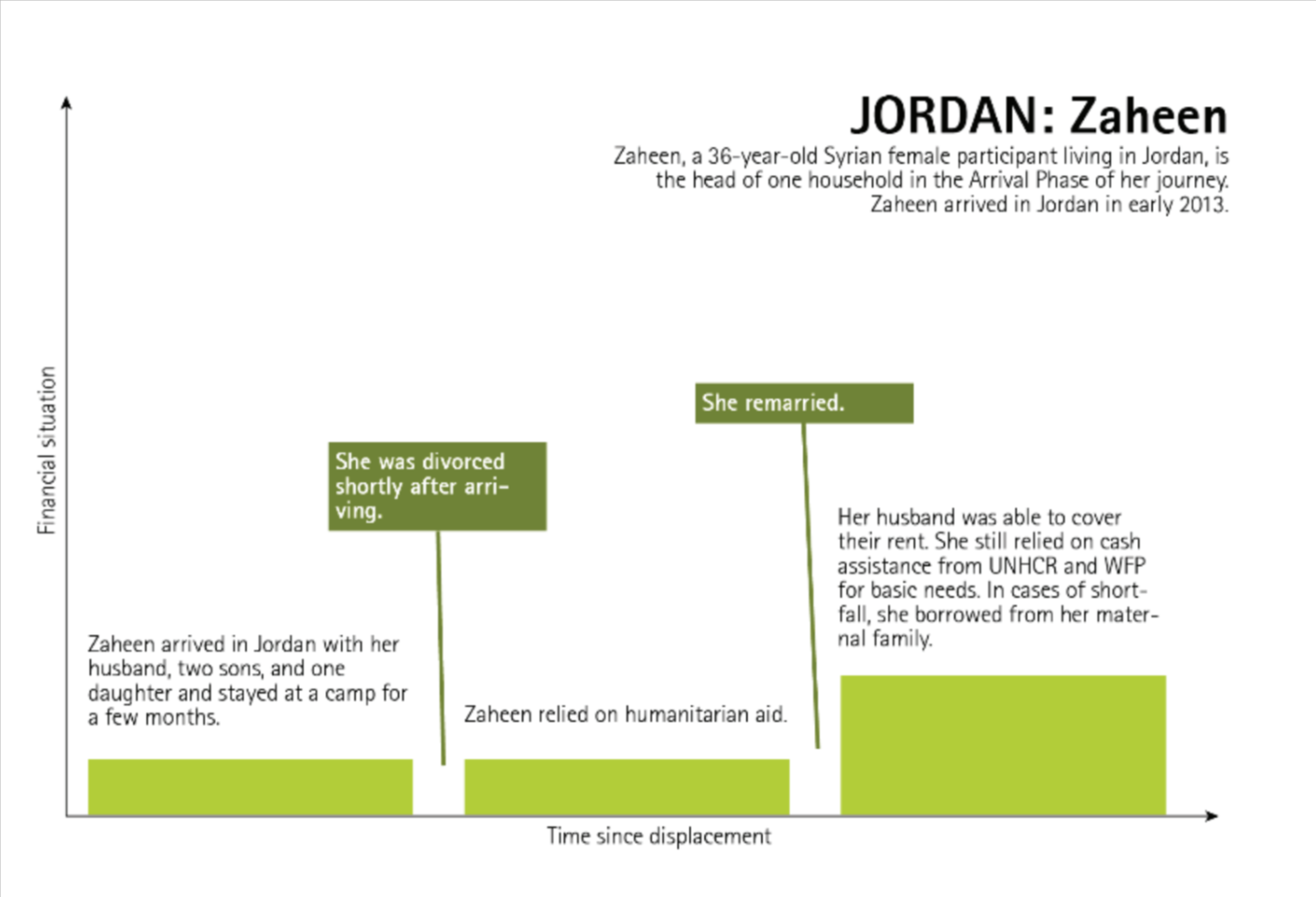

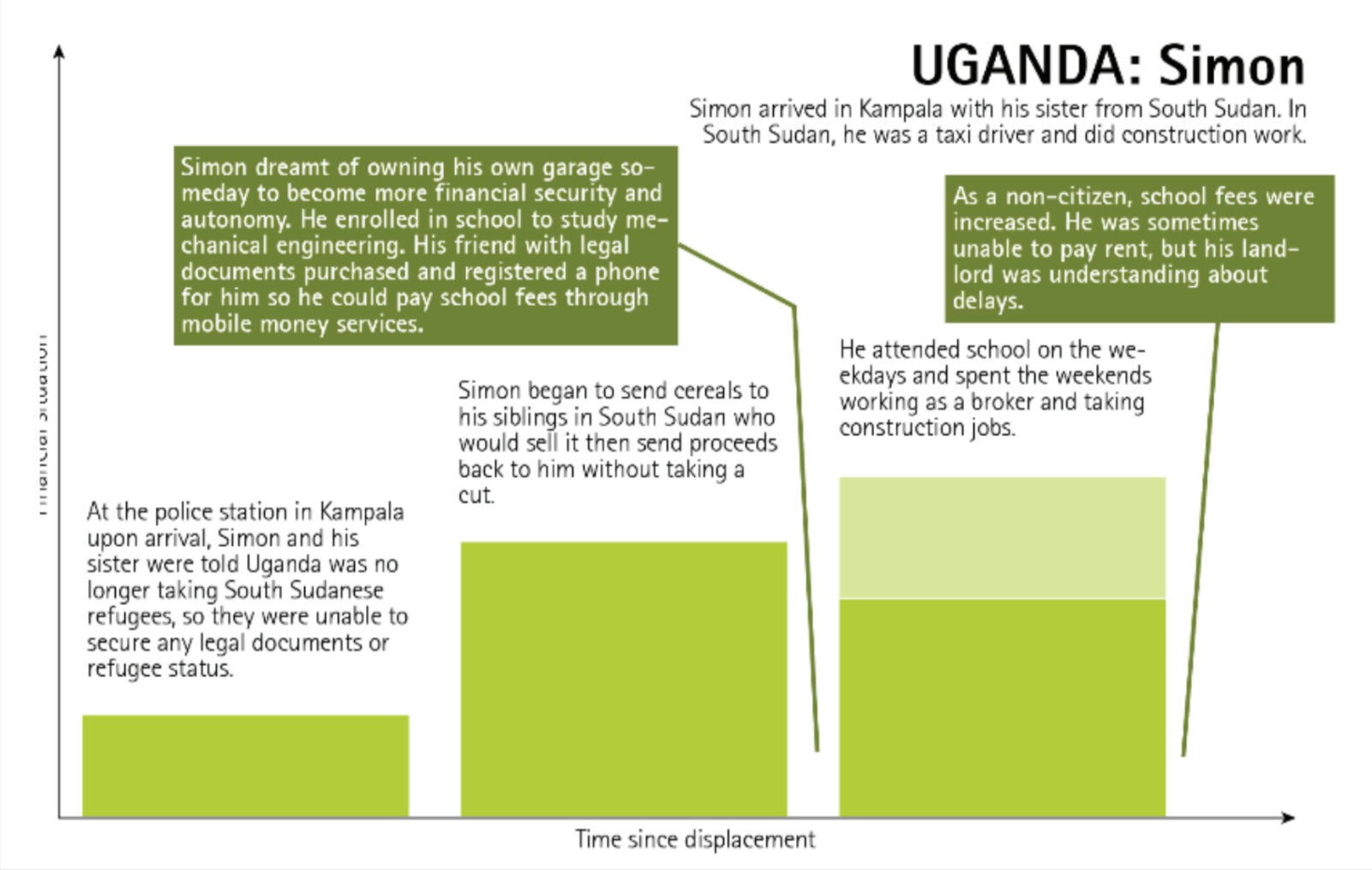

Scenario B: Urban Progressions in a Less Welcoming Economy

We’ve seen how refugees have been able to find success in welcoming economies, but how have they fared in less welcoming (“Scenario B”) economies? These are environments in which refugees and migrants have massive work and mobility restrictions, as well as obstacles to obtaining basic necessities like a SIM card. In urban environments in Jordan and Kenya, we did not observe the Ratcheting Phase taking place. With few exceptions, most would be stuck in the Survivelihood Phase, their options and activities flatlining, never reaching the Ratcheting Phase. Worse, many would see their income-generating activities decline or inch along in fits and starts. COVID-19 only worsened their prospects. We, therefore, renamed this phase in these contexts to “Livelihood-Chasing” Phase—chasing livelihoods that produced paltry and usually very irregular incomes.

Shortly after refugees and migrants arrived in the city, they depended heavily on charity, remittances, and support from others in their ethnic communities. Those who arrived with some money or other assets spent them as they adjusted to city life, tried to overcome the trauma of their journey, and found a place to live. Sometimes they were lucky and found a low-paying job quickly, such as informally working as a security guard (which paid about $60 per month). As they adjusted, they would often find what we call “survivelihood activities,” where they could patch together informal work, like cleaning a church, doing laundry, or street vending, to help contribute to shared living expenses. Such work rarely left much for savings, and refugees continued to struggle to contribute to rent and regular food expenses.

Some, but not all, graduated to finding more lucrative forms of self-employment, such as working as a barber or a musician, trading second-hand clothes or shoes, hawking fabrics or bedsheets, and selling cooked foods or running small restaurants. However, very few of these efforts turned into long-term enterprises. Instead, they frequently started, sputtered, and stopped. So instead of becoming trained and growing a single business, refugees often found themselves starting over in entirely new fields after recurrent setbacks. Below, we can see how livelihoods fail to progress in a less welcoming economy:

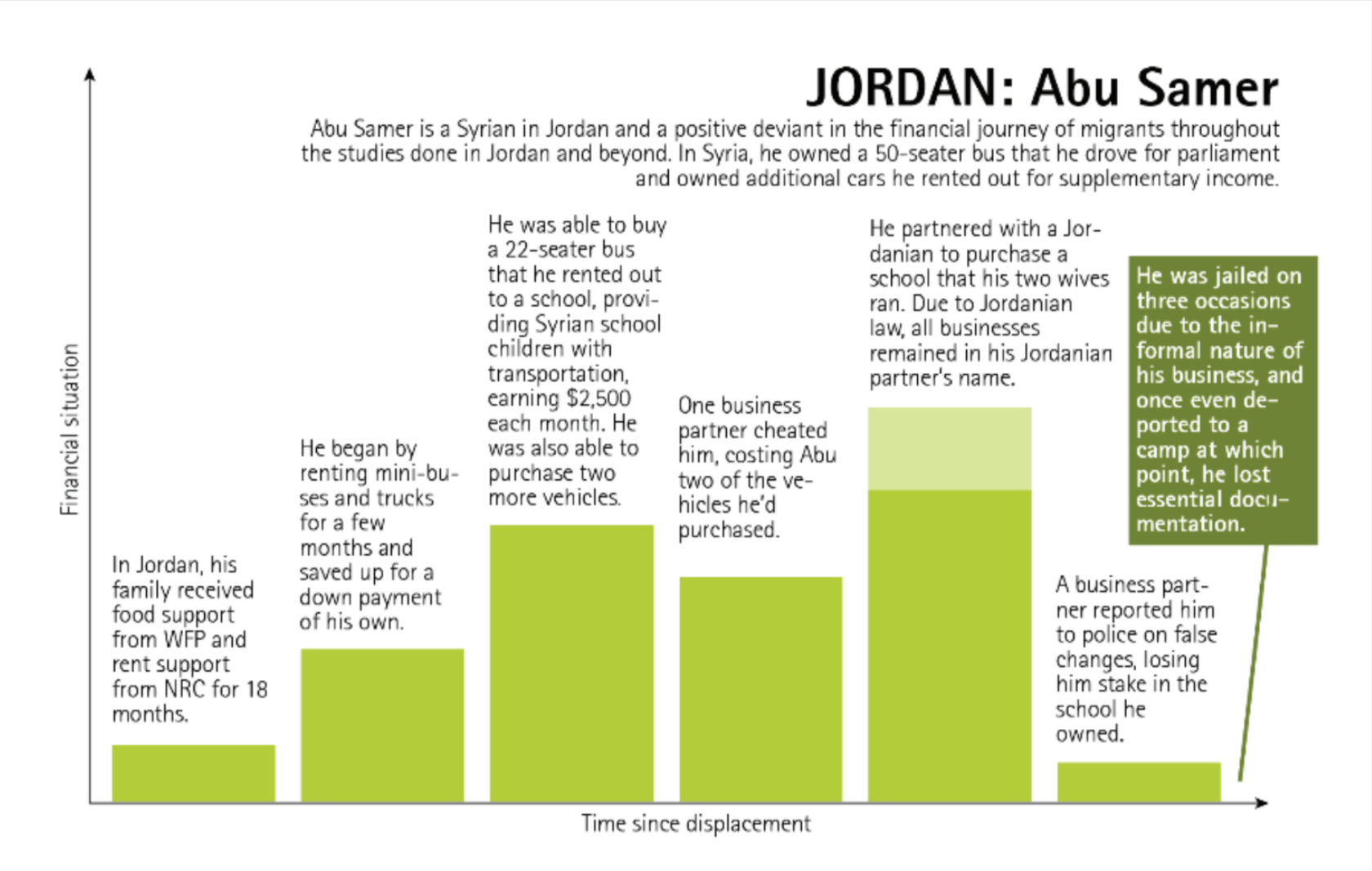

We observed examples of positive deviants in all sites, refugees who could make a go of things despite their circumstances. Initially, for Abu Samer (a Syrian in Jordan), livelihood prospects seemed promising. He was able to achieve prosperity through frugality, creativity, and hard work. Yet over time, those prospects became less promising. We can see this in his story below:

Abu Samer, a Syrian, was doing well and lived a textbook example of “ratcheting.” He managed to have diverse income streams. He was ferrying Jordanian and Syrian children to school, buying a school in partnership with his Jordanian contacts, running the canteen at the school with his two wives, selling vegetables using his pickup van, selling bread to the families of the Syrian children he transported, and working on farms with his entire family during summer months.

He also took many risks; he bought mini-buses and pickup vans under the names of his Jordanian partners (having a Jordanian partner is required by law for Syrians to open a business), even investing in the school bus without a legal contract for his investment. This allowed him to quickly grow and diversify his income streams—some big and some small. His family’s frugality funded all this entrepreneurship: Abu Samer and his wife and children sacrificed luxuries, like buying costly beds, and instead opted to sleep on the floor.

But, over time, Abu Samer was hit with one setback after another. He lost his mini-bus to unscrupulous local business partners and was even deported to a camp. After each setback, he managed to start again. Then the pandemic arrived. With COVID-19, Abu Samer lost his primary income source as the schools remained closed. He has been able to suffice financially, selling vegetables from his pickup van. Still, he was not optimistic about his future. Last we talked with him, he was hoping to be resettled in Canada.

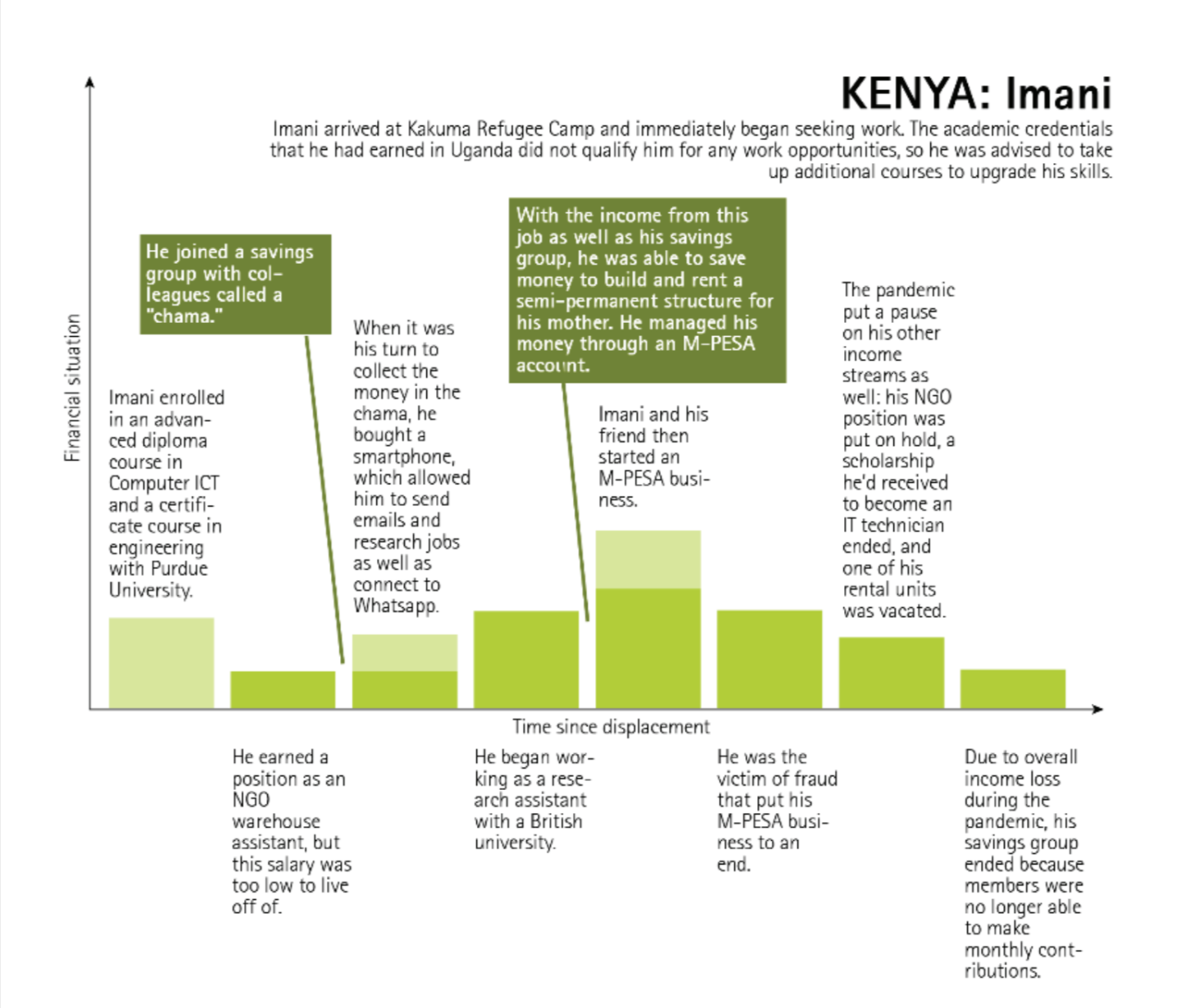

Camp Progressions

In Kakuma settlement in Kenya, restrictions made life difficult, but the surrounding economy offered possibilities, especially with regard to schooling. However, unlike Bidi Bidi, refugees were not given a plot of land to farm, nor were they given work permits (except for limited opportunities in teaching and volunteering). Refugees were meant to work in the camps, but not outside them. People did operate small businesses, but exclusively for camp clientele. This made entering a Ratcheting Phase challenging, if not impossible. See below to read Ali’s story, which shows how the ratcheting process can collapse:

Ali and his family fled from Somalia in 2011 and relocated to Kenya’s Kakuma refugee camp—leaving behind their father’s shop. The shop was a golden goose that brought in $500 per month, enough for the family of five to live comfortably.

Now 22, Ali relays their story:

“In the camp, it was hard for my dad to start a business. He was used to running shops, but to do that, he needed a lot of capital—something we definitely did not have. My father got the idea to serve as a sort of facilitator and advisor to a large number of shops within the settlement. He helped them link to and manage suppliers, which improved shop sales. From this, he was able to create a salary for himself of about $200 per month. He saved as much as he could, so he could start his own shop, attached to our house, after about a year.

“Once my father’s shop was going, things got better. But in late 2014, gunmen broke into our home and ordered us all to lie on the ground. My father screamed, and they stabbed him in the belly. He fell to the floor moaning while they looted his shop completely, ordered my mother to hand over her savings, and then raped two of my sisters right in front of us. My mother pleaded with them to stop, to just take what they wanted, but to leave the girls alone. I will never forget my sisters’ cries. They left with all of our things, all of our money, and my sisters’ lives as they knew them.

“They survived but are still in therapy. It wasn’t just the rape they had to endure. People immediately blamed the girls for what happened, even when they were still in the hospital with my father recovering.

After this horrible incident, UN officials came, promising to start the process of resettlement, so we could be safe. It took three years, but we were approved to go to the USA in 2017. But before we left, we were told that America had banned immigrants from Somalia from entering the country. Once one country has approved you for resettlement, no other country can take you again. So that’s it. We are stuck in this tiny hell.”

In Bidi Bidi, Uganda, livelihood stability is tenuous at best. Food rations do not always arrive on time and sometimes not at all; many inhabitants are left to scramble.

We were able to observe minimal livelihood development in Bidi Bidi. We did find exceptions that might light the way for others, but believe that conditions were such that the chances of thriving in this camp setting were rare. Kadi’s story below is one of those exceptions, but it should not be taken as a blueprint for success.

Kadi arrived in December 2017. Formerly married to a Ugandan man, she left him and now cares for their seven children. In South Sudan, Kadi sold cooked food and groundnuts, which netted her about $20 a day. She was doing well. When she reached Bidi Bidi, Kadi bought five goats from other refugees who had brought livestock with them to the settlement. Each goat cost her about $13.50. Kadi then exchanged the goats for a cow that she kept in the care of a Ugandan herdsman who tended other people’s livestock for a living.

Their arrangement was that after the cow had birthed three calves, Kadi would give the herder a goat. Her cow, worth about $165 at the time of the interview, had not yet had a calf. But Kadi needed immediate income. She still had some funds left after her initial expenses and used them to buy tomatoes to resell. However, the margins were too slim to continue, so she liquidated her food rations and sold them to local Ugandans. Kadi was able to net a little less than $5, but it was enough to cultivate a plot of land to harvest chia.

Barriers and Enablers to Robust Livelihoods

Across all sites, we observed barriers that prevented people from livelihoods that paid well and were dignified, two priorities for our respondents. Those barriers supported our key finding that fundamental economic rights must be in place for livelihoods to develop. Without such foundations in place, other services (such as training programs and financial services) have a reduced, marginal, and short-lived impact. Below, we have identified a few key barriers that must be overcome if refugee livelihoods are to grow.

Burdensome, Expensive, and Sometimes Inaccessible Documentation and Permissions

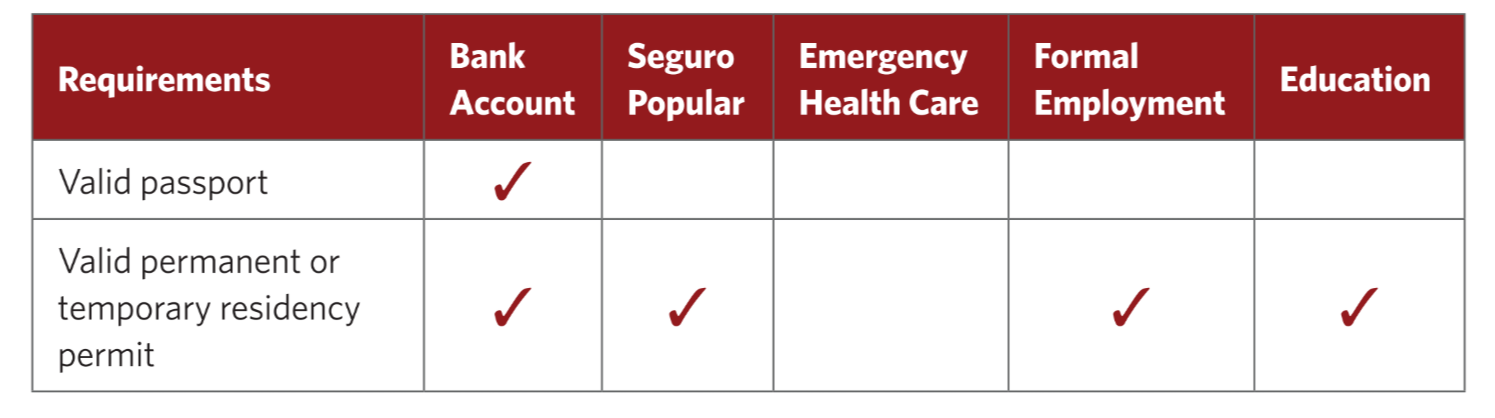

Nearly every conversation we had in all four sites highlighted the many attempts that refugees must make to secure documentation. To drive a vehicle, rent an apartment, enroll a child in school, open a bank account, visit a health clinic, purchase a SIM card, or retrieve a remittance and countless other tasks, refugees and migrants had to have proper documentation. This includes not just state-issued documentation but documentation that locals and various registries accepted.

Somalis in Jordan offer an example. Accomplishing the smallest of tasks, such as buying a SIM card, was out of reach because to do so required a passport. Getting a work permit was next to impossible, and the consequences of working under the table were harsh. One spokesperson said, “When police detain Somali refugees, they are investigated and treated unfairly as if they had killed someone. Somalis have not done anything wrong except working illegally to cover their living expenses.”

Refugees in Kenya experienced similar red tape. As one respondent said, “I went [to the UN offices] time after time for interviews, and it took me a whole three to four years to get both [a refugee ID card and alien card]…. The process is tiresome!” With or without documents, refugees—especially men—encountered persistent harassment from police who demanded bribes to allow them to simply exist. Refugees registered in the city were not allowed to move outside Nairobi without written permission. Similarly, those in camps could not leave without written permission. Government resistance to integrating refugee identification into national ID systems denied refugees in Nairobi the right to register a SIM card in their name, register a linked M-PESA mobile money account in their name, or obtain other documentation necessary for earning a living, such as certificates of good conduct.

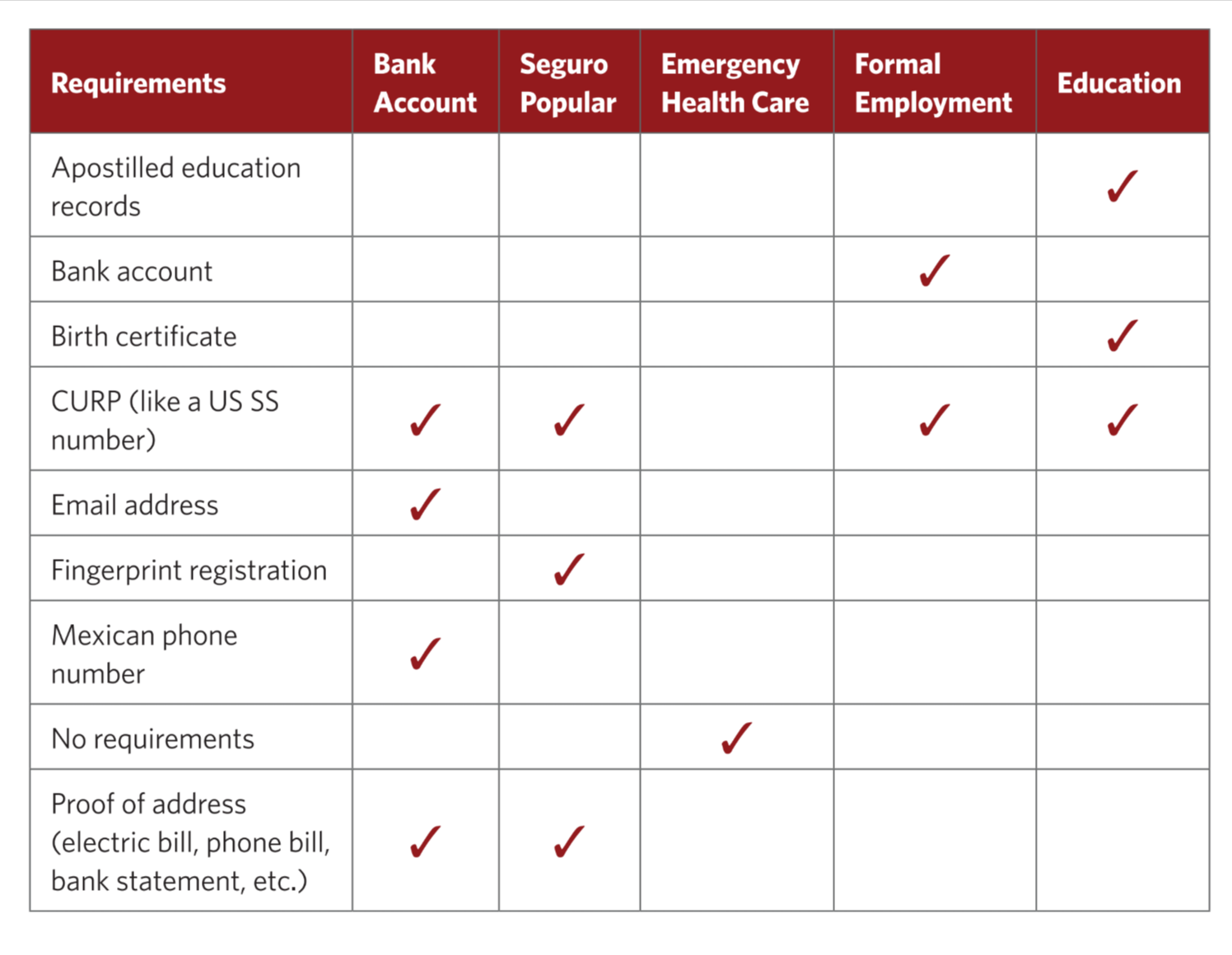

The table below—taken from research in Tijuana—illustrates the confusing maze of documents required to access a particular permit or service.

In Mexico, if a bank employee suspected a migrant was using their account for illicit purposes, the employee could request further documentation. The suspicion did not need to be supported by any evidence and was entirely at the employee’s discretion. A consular official from El Salvador said he had been denied a bank account because he “lacked credibility.”

Social Networks

Social networks included both “bonding capital” (bonding with members of your own community or group) and “bridging capital” (bonding with members outside your community or group), which grew from networks that included the host population¹⁰. When both were robust, the social networks for refugees did much of the work traditionally done by financial services. Members of a social network invested capital in starting up or expanding businesses. They also helped manage financial risk, providing food, housing, or cash (as gifts and loans) during difficult times.

In Jordan, Syrians had the closest connections with Jordanians. Respondents agreed that the similarity in cultures, shared language, and tribal affiliations strengthened these connections, giving Syrians access to jobs, business opportunities, links to suppliers, and financial resources.

In Kenya, social networks grew out of previous customs. For example, many of the Burundian and Congolese refugees identified as Banyamulenge and on arrival sought to connect with others from their tribe to help them learn how to navigate the city. They found community through churches in neighborhoods where others from their ethnic group had settled.

There is a long legacy of Somali settlement in Nairobi, and most of our Somali respondents were able to plug into those established networks in the city. Unlike Ethiopian networks, the Somali networks typically included close family connections. In some cases, respondents were able to leverage networks to start and grow businesses. Some of our respondents relied heavily on the communal practice of shaxad, in which other Somalis donated money for needy recipients’ upkeep.

For many (though this is less true for Somalis), refugee social networks in Nairobi were not particularly diverse. They tended to have a low capacity to provide financing and connections needed to navigate shocks to start and expand businesses, invest in education, and pursue new opportunities. While refugees were more likely than Kenyans to have a source of international remittances, for many, those could only be called upon in times of genuine crisis and were not particularly useful in providing capital for income-earning opportunities.

In Mexico, the differences between Haitians and Central Americans were stark. Haitians appeared to have more robust community networks, both in Tijuana and abroad. Haitians tended to live close to one another, establishing networks and small communities within Tijuana that fostered greater integration. These tighter networks among Haitians supported members with investment funds and helped them find places to stay. As Haitian migrants arrived in Tijuana, they began to form close-knit communities that served as informal centers of information and resources. Conversely, Central American migrants failed to develop these networks and were spread throughout the city, unable to rely on one another. This dynamic presented challenges not only for the Central American migrants themselves but for the organizations looking to serve them.

Business Capital

Demand for grants or investments in business startups began to appear in the Survivelihood Phase and matured in the Ratcheting Phase, where ratcheting became possible through loans and microloans. While we met respondents in Uganda who could use loans productively, we also met respondents in Jordan, who, desperate to make ends meet, would use their loans for consumption purposes. Borrowing was risky for refugees not only because of the risks they already faced by being refugees, but because of new dangers caused by opening a business. Authorities could shutter a business with no consequence or force the business to move. Locals could exploit the refugee partner for personal gain. Any of these activities could produce business failure.

Safety from Exploitation, Discrimination, Violence, and Harassment

Harm took place in multiple ways in both urban and camp settings. Let’s begin with exploitation and discrimination. Such threats took various forms, from wage theft to a relentless demand for bribes. Refugees would find work time and again from members of the host community and complete the work as planned, only to find that their employers would pay them half of what was owed or sometimes nothing at all.

To illustrate this, we turn to Abbas, one of our Yemeni respondents in Jordan:

Abbas, a male Yemeni in Jordan, found work through Open Sooq, a job-matching platform. He explained, “I just put up an ad online saying: ‘Yemeni looking for any work.’ But I found work in [the] Dead Sea and all faraway places. I worked with a man in January 2020 for four days to install solar energy panels in Aqaba, Karak, Irbid, and Dead Sea. He was paying me about $35 a day, and I worked for four days. But he paid me for only two days. I could not do anything about this.”

The informality of his work left him without a way to contest his circumstance. Legal support organizations claim that refugees have the right to contest this, even without a work contract. However, most of our research participants (except one Syrian and one Sudanese) believed this was impossible.

Wage theft was also widespread in Mexico. A woman from Central America reported that she had worked for a woman downtown, caring for her children and cleaning her apartment. “The work was really tough,” she said. “I had to care for the two kids, do all the cleaning, do her laundry, grocery shopping… I would even bring my own food.

She said she would pay me $60 a week. When the time came, she only paid me only $34.78. I thought maybe she would pay me the rest later.” But she never did. Her story parallels Abbas’s. She received about half what was promised.

In Kenya, exploitation was just as commonplace. Respondents complained about wage discrimination or being cheated out of their pay because of their refugee status. This encouraged some to conceal their nationalities in order to find fair wages. One refugee respondent worked as a mechanic and reported that clients often tried to underpay him when they realized he was foreign. He was proud of learning to copy the Kenyan dialect so that he could pass more easily. He had one repair job that brought in $500, and he believed that he was able to ask for this kind of money because he passed as Kenyan.

Violence and harassment were pervasive in our studied communities. We explore in more detail how women face violence in harassment in the Gender section of this report, but it’s important to emphasize that the need for safety and protection was not exclusive to women. Refugee men faced persistent harassment and extortion from locals and the police. Our female respondents in Kenya and Jordan reported minimal police harassment and agreed that the police targeted male refugees. Respondents believed that the reason why the police target men is that they are the ones with money who can readily pay bribes. One of our South Sudanese respondents told us his story of police abuse:

Our respondent and his brother used to work informally at a car wash and would leave work just after midnight. They were arrested more than three times without cause as they walked home:

“They don’t even take you to the police station; they just tell you, ‘Just give us something before we take you in.’ You personally, you know, if you get inside a police station, it will be a different thing. So, if I had made $9.00 (KES 1,000) that day, I gave them $4.50 (KES 500). Last time there was a meeting with refugees and the police, and I complained about this. The big boss said I should come to the station and report them. Now, if I go to the police station and report it, and then they know who I am, won’t it make my situation even worse? They can even kill you… Once, they stopped us on the way home and claimed they saw my brother buying drugs. They took him to the station, beat him, even wounded his eye. They were telling us to bring $180 (KES 20,000), and Mum said, ‘Okay, do whatever you want with him.’ After they realized these people were not playing, they said, ‘Okay, just bring what you have.’ We tried and told them we only [had] $18 (KES 2,000). They said ‘No, come with $73 (KES 8,000).’ So we went and looked for $45 (KES 5,000). Once we gave them $50 (KES 5,500), they let my brother go.”

The threat of violence had an enormous impact on our respondents’ economic lives. Fear of being attacked led people to pay rents higher than they otherwise would. In all sites, respondents sought to improve their quality of housing as quickly as possible. An individual or family would often start out by sharing a cramped space with many others in a low-income residential neighborhood. But, after experiencing repeated threats or hearing stories of violence, they would come to prioritize safe surroundings—that naturally came with higher rents—over other essential expenses.

Waiting for Resettlement

Perhaps the most significant barrier to integration in Jordan and Kenya was that refugees, seeing a lack of long-term solutions, were holding out in hope of resettlement. The prospect of durable solutions (such as pathways to residency, work permits, and freedom of movement) was absent in these sites. With no visible future in the given settings, refugees were left to bide their time until something better came along—possibly resettlement to a third country. Ideally, they would relocate to a more economically vibrant destination like Canada, Germany, Australia, or the US. Consequently, many respondents in Jordan and Kenya had little motivation to invest in where they were.

This sentiment was very prevalent among our respondents in Kenya. About 73% of our respondents there hoped to be resettled to a third country. Though the process was slow, they were still excited about resettlement. They believed that in a third country, they would be afforded full rights to move, work, and build their lives in perpetuity, in contrast to the uncertainty they faced in Kenya. The preference for resettlement was not only about the lure of places like the US and Canada but also the freedom to build a full life. In fact, 12% said they would like to stay in Nairobi and be granted permission to remain indefinitely, preferably with full rights to work and move.

Because of their current uncertainty, very few respondents were investing in long-term businesses, property, or other assets. As a result, many are left in a state of perpetual waiting, further discouraging productive investment. Instead of trying to start or grow a business or purchase productive assets, like equipment for a restaurant or a motorbike to ride as a boda driver, respondents were more interested in the kinds of work that would help them get by and were wary of things that felt too permanent. One told us:

“I believe I will one day be resettled even if I am not 100% sure. That is my only hope and the only reason I keep on fighting. I know [that sooner] or later I will be resettled and have a country which I call my country, where I will have all the rights just like any other citizen of any country.”

In Jordan, non-Syrian refugees held similar outlooks, with one additional twist: they would have to give up their work permits in exchange for the possibility of resettlement. A Yemeni man told us, “I know this from other Yemenis I used to work within Sahab (a neighborhood in Amman). They told me that UNHCR asked them to either cancel their permits or their UNHCR registration. Most of them canceled their UNHCR registrations because they have stable jobs. I want to keep my UNHCR status. I want to travel to get another nationality. My country is not okay, and I can never go back.”

Refugee women in Jordan faced dire choices. For some, returning home was the only option when resettlement became elusive. While they did receive assistance from UNHCR, it was not enough to meet their needs. See below for our respondent, Sahra’s, experience:

Sahra, a Somali single mother, provided a telling illustration of the resettlement process. When asked during our second interview, Sahra said worryingly, “I do not have any resources. Not even a small amount that I can benefit from to get me through the coronavirus crisis. I do not have anything to sell, and I do not have any money to save. I do not have anyone to support me from any other direction. Even amongst friends, there is no possibility of taking a loan during the crisis. Everyone is going through the same difficult circumstances.”

When we met Sahra again for a final interview, she was struggling to pay her children’s school fees and feared that they would be expelled. She still had outstanding debts to both the corner shop and her landlord—she had no other option but to wait for winter assistance (a lump sum of cash to help refugees prepare their places for winter) to pay them off. A few months later, she moved back to Somalia. Her family helped her pay for the travel. This was an incredibly difficult decision—she had stayed in Jordan for seven years, waiting for resettlement, and all her struggles had been wasted as she returned to Somalia. Her family decided the next steps for her—she would remarry her ex-husband (the primary reason she fled) and reunite with him in Kenya to make a fresh start.

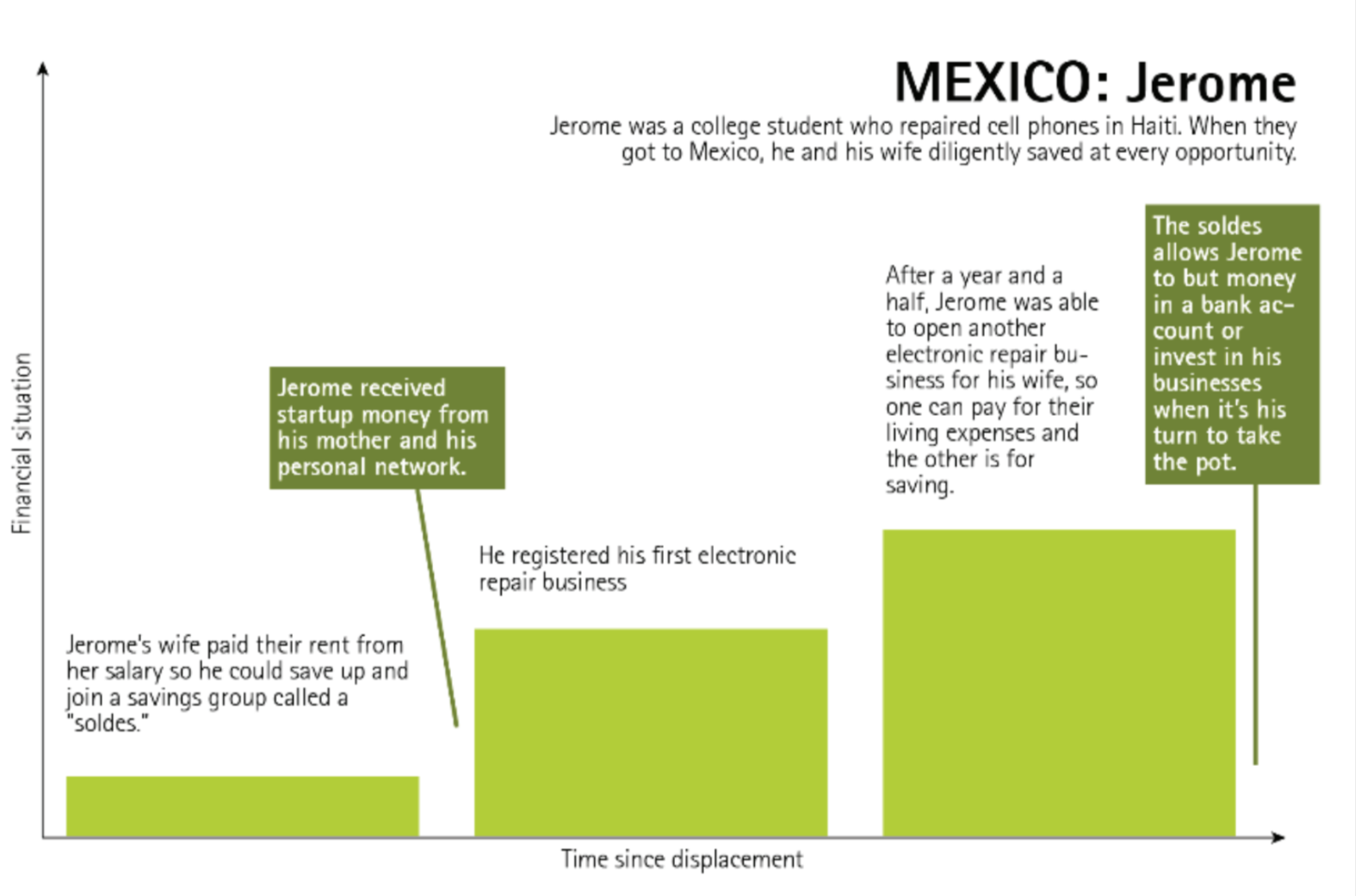

These are the experiences of refugees and migrants in less welcoming economies. But what about those in more welcoming ones, such as Uganda and Mexico? The refugees in those settings had a range of stories to tell. Yes, some wanted to be resettled, but many were happy to stay and make a life for themselves in their host community. Jerome, a Haitian business owner in Mexico, concluded:

“I’ve decided to stay in Tijuana for the long-term. The only reason I wanted to go to the United States was to make money, but here, I’ve found 90% of what I wanted. I have a stable salary, I can provide for the needs of my family, and I can save money and progress in life.”

Skill-building and Mentorship

Language skills were vital to finding a mentor, and in turn, mentors were key to gaining a foothold in the local business community. Respondents often talked about how helpful it was in Kenya to be taught the business by someone who could show them the ropes.

Respondents valued the trainings they were able to attend and, when available, the opportunity to be mentored by a local. Those who were able to develop their language skills quickly saw their business and job opportunities expand. Whether it was Iraqis in Jordan perfecting their Levantine vocabulary or Haitians in Tijuana adopting a distinctly Mexican accent, the ability to speak the same language as the host population (ideally with the same accent) was a boon. In Kenya, Congolese and Burundians were known to adapt their Swahili quickly. This was important because having a Kenyan local as a business partner could amplify their chances of becoming legitimate. The same was true in Mexico. Wilson, a French teacher in Tijuana, believed language not only helped you get by, it helped you integrate. He summed it up:

“In order to integrate more into the community, I distance myself a bit from the Haitian community, even though I serve it. If I’m only around other Haitians, I won’t learn Spanish, and I need Mexican friends to help me speak Spanish.”

Trainings in competitive fields were valued less by respondents. This was particularly true for a camp setting. For example, in Uganda, NGOs provided livelihood support that included lessons in tailoring and other services. However, the challenge for small businesses in Bidi Bidi was that there was no demand for items beyond household necessities. One South Sudanese in the camp, after a business training, opened a store that offered fresh juice and food but found little demand for his items: “There is no market, no money for the people to buy items, so I plan now to close.”

But in the same setting, trainees appreciated NGOs that had identified market niches and were training refugees to fill them. For example, Danish Christian Aid trained refugees on mushroom farming. One respondent was in a group that collectively farmed oyster mushrooms. Each kilogram brought in about $2.70. The farmers liked the process because it takes about 25 days from preparing the spores to harvesting the mushrooms, and they can be harvested year-round. What’s more, it’s a skill that can be transplanted to another setting.

In Nairobi, refugees got little value from skills training for another reason: they were not legally allowed to work using the skills they gained. One respondent, for example, was put through college in electrical engineering with support from an NGO. But when he was offered a job after his internship, he could never get approval for a work permit. He has been waiting for more than two years to get a response on the permit, and the job offer has long since been withdrawn.

Gender and Livelihoods

In our research, we saw women across all nationalities taking on new roles and responsibilities—going out in the public sphere to find work, interacting with aid organizations, police authorities, and engaging in different forms of paid work.

Women respondents dealt with multiple challenges unique to their physical limitations (affecting their ability to secure jobs in construction and public works), their limitations as caregivers (affecting their ability to commute to a job outside the home), and safety issues (women refugees saw themselves as targets of violence). This meant that they had fewer opportunities than men, and as a result, many women were restricted to home-based businesses or small-scale retail located close to their homes.

Shifting Gender Roles

We met women who, as heads (or co-heads) of households, gained new confidence as their economic and social roles changed in displacement. They contributed to family income, participated in financial decision-making, invested in their children’s education and their own skill-building, and expanded their social networks. But these successes were the exception.

More commonly, we met many women (single mothers, young mothers, or de facto heads of households where male members could not work) who struggled to make ends meet, hoping for relief in the form of cash assistance. Even with economic opportunities and occasional gains, their restraints (such as childcare, safety, and social norms) stifled the possibility of growing their livelihoods into meaningful income streams.

Women’s lower incomes and reliance on spouses created acute vulnerabilities. Our female respondents’ financial journeys were interrupted by the challenges that come with getting married, divorced, or separated. And while limited by the challenges, they also spoke of how the act of overcoming these obstacles gave them a tremendous sense of achievement confidence. We observed that older women were more confident than younger ones, having earned their confidence from years of displacement.

The story of Jamal offers an example of the barriers that refugee women face in obtaining financial stability:

Jamal, a thirty-year-old Syrian respondent in Jordan, experienced multiple turning points caused by changes in her family status. After she had to stop working to give birth to her son, her husband started his own shop. The shop brought temporary financial relief, but soon created significant financial losses that weighed heavily on their marriage. The couple ultimately divorced, and her husband took sole custody of their son, devastating Jamal.

Over time, she secured cash assistance (through cash grants) and began investing in skills to broaden her work possibilities. She even registered a small business with her savings and support from her social networks. But, after getting engaged, her fiancé didn’t want her to work, so she shuttered her shop. When her fiancé became impatient with the drawn-out security clearance process through the Ministry of Interior, a precondition to register her new marriage, she was left without a business or a husband. When we last interviewed her, she was working and skill-building, drawing on her confidence and determination to support herself. Still, she hopes that a future marriage will bring more stability to her life.

Safety

Single women’s experiences with and fears of violence limited their prospects for building financial health. Single women lived in fear of their safety and that of their children. We heard numerous reports of violence that had taken place on respondents’ physical journeys of escape as well as in their new neighborhoods. Rape and child kidnapping were common enough to keep women constantly on edge. For example, one of our respondents in Uganda, Halima, voiced her fears about what could happen to her children should they leave the house. She had three children, all girls, none of whom were enrolled in school despite Hamila’s ability to afford tuition. “They may be raped on the way to or from school,” she lamented. There were other stories, too, even more disturbing than Halima’s. Our respondent, Eunice, offers an example:

Eunice, a Burundian in Uganda, sheltered in a church for three years. She struggled daily to provide enough food for the children in her care and was selling cassava leaves to support her family. One day, a fellow Burundian acquaintance offered Eunice a portion of flour that she could use for cooking. When Eunice arrived at his home, the man raped her. She reported the case to the police, but the man had fled and could not be found. A month later, Eunice learned that she was pregnant by the rape.

Devastated, she struggled to make ends meet by relying on church donations. She opened a make-shift kiosk outside her living quarters and sold vegetables, earning less than $1 a day. She calculated that a more traditional job would be difficult to perform while she was breastfeeding.

In Tijuana, Mexico, many women expressed similar fears about being on the streets because of the city’s reputation for violent crime and kidnapping. Women were reluctant to venture out of the shelters, making it difficult to find work. One of our Salvadoran respondents who sold candy on the street reported how a man had grabbed her daughter by the arm. “I grabbed her other arm and started screaming. A man in a business across the street ran over, and the man trying to take my daughter ran away. After that, I was scared to keep selling candy… What I make won’t be worth the possibility of someone kidnapping my daughter. What would I do if that happened? Here, the police do nothing.”

In Tijuana, as in other research sites, trusting a stranger with childcare was not a viable option, a sad truth that forced women to depend on migrant shelters to cover their basic needs. There were a few shelters dedicated to women and children, which supported women with childcare. These shelters operated well above their capacity, leaving many migrant women underserved.

Collectively, these experiences resulted in several strategies being deployed by single women. First, find shelter that is secure, even if it costs more. This adds to the burden of earning extra income to support higher rents. Second, take on jobs that limit physical vulnerability, such as not working alone. And third, walk children to and from school (further curtailing livelihood options) or pull them out of school altogether.

Entrepreneurship and Gender

Entrepreneurship alone cannot be a silver bullet for women’s economic participation. While entrepreneurship is often hailed as the solution to women’s labor market participation and a vehicle for empowerment, the experience of our female participants shows that the results are limited. Successful ventures¹⁴ remain an exception rather than a rule. Many women-led small businesses struggle with a lack of business skills, market connections, mentorship, and role models. When women do start businesses, they are likely informal. Their limited scale, combined with the complex business registration processes, all work to constrain their enterprises.¹⁵

Development interventions only partially tackle this multifaceted issue. For instance, many women received vocational training in skills such as sewing, but then did not receive commensurate management and marketing instruction or connections to grow their businesses. Even when women were provided equipment (such as a sewing machine), they lacked the confidence to start a business. Microfinance, rarely offered to refugees, was an option in Jordan. Still, women in our study did not feel comfortable taking formal micro-credit, given the small profits of their small-scale and craft-based businesses.

Networking and Solidarity

Women have limited avenues to build connections and collective solidarity. Social networks play a critical role for refugees as a safety net against adversity, disperse information about economic opportunities, and provide psycho-social support. Women respondents who had limited social networks had the lowest incomes in the entire sample.

We saw this play out in Jordan, noting discrepancies between the often educated and connected Syrian and Iraqi participants compared to more secluded participants from Somalia and Yemen. It was evident in Kenya as well. There is a long legacy of Somali settlement in Nairobi, Kenya. Most of our respondents could plug into those established networks in the city, typically using close family connections. In some cases, respondents were able to leverage those networks to start and grow businesses.

However, things tended to be more challenging for female respondents who had previously been dependent on other family members, only to find themselves thrust uncomfortably into public life. Some relied heavily on the communal practice of shaxad, in which other Somalis (even without a personal connection) donated money for needy recipients’ upkeep. The importance of social networks is pervasive.

Humanitarian interventions in some of our research sites (such as Jordan) included trainings and awareness sessions provided by various organizations. Women appreciated the safe spaces to interact socially and build new contacts, which were an essential source of information. But many judged such connections as superficial, short-lived, and not conducive to more robust networks for mutual support or collaboration. Their support remained limited but did serve a need for temporary social distraction—relieving them from thoughts of constant hardship.

Women also had limited avenues for collective action. Given the change in the socioeconomic roles of refugee women and their fragile context, collective action could help challenge the social norms that constrain women’s engagement and address development problems (such as access to savings and business capital or childcare).¹⁶ It could also help promote role models and leaders from the community to inspire broader social change and campaign for legal rights.¹⁷

However, building collective action and solidarity requires a supportive legal and social environment. Today, refugees in Jordan are not permitted to form an association or become members of an association or cooperative. This limits their ability to cooperate for economic or social activities, even when there are preexisting ties based on nationality, tribe, or religion.

Male Emasculation

The support of male family and community members is crucial in protecting women and supporting broader social change. Our study (along with previous studies) found that men, especially those in the working-age group, often fell much lower in the hierarchy of humanitarian assistance.¹⁸ They are expected to be financially self-sufficient or at least be able to achieve independence with fewer difficulties than women.

Women often found themselves as the primary earner, chiefly due to divorce, death, or split families. They immediately understood that they could not put food on the table if they did not make a wage or run a business. They quickly abandoned any concerns about taking on work that did not match the skills they had honed back in their home countries. Men, on the other hand, were more determined to put their hard-won skills to use. But doing so in brand new surroundings proved difficult. Shifting roles caused men to either become idle or take on jobs they felt were beneath them.

We also saw limitations on men who managed to take on work. They were afraid of law enforcement cracking down on illegal work. Our female respondents in Kenya reported minimal police harassment, instead believing the police targeted male refugees, expecting men were the ones with money who would readily pay bribes to be released. While male refugees cited fear of arrest before receiving their official documentation, harassment rarely abated when a refugee had all of his documents in order.

Not being able to provide for the needs of their families, men struggled to find their identity and negotiate “respectable masculinity.”¹⁹ Humanitarian agencies may further contribute to this imbalance as they provide targeted support to women through livelihood training, psycho-social support, and microfinance, often overlooking the needs of vulnerable men.

Financial Portfolios

As with any individual’s portfolio, a refugee or migrant’s financial portfolio includes both the sources of income and the destination of payments (expenses, debt repayment, investments in assets). Because they are subject to massive volatility, we have chosen not to itemize the specific financial contents of their portfolios but only to describe what’s in them and how they might shift over time.

Income from Livelihood Earnings

For those living in the city, various income-generating activities constituted the mainstay of their economic survival. We have already detailed those activities in the Livelihoods section. It’s worth repeating that livelihoods that depended partly on volunteering (for pay) for NGOs meant low and unsteady wages. Those activities that went beyond volunteer activities with NGOs were mainly in the informal sector, such as daily wage work or self-employed activities. As such, they were subject to various kinds of exploitation, including wage theft.

Income from Humanitarian Cash Assistance, Government Programs, and Charity

We mentioned that humanitarian aid from UN organizations and large NGOs was a substantial part of the portfolios of refugees who could receive this kind of aid. Overall, we found that cash assistance alone could not revive self-reliance among the vulnerable households that organizations target. Any improvement in their financial status was temporary and was only sustained through subsequent disbursements. There were cases where some family members had access to regular employment, while others received monthly cash assistance. This combination of regular employment and cash assistance helped these families cover the rent, one of the most prominent stressors, and free up mental bandwidth and resources to leverage economic opportunities.

In some places, various kinds of assistance were offered monthly cash/voucher assistance, regular annual assistance for specific purposes like winterization, and one-off assistance from local charities and some NGOs. In Jordan, for example, humanitarian assistance grants offered by UNHCR, WFP, and NGOs,²⁰ proved crucial for survival in places where work opportunities were curtailed. Within our sample, more than half of the respondents in Jordan received regular cash assistance from UNHCR, money for food from WFP, or both. Syrians were most likely to receive this support, even though they were most likely to secure legal forms of work.

And yet, many had to get by without this kind of support. In Jordan, humanitarian cash assistance from the government or the UN was limited to Syrian refugees. Non-Syrians such as Yemenis, Iraqis, and Sudanese refugees were not permitted this kind of cash assistance, and neither, as we have mentioned, did they have permission to work.

Cash-for-work, the name given to government programs that pay wages to beneficiaries in exchange for their labor, was also seen as valuable, especially when it complemented humanitarian cash transfers and other income. Syrians in Jordan offer an example of the importance of both these services. See below for Alem’s story:

Alem is a 45-year-old Syrian refugee who lives in Irbid with his wife and five young sons. They came to Jordan in 2011 with enough savings for only one month’s rent. They thought that they would return home in one or two months. Alem used to work as a painting contractor in Syria and had workers under him. They owned their home and were doing well until the war broke out. Now, he has an issue with his back and, as a result, cannot work long hours painting. During their initial years in Jordan, when there was no UNHCR assistance, they depended on one-off cash assistance payments, donations, and selling goods.

Finally, in 2014, they started receiving monthly UNHCR and WFP assistance, which provided some stability. However, their money from work was unstable and never the primary source of income. Alem cannot find painting work during the winter, and they are dependent on the monthly cash assistance. They fear losing it.

"Our money is very tight,” Alem said. “We have a lot of expenses. Sometimes, we are short on 70-80 JODs (~$100−113) in a month. We work during that month and would use the money to pay that month. But every month, there is little debt. There were times when our debt reached 200 JODs (~$282), and we paid it. Now our debt is around 150 JODs (~$212) for water bills and other things at home.”

Income from Selling Food Assistance

A common source of income in Jordan, Kenya, and Uganda was the sale of food aid (grains and oil) for cash. Food was only distributed in the camps, which meant that the readiest market were locals near the camps. In Uganda, for example, when food rations arrived, they did so monthly and included oil, beans, grains, and salt. Most respondents agreed that the rations were too little to thrive on. To quote a South Sudanese refugee in Bidi Bidi, “We learned that the rations were meant to help us survive, not to feel full.”

Not only were the rations not enough to abate the hunger of Bidi Bidi residents, but they also lacked important nutritional ingredients. Families might make do between their own vegetable crops and the rations provided, but we could not find families that did so based on their crops and rations alone. Most sold their rations the same day they received them. They took the cash and purchased other foodstuffs, medicine, or household necessities like soap and laundry detergent.

Uses of Funds

Our respondents’ spending habits were similar to those of the host community: their chief costs were rent, daily food and medicine, clothing purchases, transportation, school tuition, and household items. What differed in our respondents’ opinion were two factors: the magnitude of housing costs and the need to budget for bribes, something they believed their hosts did not have to pay as frequently.

In all sites, rent was the most significant expense and stressor. Housing was critical to our respondents’ safety, and they worried about being evicted by their landlords. Rents in Tijuana were far higher than what our respondents were used to paying in their home countries. For instance, a one-bedroom outside of the city center in Tegucigalpa, Honduras, is $288, versus $500 per month for a one-bedroom in Tijuana.

Most were unable to find housing they could afford on their own in the first months after arrival. A common strategy was to share rent with family members, friends, or fellow migrants they already knew or had met on their journeys. The prevailing stereotypes among the host population in Mexico were that Haitians were hardworking and trustworthy. As a result, landlords were more open to renting to them than to Central Americans.

COVID-19 exacerbated concerns about rent for our respondents in all sites. In Kenya, we watched as both refugees and native-born Kenyans fell months behind on their rent due to the COVID-19 crisis. But it was striking that none of the respondents in the host population were evicted from their homes during that period, while nearly 1/3 of our refugee respondents suffered eviction between June and December 2020.

Some respondents felt that landlords viewed the shock as an opportunity to replace “foreign” tenants with Kenyans—that landlords expected refugees would have fewer resources to draw on to get through the crisis and were less likely than others to rebound financially. Respondents believed that distrust also affected this kind of informal credit. Respondents felt that they were less “well-known” and were treated as a more significant credit risk to landlords and shopkeepers, not to mention more formal lenders.

For Ugandans, landlords were often patient with rent payments, as they were in Jordan. But refugees still struggled. In Amman and Irbid, respondents grappled with rent; their incomes were uneven, as many could not find steady work. And the rent was never negotiable. If respondents were unable to pay for a few months, they risked eviction. Thus, they prioritized paying off any outstanding rent the moment they received any income or cash assistance. Those who received regular monthly assistance from the UNHCR and WFP could plan for this expense relatively easily. But even for them, a large proportion of their assistance went into paying the rent.

While rent in Jordan depended on the house and family size, most respondents paid between 100-150 JODs ($141-$212) for rent and utilities. For many, this sum was 80 percent of their income, leaving very little for food, medicine, childcare, or other living expenses. One 36-year-old Yemeni respondent who lived with his wife in Amman worked at restaurants or in construction and earned 250 JODs (~$353)per month at best. Rent and utilities alone cost up to 180 JODs a month (~$254). “We don’t think of food as much as we think of the rent. We live off tea and bread.”

Aarya, a Sudanese woman in Jordan, lived with her husband and three children. She was the only one working in her household at the time of our interview. Her husband suffered from a tumor and needed care. They received a monthly payment from the UNHCR but still struggled to meet their expenses. Aarya worked at local salons offering on-demand beauty services but could not work full-time due to her husband’s health.

When asked about the expenses that put on most pressure on her financially, she said, “It is rent. Food, we can manage. We work for a few days and buy cheap things and get us going. We can suffer medical issues and take painkillers from charities. But rent is most difficult. It has been two months that I have not paid the landlord. We tell him that we have circumstances, and we are not working, and he waits for two days. When he [pressures] us, we try to borrow money from the guys (other refugees), but even their situation is not any better. There is no work, and even the people they work for sometimes do not pay them.”

Bribes

Bribing is a fact of life for everyone in our research sites, refugee and host communities alike. But our respondents believed that migrants and refugees needed to pay more bribes than hosts. They offered three reasons. First, bribing was needed for activities unique to refugees and migrants. Second, they often lacked the required documents to reduce the need for bribes. Third, their precarious status made them easy targets.

In Mexico, Haitian respondents explained how bribes were part of their immigration process. Mexican immigration officials would “lose” one or more of their payments for humanitarian or asylum applications and then require additional payments to complete the process. To quote one respondent:

“Immigration asks us to pay in two parts. If we pay the first part, they don’t give us the card. You hope that the second payment is all you need. But when you bring that, they say the first payment was lost. You may even have a copy of the receipt … but when they look, they say, ‘The money has been lost.’ This has happened to a lot of Haitians.”

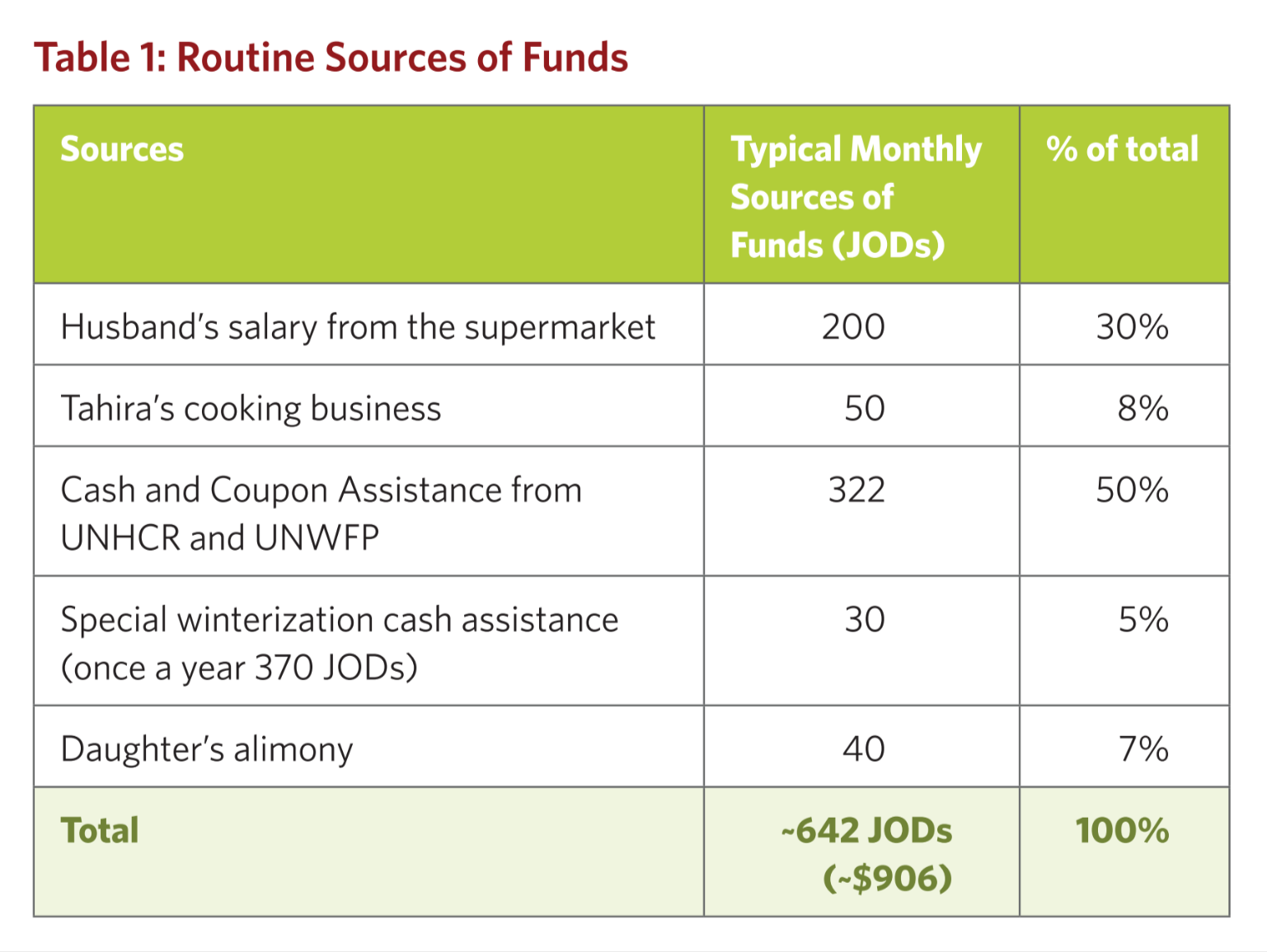

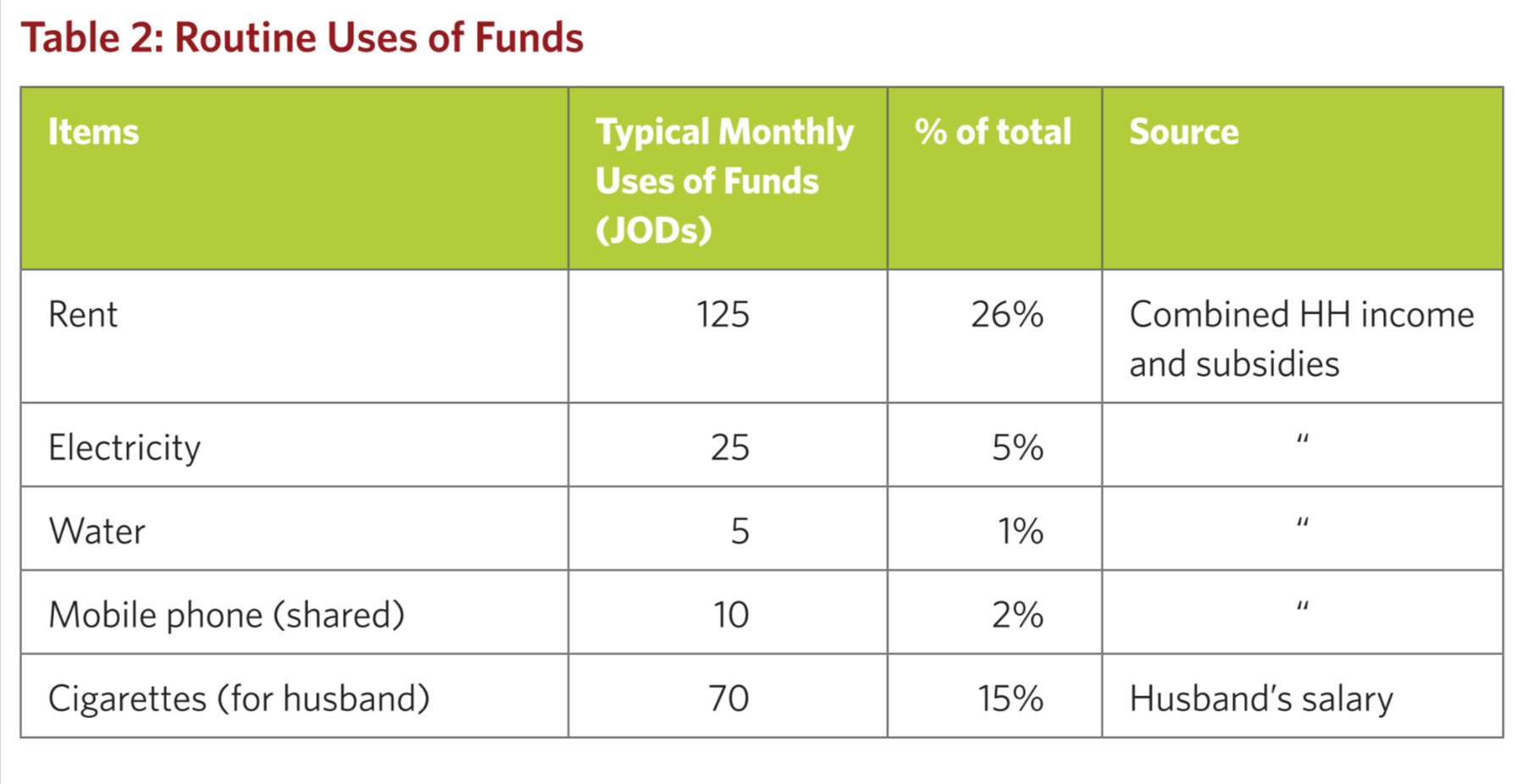

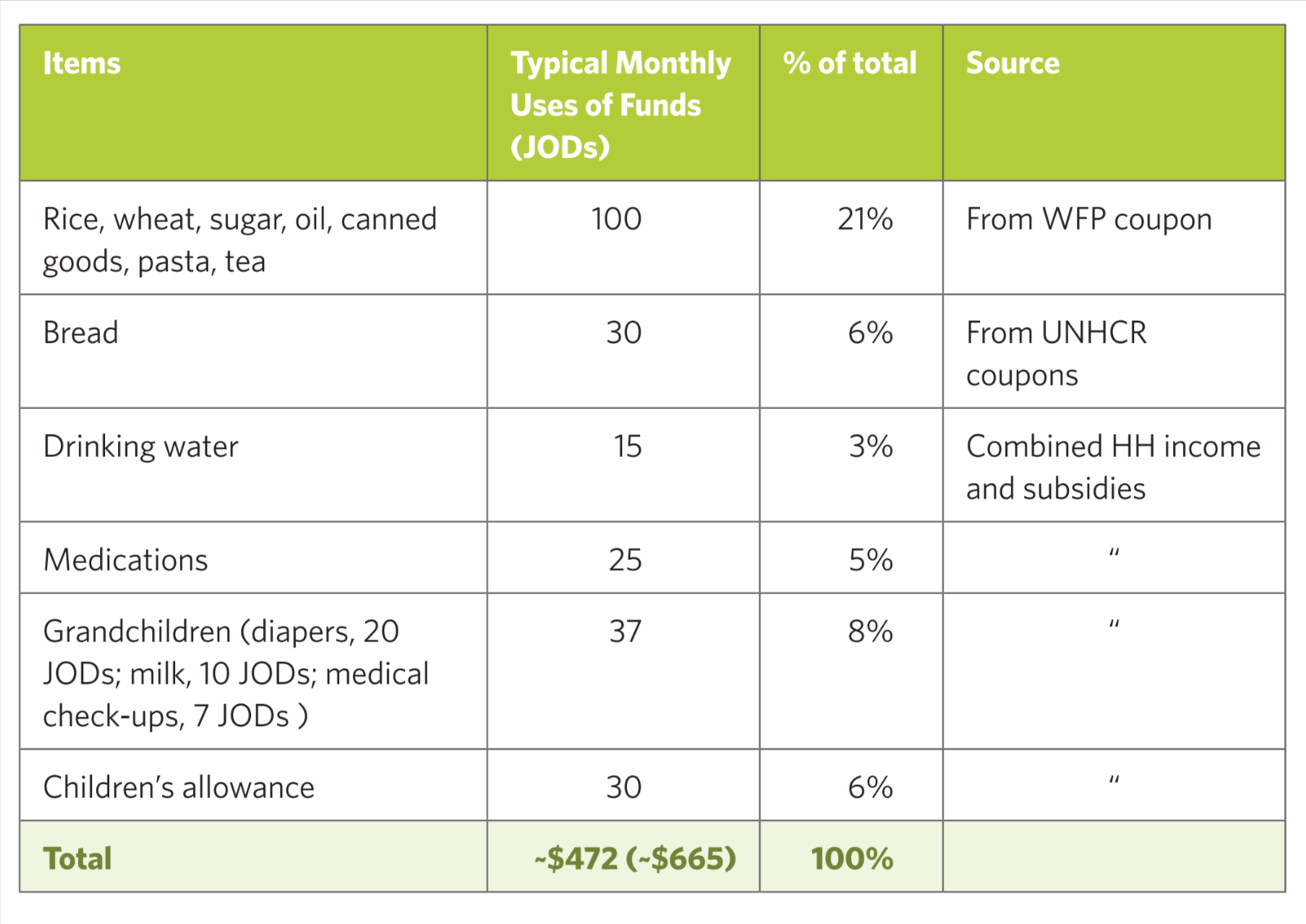

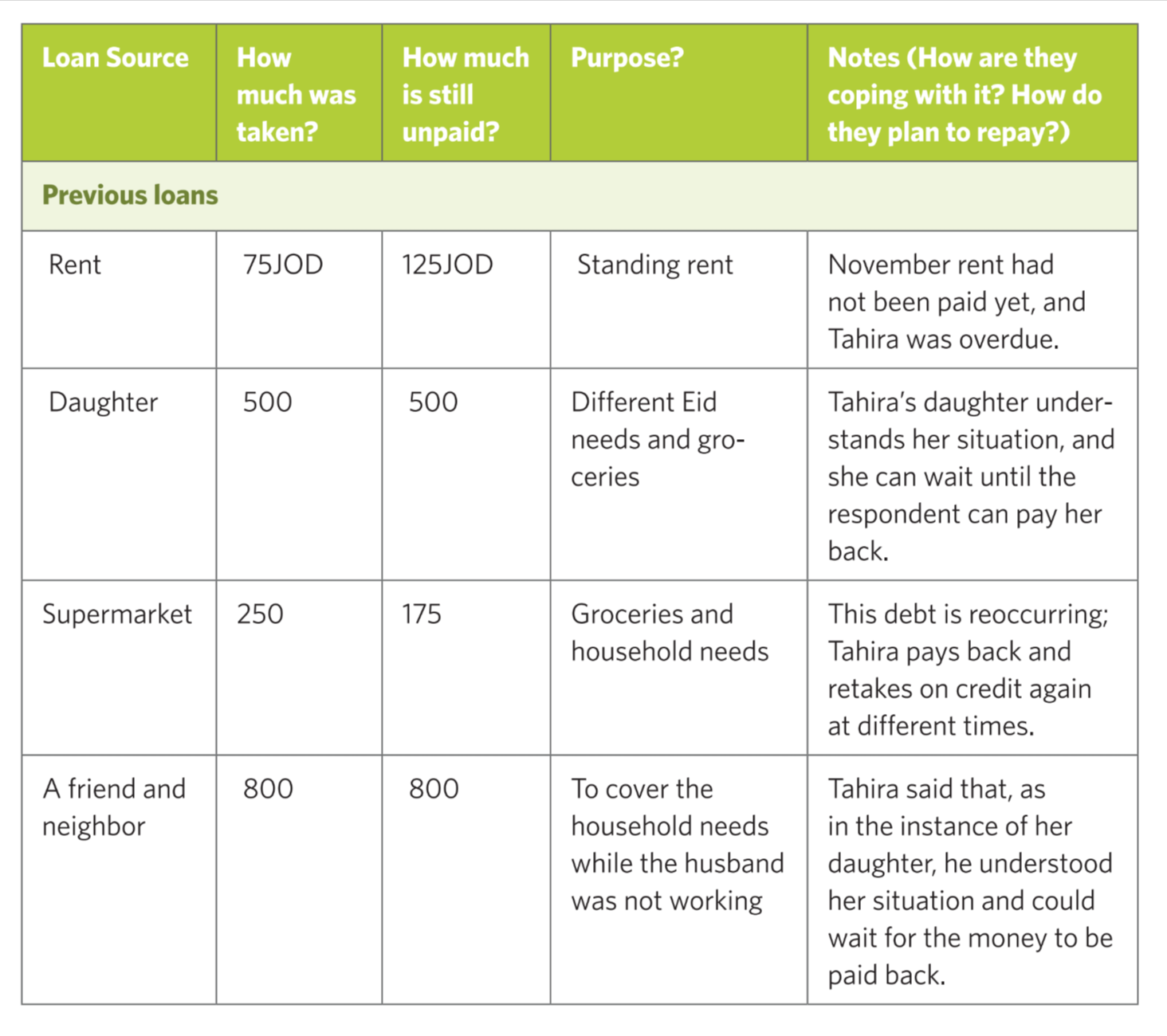

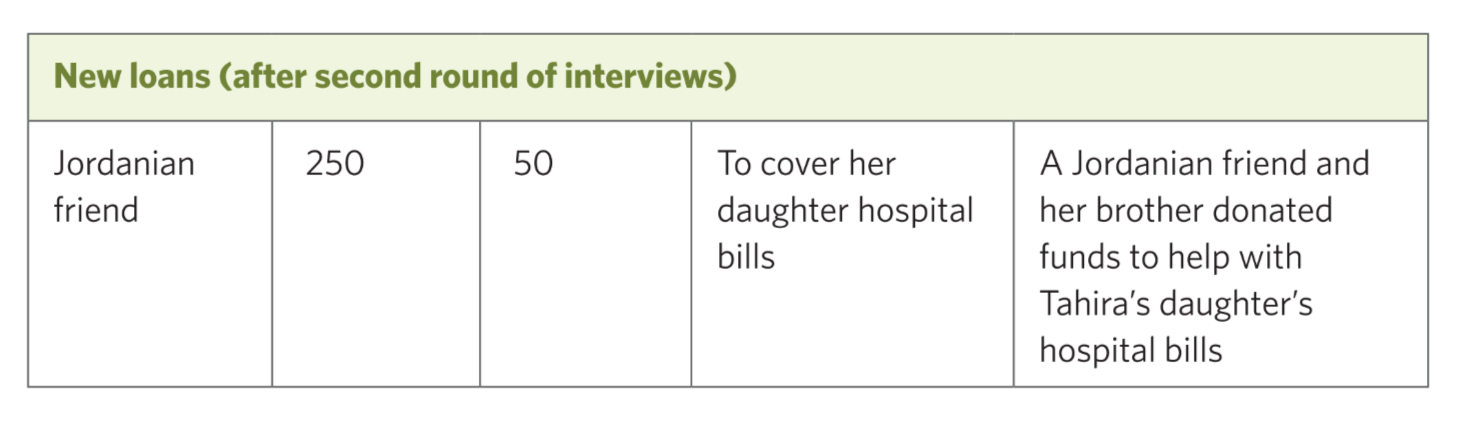

Sources and Uses – An Example of a Refugee’s Financial Portfolio